Do you remember The Weakest Link game show that was on years and years ago?

First debuting in the U.K. on Aug. 14, 2000, it was picked up in the U.S. the very next year for, I believe, a total three-year run. Here’s NBC’s official description of it:

“In each episode, eight contestants enter the studio as total strangers but must work together to bank the maximum amount of prize money available in each round. The contestants take turns to answer general knowledge questions to build chains of correct answers.

“Consecutive correct answers greatly increase the value of the chain, while incorrect answers break the chain and force the contestants to start over on the lowest rung with the smallest amount (of) money. At the end of each round, contestants vote to eliminate the fellow contestant they consider to be the ‘weakest link’ in the chain.

“The contestant who receives the highest number of votes leaves the game as (the host) declares the iconic phrase, ‘You are the weakest link. Goodbye.’”

Now, there’s only one winner allowed in the end. And, obviously, once the competition gets down to the final two, each person is going to vote the other out to get the grand (and only) prize for himself or herself.

That’s why the last round cuts right to the chase. Each contestant gets five questions. Whoever gets the most wins while the other walks away with nothing.

That’s it.

That’s how the game is played.

A Snarky Show That Models the Stock Market

The original host, Anne Robinson, was a snarky Englishwoman who knew how to make participants wince and viewers gape. Her cutting comments about people’s positive and negative progress alike was truly something to watch.

Her nickname, according to IMDb, at least was “The Queen of Mean.”

Then again, that’s part of the reason why people watched it. That snark gave the show a unique flair compared to, say, Who Wants to Be a Millionaire, which has much nicer hosts.

The show has been syndicated around the world, with French, Dutch, Australian, Portuguese, Italian, Taiwanese, Finnish, and Brazilian versions – to name a few. I can’t speak for all of those, but I imagine their hosts were equally cold, cruel, and calculated.

Otherwise, would it really be The Weakest Link? You might as well have The Apprentice without Donald Trump.

(Sorry, Schwarzenegger.)

Incidentally, The Weakest Link was picked up in the U.S. again just this year, airing its first new episode on Feb. 1. This time, actress Jane Lynch – who became famous for her own merciless portrayal on the high school singing comedy Glee – is hosting.

And while she probably doesn’t have quite the same flair as Robinson, she still does a pretty decent job of making people squirm. Once again, there’s no pity there.

In which case, The Weakest Link has more than a few things in common with the stock market.

At the End of the Day, the Stock Market Couldn’t Care Less About You

Like The Weakest Link, the stock market doesn’t care about your feelings. In the same way, it can either make you a lot of money or lose you a lot of money.

It all depends on how you answer the questions it presents.

Also similar are the categories of those questions presented: History, geography, math… even some pop culture. It can and will throw all that your way.

And then, of course, there are the classics: Who likes what? How much do they like it? How long will they like it for?

That’s not to say the game show and market are completely alike. On the plus side, you get to choose the questions you decide to answer when investing. If you’re not comfortable with one category, you can leave it alone – without losing everything you’ve made from previous correct answers.

Though there's a definite downside too in their dissimilarities as well.

Every human being has some sort of gentler emotion about someone – some weak spot people can exploit to soften them. It might take a lot of time and research to find it, admittedly, but I firmly do subscribe to the “no man is an island” theory.

The stock market, on the other hand, is a complete sociopath. It simply doesn’t care if you win or lose, succeed or die trying.

That’s why it’s usually best to play it safe by picking the stocks you’re most likely to win with.

And to avoid the weakest links as if you knew someone was going to mock you for it when you fail.

