Commercial banks, as of August 18, 2021, had $2,422.7 billion in Commercial and Industrial loan on their balance sheets. This is from the H.8 statistical release of the Federal Reserve, "Assets and Liabilities of Commercial Banks in the U.S."

These same banks had $4,100.4 billion in cash assets on hand. There is plenty of money sloshing around in the banking system, as there is plenty of money sloshing around the U.S. economy. The Federal Reserve has created this condition for us.

But, can you imagine that the cash assets of commercial banks is 1.7 times the amount of commercial and industrial loans on their balance sheets. This is certainly not what you would expect from your commercial banking system.

People, and businesses, just don't want to borrow from the banks. They just have too much money available to them to think much about borrowing money from their local bank.

And, the commercial banks don't seem to be too willing to go out and start pushing for loans in the current economic environment.

So, the banks hold onto their cash balances. And, when the Federal Reserve goes out and pumps even more money into the banking system, the commercial banks just sit on that money.

For example, in the month of July 2020, the commercial banking system held $2,746.1 billion in cash assets.

So, cash assets in commercial banks have increased by about 49 percent, year-over-year. This is unheard of.

And, commercial and industrial loans? In July 2020, they totaled $2,864.4 billion, not too far different from the amount of cash the banks had on hand.

C&I loans actually declined by about 15 percent.

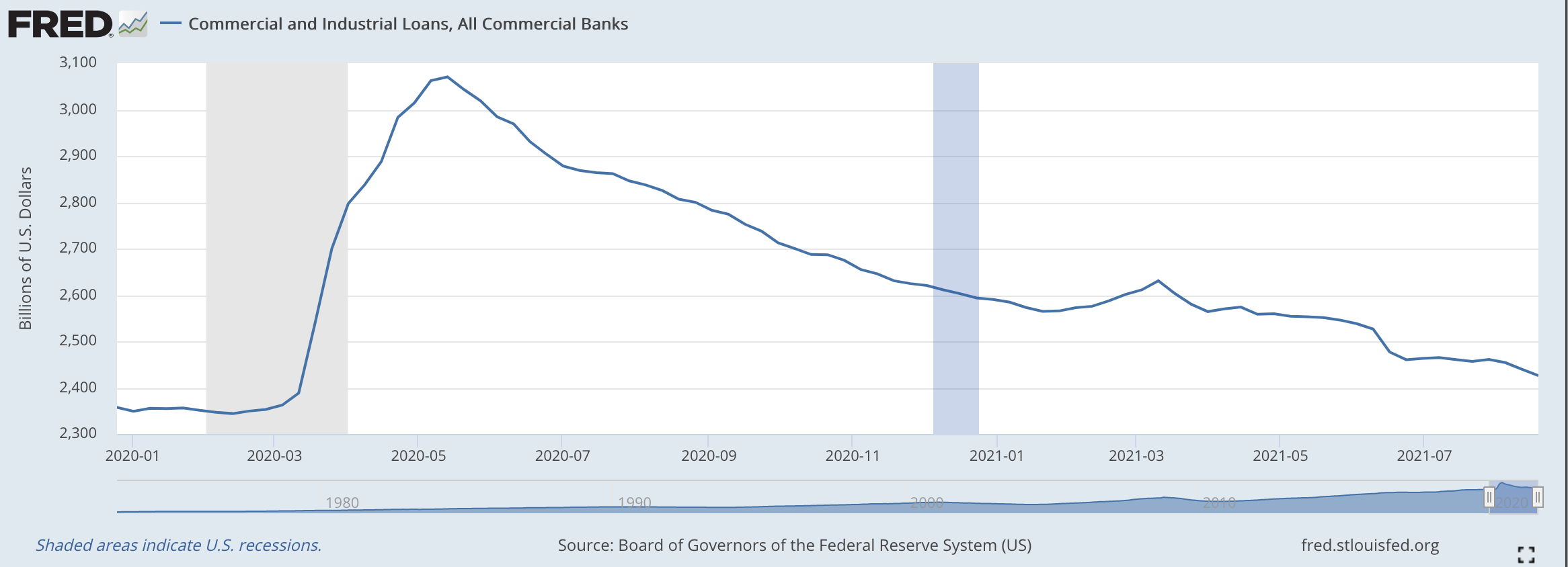

And, how does this look on a chart?

Well, you can see that during the short recession that took place from February through to May, C&I loans really jumped up. You had borrowers in a pretty desperate position and you had the Federal Reserve pumping money into the economy about as fast as it could to help the banks service their customers.

