2020 was nuts. The market got crushed but quickly recovered. Therefore, it's important to look at Johnson & Johnson (NYSE:JNJ) with respect to dramatic market fluctuations in Q1 2020 versus Q1 2021.

Here's how the article plays out. First, I show what happened to the market in 2020. It was bad, until suddenly, it was much better. Second, I review earnings today of three big, well-known companies. This is useful to understand the impact of base effects, and bounces. Third, I specifically look at JNJ Q1 2021 results, and the outcome. Plus, I include comments about the long-term view, including dividends.

S&P 500 Reminder

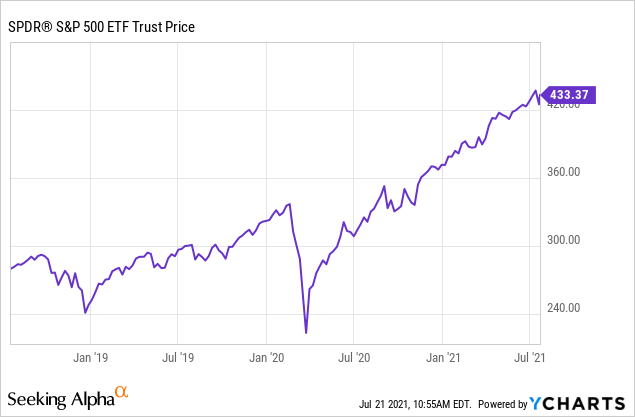

Let's first look at what's happened in the market over the last few years. This view of SPY should clear away any fog.

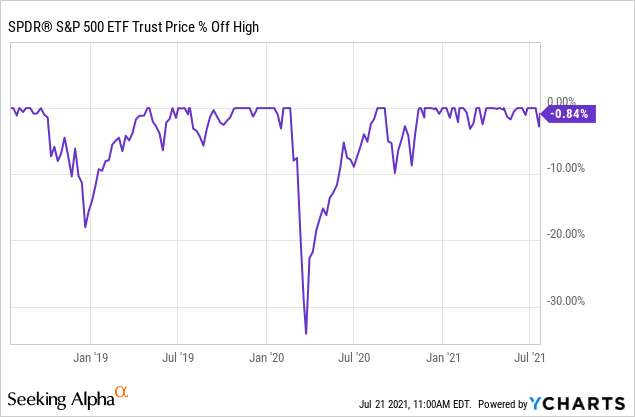

On the one hand, it's completely accurate. On the other hand, this view manipulates the mind because of the massive drop in early 2020. I'll come back to this shortly. First, I want to take another view here:

Two more things stand out here. There was a big drop from highs in late 2018. That's easier to see here. And, the massive drop in early 2020 was truly severe, but the return to all-time highs was equally impressive. The massive "hole" was rapidly filled up with price gains.

The whole point is that Q2 2020 saw a dramatic decline. The entire market died off by over 30% in an extremely short period of time. The media pounced when blood was running in the streets:

Source: CNBC

Source: CNBC

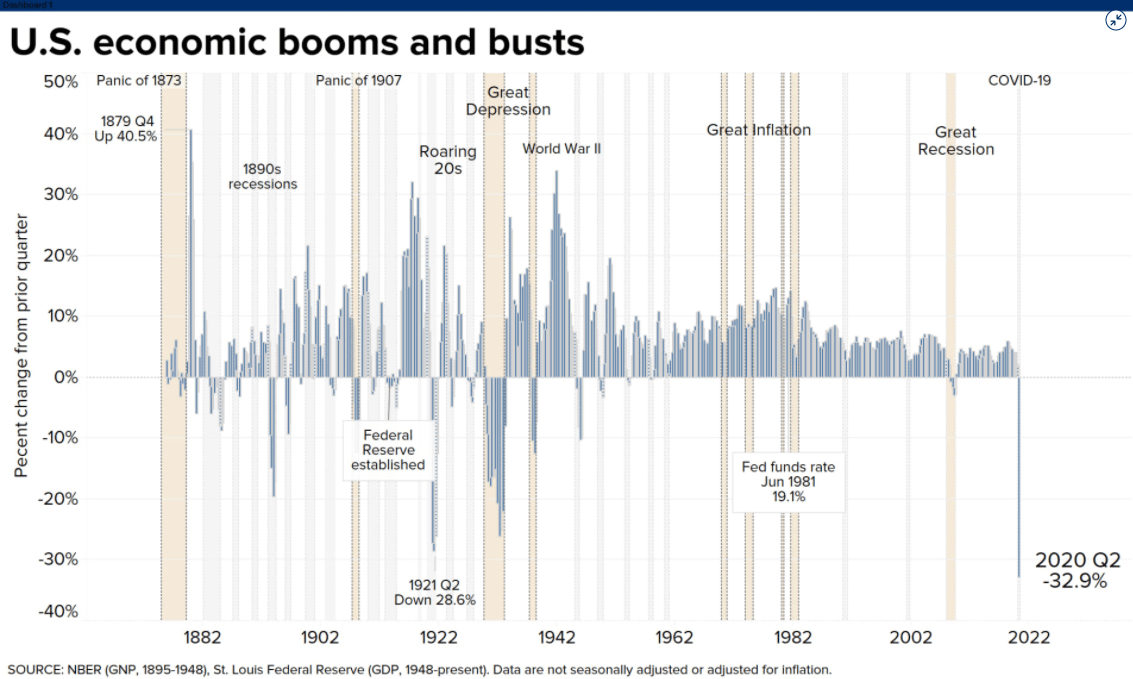

- The U.S. economy suffered its worst period ever in the Q2 2020.

- The drop was worse than the Great Depression and Great Recession.

- We were already in a recession that began in February 2020.

- Many investors forget that Q1 2020 growth was already down 5%.

- At the same time, disposable personal income soared over 42%.

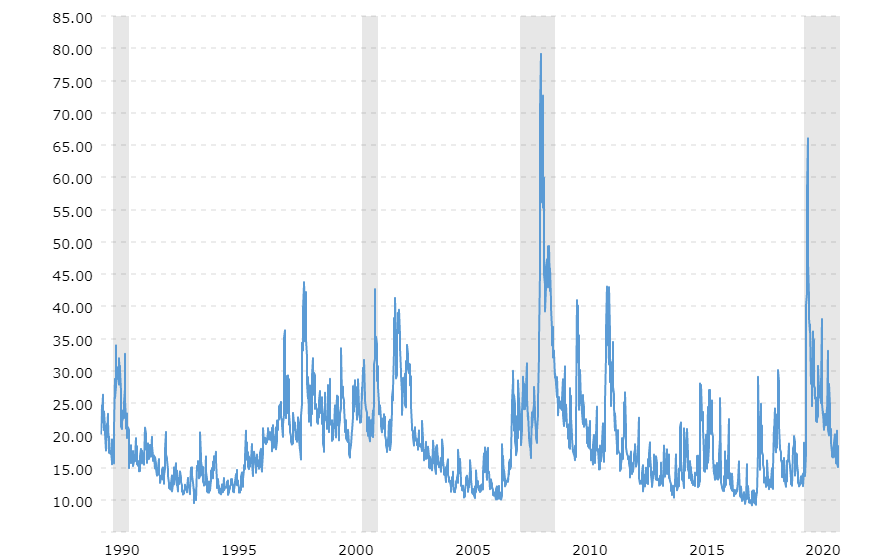

However, generally speaking, it was a very dark quarter. Fear was extreme, although not quite as bad as 2008:

Source: Macrotrends

Source: Macrotrends

Nevertheless, the essential point is that Q2 2020 created a very low base for the stock market. Therefore, companies reporting in Q2 2021 are being compared against Q2 2020. It should be obvious that because of the rapid and robust recovery, the comparisons will be rather shocking.

Big Dogs On Display

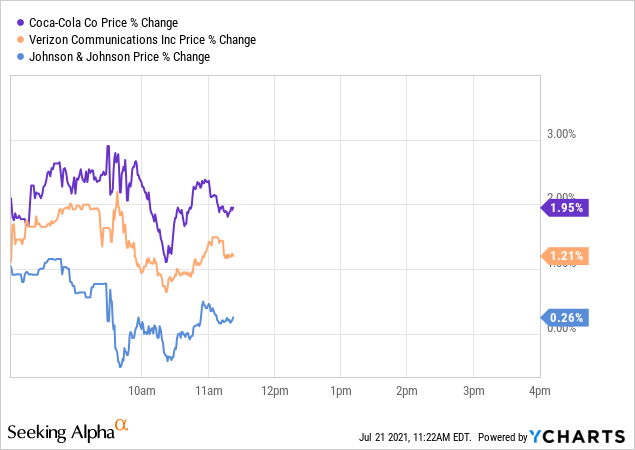

Here are the big headlines today about Coca-Cola (KO), Verizon (VZ) and JNJ. Good news, indeed:

- KO reported a quarterly profit that beat expectations. Revenue rose 42% from last year to reach $10.1B including 37% organic revenue growth.

- VZ also ticked up following the company's earnings announcement, rising by about 1% in pre-market action. This followed a quarterly profit that beat expectations, as strong broadband subscriptions boosted the bottom line.

- JNJ reported a non-GAAP quarterly profit of $2.48 per share. That beat analysts' consensus by $0.19 per share, bolstered by better-than-expected revenue growth of 27%.

