Investment Thesis

Cigna's (NYSE:NYSE:CI) shares have increased by 20% on a year-to-date basis outperforming the S&P 500 (SP500) by 6.7%. The company's acquisition of Express Scripts in 2018 has been beneficial for its earnings per share which is increasing on a double-digit basis since 2017. Earlier this year, Cigna agreed to acquire MDLIVE, a virtual care delivery platform that is expected to diversify the company's services further. Following this acquisition and based on the trend in the company's memberships, we expect another boost in its revenues. Cigna managed to successfully integrate the acquired companies into its business model and managed to control its balance sheet since 2018 by continuously decreasing its debt burden.

Based on its management guidance and its historical financial metrics averages, we found that Cigna is an attractive investment opportunity that might offer its investors a further 17% upside potential.

Business Overview

Cigna Corporation is a healthcare conglomerate offering health insurance and pharmacy services. The company launched Evernorth in late 2020, a new brand meant to accelerate the innovation of flexible solutions for health plans, employers, and government organizations. Then, in 2021 it announced the purchase of MDLIVE.

Following the launching of Evernorth, the company updated its business segments to better reflect its innovative portfolio of services offered:

- Evernorth segment (72% of 2020 revenues): delivers innovative and flexible solutions to employers, health care providers, and government organizations, including pharmacy services, care solutions, and data analytics;

- U.S. medical segment (24% of 2020 revenues): provides comprehensive medical solutions to insured and self-insured customers including medical, and pharmacy services and health advocacy programs;

- International segment (4% of 2020 revenues): provides a full range of medical, life benefits, and other products in over 30 countries.

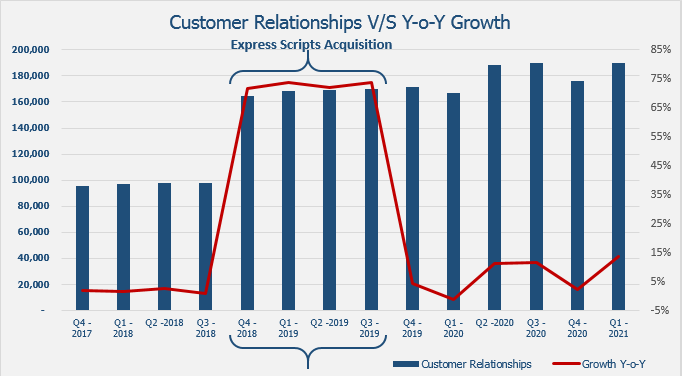

As shown in the below chart, Cigna managed to increase its customer relationships over the years continuously. This number was tremendously boosted following the acquisition of Express Scripts and continued its upward trend.

Source: Company's filings and author calculations

MDLIVE Acquisition

MDLIVE's main business operations rely on a digital platform offering low-cost Urgent Care Clinic alternatives facilitating doctor-patient visits via a new innovative concept, "Telehealth." MDLIVE benefited from the COVID-19 emergence as there was a massive push toward telemedicine and telehealthcare following the risks of physically going to hospitals for light or medium case consultations.

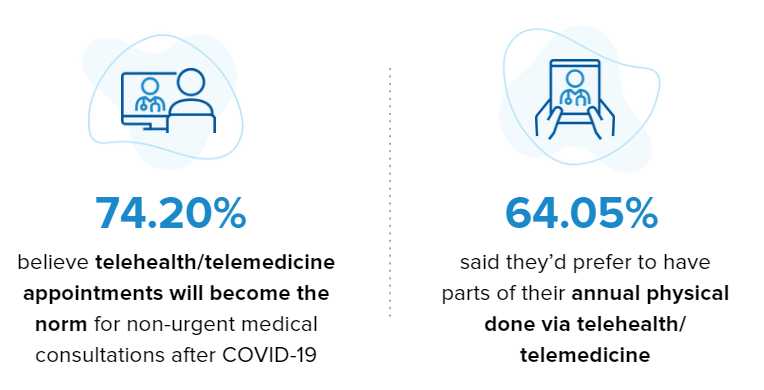

A recent study on the Telemedicine industry shows that the size of this market has huge potential over the coming years. It is anticipated to grow at a CAGR of 25.08% during the period between 2019 and 2026. Thus, after being estimated at $41.63 billion in 2018, the market size is projected to reach $ 397 billion by 2026. In fact, according to another survey conducted by Sykes comparing pre and post-pandemic patients' behavior concerning telemedicine, 87.82% of patients want to continue using telehealth services for non-urgent consultations after COVID-19. In contrast, during the pre-COVID period, 65.60% were hesitant and doubted the quality of services offered via those portals.