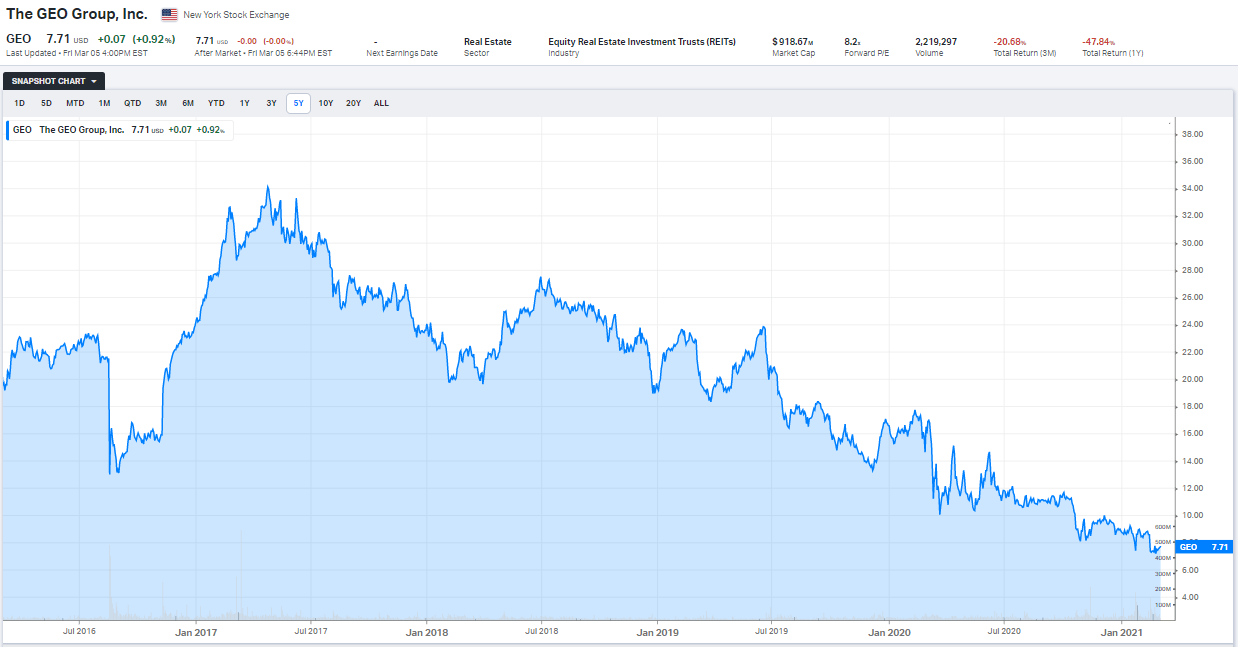

Avoid this Prison REIT!

My first weakest pick is the Geo Group (GEO), a prison REIT that owns 118 facilities that includes 93,000 beds in the US, Australia, South Africa, and the United Kingdom. GEO is the last prison REIT in the sector as CoreCivic (CXW) has opted to trade as a traditional C-Corporation.

In my view, CXW’s decision to convert back to a C-Corp is a wise move, as the company can focus on debt reduction instead of being forced to pay out dividends (in the REIT sector).

However, GEO doesn’t have the same luxury…

As Julian Lin recently pointed out,

“GEO reports its debt to EBITDA as 5.2 times as of the latest quarter. However, GEO excludes “non-recourse debt” (mortgage debt) from the calculation. I view such an adjustment as dubious because not only is it not standard in the REIT industry, but non-recourse debt is still debt.

Accounting for $2.6 billion in unsecured debt, $324 million in non-recourse debt, and $283 million in cash, GEO has $2.6 billion in debt. Compared to $439.8 million of adjusted EBITDA in 2020, debt to EBITDA stands at 5.9 times. However, GEO has guided for 2021 to see adjusted EBITDA of $400 million at the high end of guidance. Debt to EBITDA would stand at 6.5 times.”

GEO cut its dividend in January 2021 by 25% to $1.00 per share (annually) and even after that, shares are now yielding 13.0%. As far as I’m concerned, any REIT paying over 10% is not healthy…

And as Julian Lin points out, the real threat to GEO’s not-sustainable business model is the company’s “outsized 13.7% exposure to the Federal Bureau of Prisons (‘BOP’).”

Lin writes that “The Biden administration has instructed the BOP to not renew contracts with private prisons” and “cash flows appear to be in danger of falling in free-fall - debt to EBITDA will rise as a result. Shareholders should not assume that this recent dividend cut will be the last.”

We maintain a SELL.

Source: Koyfin

GEO shares plunged 19.5% in February and by 13% year-to-date. Given the political headwinds surrounding this REIT, we believe that investors should be extremely cautious. In hindsight, CXW appears to be better equipped to navigate the turbulence because it’s not obligated to distribute 90% of taxable income to maintain REIT status.

In our view, GEO is a “sucker yield” bet!