And so, stock prices are up in the morning for these juggernauts:

So far, so good. But, notice that KO revenue was up a mind-numbing 42%. Clearly, KO took a massive hit in Q1 2020, so the base effect bounce is evident. On the other hand, VZ revenue was up "only" 11% Year over Year. Quite good, but clearly the pandemic didn't impact VZ the same way it impacted KO.

How About Johnson & Johnson?

Clearly, from the chart above, the market loves what's going on with KO, and VZ is also enjoying a bump. But, JNJ is just kind of muddling along. Not bad, but certainly not amazing given the news.

To be more specific, JNJ revenue was up a whopping 27% YoY. Furthermore, Q2 2021 Non-GAAP EPS of $2.48 beat analyst expectations by $0.19, and GAAP EPS by $0.31 as well.

On top of this, JNJ stacked on more good news:

2021 Guidance: Revenue of $92.5B-$93.3B vs. $92.55B consensus, Adj. EPS of $9.50-$9.60 from prior guidance of $9.42-$9.57 vs. $9.55 consensus.

And, COVID-19 sales are expected to be jolly good, to the tune of $2.5B in 2021. JNJ generated $164M in Q2 2021, up from $100M in Q1 2021. So, clearly there's plenty of vaccine upside, although both Moderna (MRNA) and Pfizer (PFE) will do better. We're told JNJ's vaccine maybe isn't as good.

Coming back to revenue, I need to point out that it translated to an incredibly stout bottom line improvement.

- Net earnings grew ~73.1% YoY

- Diluted EPS grew ~72.8% YoY

That's where it's easy to see the true "insanity" around base rate changes. It's hard to see in revenue, but it's easy to see in earnings. After all, JNJ's 27% YoY revenue increase is hot but the earnings improvements are totally on fire. Again, this is all about base effects.

All-in-all, the good news is captured well here:

- JNJ lifted its 2021 guidance estimating ~10.5-11.5% YoY growth for the base business compared to the 9.7-10.9% YoY projection made three months ago.

- Estimated adjusted EPS (Diluted) stands at $9.60-9.70 compared to the previous forecast of $9.42-9.57 per share.

Summing this up, JNJ isn't really benefitting or suffering from base effects. The market isn't fooled - no surprise - and yet, it appears that JNJ is doing just fine, plodding along as per usual.

Long-Term View

It's always easy to get caught up in the moment, via headlines, media and various news channels. The sky is falling, the sky is falling. Emotions kill returns because investors get sucked in to buy high then sell low. In any case, we all know this. And, one antidote is to zoom out.

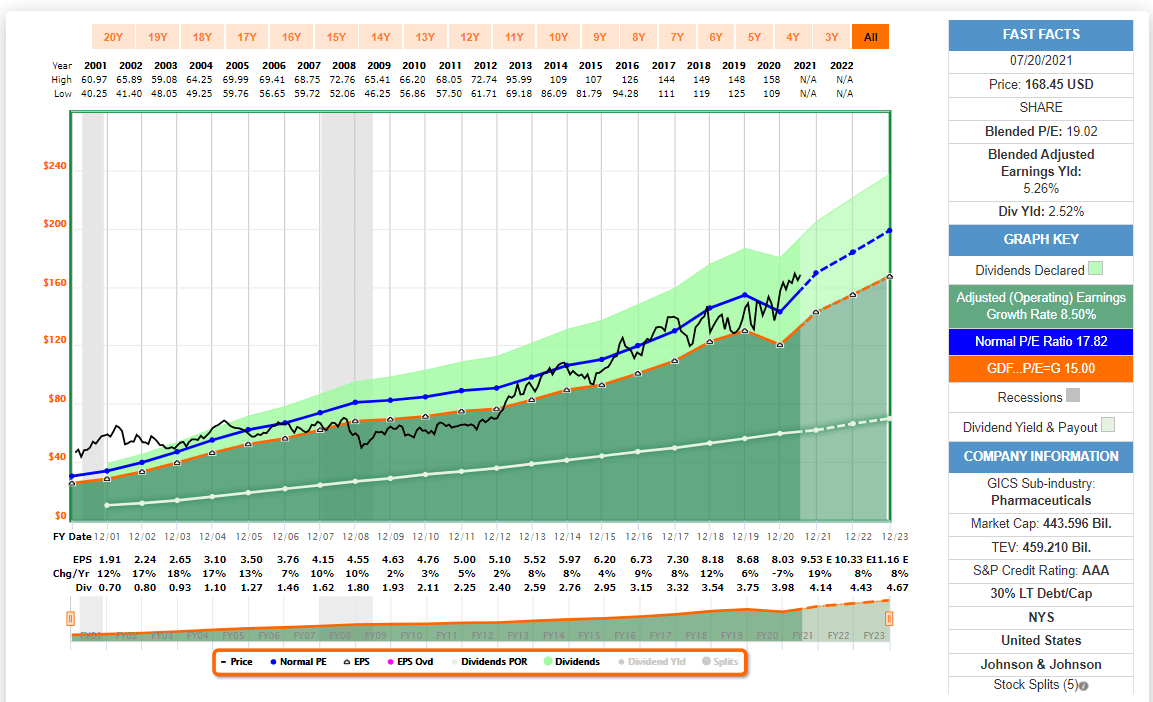

Source: F.A.S.T. Graphs

Sure, we see a drop in earnings in 2020. And, there's certainly been some volatility in price over the years, but nothing extraordinary. The real story is here is steady-as-she-goes.