Source: Extract from Sykes survey

We do not know the exact acquisition price of MDLIVE, but it is estimated that its valuation is near $1 billion. MDLIVE seems to be a good fit into Cigna's business model and is expected to bring new opportunities for the company amid stellar potential growth in the Telemedicine industry.

As per Evernorth president and COO Eric Palmer:

Combining MDLIVE's platform and strong network for virtual providers with our comprehensive care solutions, we will be better positioned to optimize the care journey to improve affordability and accessibility, and to deliver superior support to health plans as they advance their own care delivery models for the future.

Attractive Fundamental Metrics

In addition to MDLIVE's recent acquisition, we found that the below fundamental metrics can trigger higher price levels for Cigna in the coming period:

Growing revenues combined with increasing bottom line

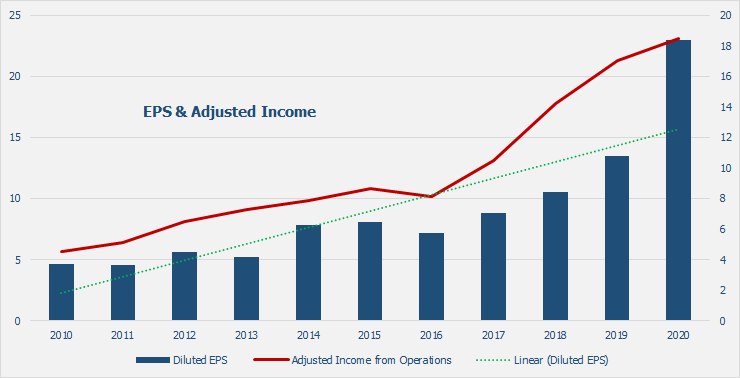

Given Cigna's expansion over the years and its targeted focus on providing affordable and simple health solutions to its customers, it successfully increased its revenue at 11% on average since 2010 (excluding FY2019, where growth was beyond 200% due to the acquisition). Furthermore, the company maintained a profitable bottom-line where diluted EPS grew from $4.65 in FY2010 to $22.96 in FY2020.

Source: 2021 Investor Day Snapshot and author calculations

Cigna debt levels

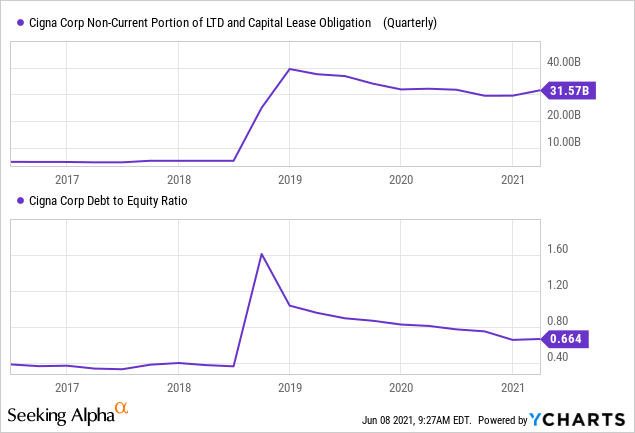

Cigna's debt surged in 2019 following the acquisition of Express Scripts. However, the company managed to reduce the debt burden's impact on the balance sheet significantly. Debt to Equity decreased to 0.66 after reaching 1.6 two years ago, while long-term debt decreased by approximately $9 billion since the acquisition leading to a lighter projected balance sheet.

Share buyback and Dividend

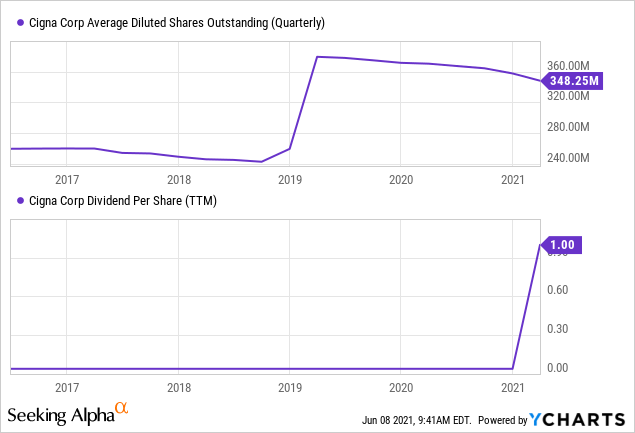

The company is continuously decreasing the number of its outstanding shares. On a year-to-date basis, as of May 6, 2021, 14.4 million shares were repurchased for $3.2 billion. For 2021, management expects that the weighted average shares to be between 346 million and 348 million shares.