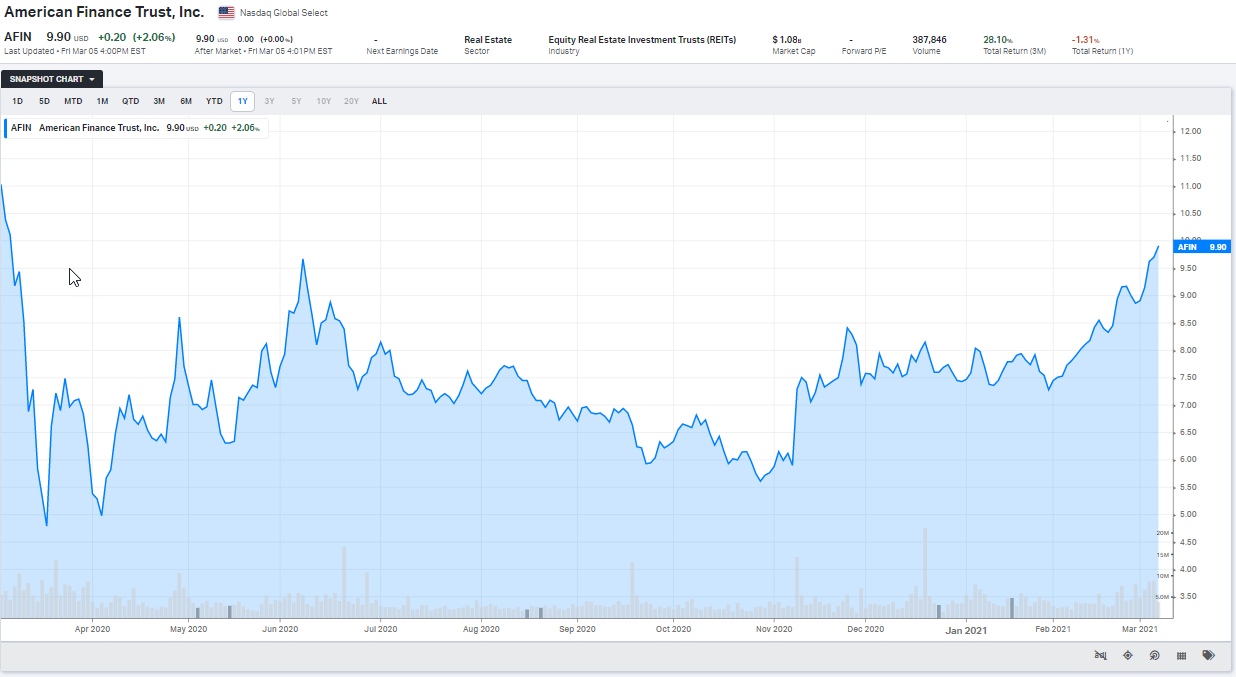

Another Sucker Yield Bet

Speaking of “sucker yields” our next “weak link” pick is American Finance Trust (AFIN), a retail REIT that owns a portfolio of 920 properties (19.3 million square feet) consisting of 887 single tenant buildings and 33 multi-tenant properties.

As the end of Q4 2020, the portfolio was 93.9% occupied with a weighted average remaining lease term of 8.8 years. In January 2021, the cash collection for the portfolio was 97%.

These numbers aren’t too bad, right?

When you dig deeper into AFIN, two things spook me…

First, AFIN is externally-managed by AR Global Investments LLC and several key executives are also key real estate professionals of both firms. For example, Global Net Lease (GNL), an entity advised by affiliates of AR Global, invests in sale-leaseback transactions involving single-tenant net-leased commercial properties in the U.S.

As many readers know, I'm not a big fan of external management, and in addition to conflicts of interest, AFIN may be required to pay a substantial internalization fee at some point. In addition, the advisory agreement with AR Global does not expire until April 29, 2035 and is automatically extended for successive 20-year terms.

The other issue I have with AFIN is the payout ratio.

AFIN cut its monthly dividend last April (2020) from $.0917 per share to $.0708 per share, and is currently paying out $.8496 per year (in dividends). That’s a 22.8% dividend cut…for a Net Lease REIT (that also owns 33 shopping centers).

And even after a dividend cut, AFIN shares are now yielding 8.6%.

Why is that?

Upon closer inspection, AFIN’s payout ratio is a troubling 94%, even after the dividend cut, and the company’s cost of capital is around 7%. When you examine the acquisition activity, you will see some interesting “yield enhancement” activities.

Short-term leases with credit tenants like Advance Auto (AAP) and long-term (20 year) leases with companies like Mammoth Car Wash (non-rated of course).

Source: Koyfin

I have no interest in the common shares of AFIN (although we have recommended the preferred) as there are better alternatives without the conflictive management structure and elevated dividend risk.

We maintain a SELL.