- AAA S&P credit rating is fantastic

- Debt is easily handled

- P/E ratio is not insane

- JNJ's 2.5% yield beats SPY's 1.3%

- Analysts expect 8% growth in 2022 and 2023

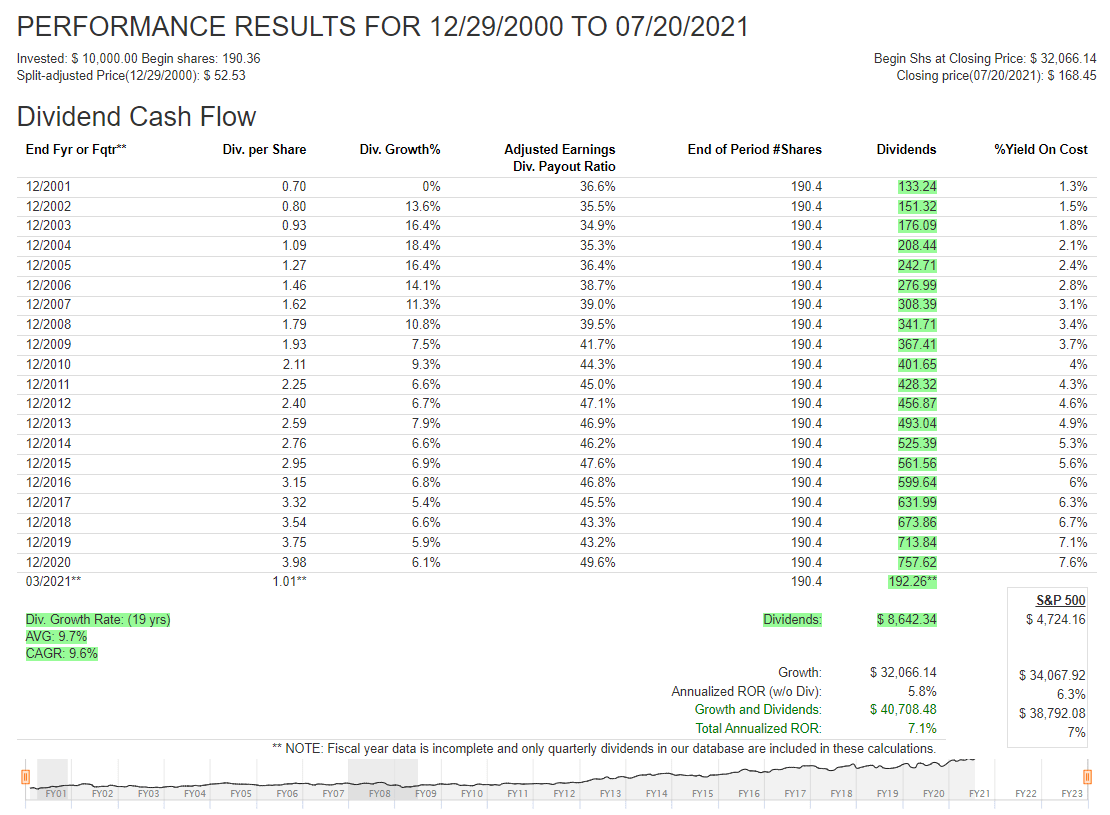

There's plenty more. And while the 2.5% yield isn't incredible, when you look at the 9-10% 20-year dividend growth, or the more conservative 6% 10-year dividend growth, the value proposition is compelling. Over the 20-year view, you're matching the market, with a slightly higher yield:

Source: F.A.S.T. Graphs

As far as expected returns look:

- If P/E falls to 15, then Total Annual ROR is 2.3%.

- If P/E falls to 18, then Total Annual ROR is 5.3%.

- If P/E rises to 21, then Total Annual ROR is 8%.

That's based on EPS growth of 5% in 2021 to 2026, which I think is a bit too conservative. I believe we're more likely to see something closer to 7-8% Total Annual ROR. That'll match the market, or perhaps better, and it'll deliver more dividend income over the next 3-5 years.

I'm not too interested in buying at today's prices. I'd be far more interested, and would likely consider adding to my position, down around $140 to $150. And really, I'd want that even a little bit lower, which would push JNJ's dividend above 3% again. All of this said, I'm relatively bullish on the long-term business. JNJ is an easy hold right now.