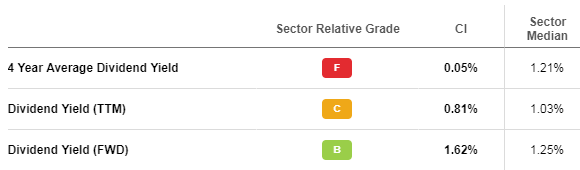

Furthermore, the dividend increase was attractive as the company started paying a quarterly dividend of $1.00, whereas it used to pay a fixed yearly dividend of $0.04 since 2011. This remarkable change increased the forward dividend yield to 1.62% compared to a 1.25% forward dividend for the sector, making the company under the radar of income investors.

Source: Seekingalpha premium features

Potential Risks

Despite its strong fundamentals, some risks pose real threats to the company's upside potential.

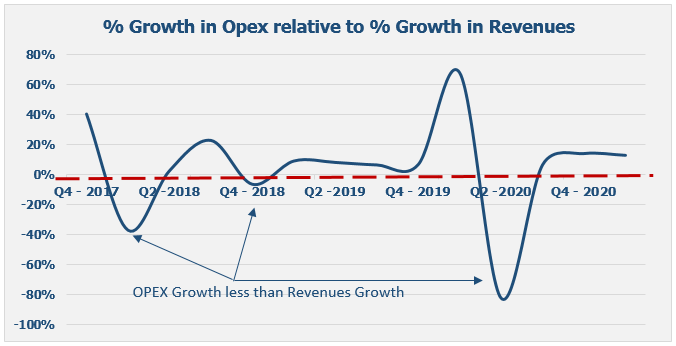

Increase in operating expenses greater than increase in revenues

We checked the year-over-year change in revenues and operating expenses and found that the growth in Cigna's operating expenses is outpacing the increase in revenues, which is expected to have a material impact on the company's future financial operations. Investors should track the change over the coming period and check whether it is within acceptable ranges or deviating towards alarming levels.

Source: TIKR and author calculations

Changing customers trends

Due to COVID-19, the shift towards virtual medicine accelerated at unprecedented levels. The main concern lies in whether this trend will reverse after the full reopening of the economy. In addition, the extensive vaccination rollout might jeopardize the growth in the telemedicine industry.

The dark side of acquisitions

There is always a dark side while acquiring companies. Cigna might be exposed to new risks due to its interaction with new key players: competitors, clients, suppliers... Moreover, the companies offering online services are constantly exposed to risks such as privacy and security, which poses a serious potential liability to Cigna.

Valuation

Turning to the valuation side, we based our assumptions on the management's guidance during their last earnings call. Consolidated adjusted revenues increased to at least $166 billion while diluted EPS is expected at $20.20 per share.

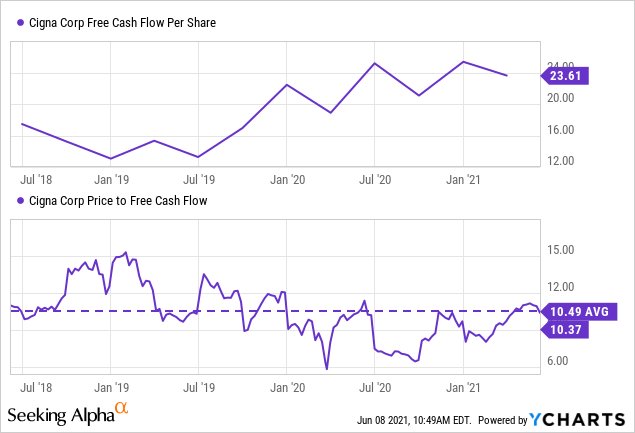

Over the last three years, Cigna's free cash flow margin ranged between 5.5% and 6.7%. For the next fiscal year, we will assume it will be at 5.75%. Thus, we estimate free cash flow for FY21 to be at $9,545 billion. Also, management expects the weighted average shares at a midpoint of 347 million shares. Accordingly, free cash flow per share is estimated at $27.51.

Based on the above chart, Cigna traded at an average 10.49x price to free cash flow over the last three years. As such, and assuming it remains at this average level, our estimated fair value is at $288 per share, presenting an approximate 17% upside potential.

Conclusion

Cigna showed strong growth during the recent years and solid fundamentals that translated into an 18.20% surge in its stock price on a one-year basis. The healthcare provider reached its 52-week high beyond $272 during May and started paying a $1.00 quarterly dividend this year, the first increase since 2011.

Although Cigna is currently trading at relatively high levels, we remain optimistic about the company since there is plenty of reason to be bullish on its future outlook. Following the recent acquisition of MDLIVE and based on its sound financial metrics, we estimate its fair value per share at $288. Management's strong outlook backs this bullish conclusion for the future, implying that the company is continuously expanding and capitalizing on its acquisition activities.