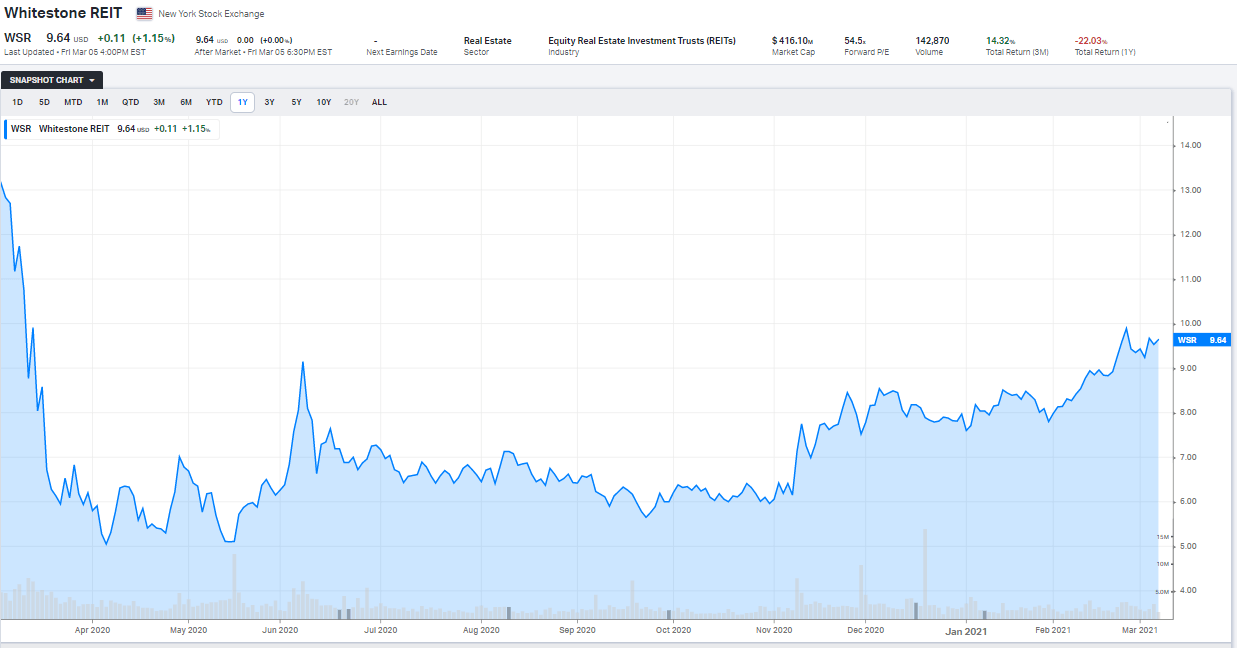

Who Likes Texas Toast?

Our final “weak link” REIT is Whitestone REIT (WSR), a shopping center that focuses on key markets such as Texas and Arizona’s fastest growing cities. The company owns 58 properties (5 million square feet) with over 1,300 tenants.

WSR is not like the other shopping center REITs that are mostly anchored, instead WSR is “consumer focused” where it leases to many “mom and pop” customers and small franchisees. The top categories include (based on ABR):

- Restaurant & food service: 23%

- Grocery: 9%

- Financial services: 9%

- Salons: 8%

- Medical & Dental: 7%

- Non-Retail: 6%

- General Retail: 5%

- Apparel: 4%

- Home Décor: 4%

- Education: 4%

- Fitness: 4%

We were bearish with WSR prior to the pandemic as we feared a likely dividend cut, and of course, that is precisely what happened to WSR as the company announced a whopping 63% dividend cut in March 2020.

The monthly dividend was reduced to $.035 per share vs. the prior dividend of $.095 per share that resulted in more than $30 million of annualized cash savings. The company has since increased the dividend recently to $.035833 per share (paid monthly), a 2.3% increase.

Wow!

A 63% cut in March 2020 and a 2.3% increase in March 2021. That’s not what I would call a "lot of love."

But then again, most shopping center REITs are still suffering from the lingering effects of the COVID-19 pandemic.

One of the reasons we included WSR on the “weakest link” list is because of the weak quality score, our iQ (quality scoring) model puts a “39” on WSR, that is one of the overall worst in our coverage spectrum.

A big part of the score is attributed to WSR’s high leverage and the fact that the company has 16% of its leases expiring in 2021 (800,000 square feet).

As noted, WSR’s tenants are much smaller than the average shopping center REIT and this makes the company more of a small business landlord than a traditional retail landlord.

Source: Koyfin

In addition, as many investors are preparing for rising rates, we’re concerned that WSR’s tenants will continue to struggle as they get their feet on solid footing. PPP has saved many businesses, but we believe there will be longer lasting effects to WSR’s business model, and one in which high leverage could be problematic.

We maintain a SELL.

In Closing

We’re gearing up for our annual March Madness series in which we plan to highlight the “Sweet 16 REITs”. I can guarantee you that none of these three REITs listed in this article will make it to the finals.

In fact, they will not make the CUT whatsoever… perhaps that’s obvious since they did already “cut the dividend cheese” last year (so to speak).

From time to time I will get a reader who asks me about the REITs to avoid, and hopefully this article is helpful. If I can help one reader avoid painful losses, I feel as though I have done my job.

“The chain is only as strong as its weakest link, for if that fails the chain fails and the object that it has been holding up falls to the ground.” Thomas Reid

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.

March Madness Price: $999 For All 3 Services

Join iREIT on Alpha today and get a “front row seat” to our “March Madness” REIT Bracketology series where we break down each property sector to arrive at the “Sweet 16 REITs” to own.

We include exclusive video so our members can get all of the latest and greatest insight and maximize portfolio performance. Our coverage spectrum includes equity REITs, mREITs, Preferreds, BDCs, MLPs, ETFs, and we recently added SPACs to the lineup.

And this offer includes a 2-Week FREE TRIAL plus my FREE book.