The Fed was out to save the financial system, and the economy along with it.

C&I loans at commercial banks peaked in May and then began to decline.

The decline was quite steady, even though the Fed formalized its "accomodative" policy stance and began to add $120.0 billion securities to its portfolio every month.

As one can see, the totals for the month of August 2021 lie below the numbers attained earlier in this year.

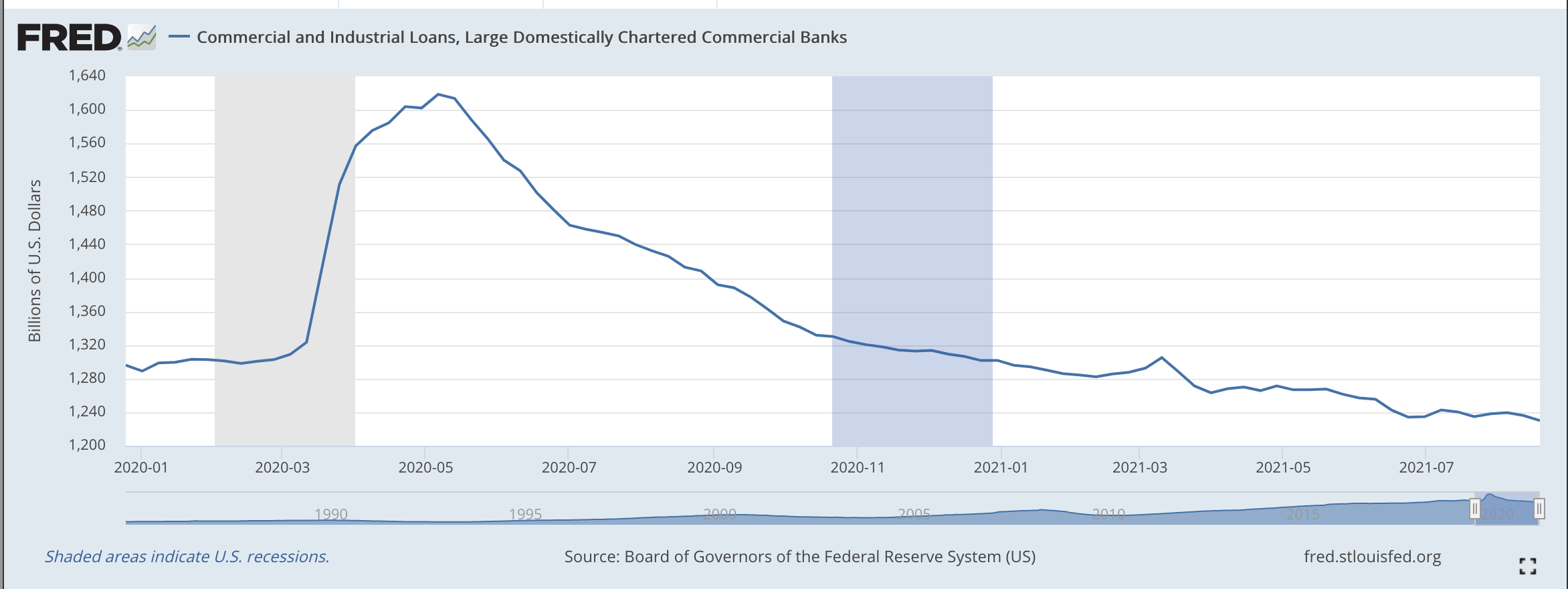

Large, Domestically Chartered Commercial Banks

This movement was dominated by the largest, domestically chartered banks in the banking system. There are only 25 banks in this category.

Comparing numbers, we find that on August 18, 2021, these large, domestically chartered banks had $1,224.7 billion in Commercial and Industrial Loans on their balance sheets. This was just over 50 percent of all the C&I loans on the books of commercial banks in the banking system.

On that date, they also held $1,999.0 billion in cash assets.

In July 2020, the numbers were as follows: C&I loans totaled $1,448.2 billion. Thus, the largest domestically chartered commercial banks in the banking system, 25 of them, held roughly the same percentage of all C&I loans on their balance sheet at the later date.

in July 2020, however, cash assets at these large, domestically chartered banks amounted to only $1,516.7. Cash assets grew by almost 33 percent up to August 18.

The trajectory of commercial and industrial loans at large, domestically chartered commercial banks is captured in the following chart. The flow in these 25 banks pretty much dominates the flow of C&I loans of all the commercial banks in the banking system.

The Rest Of The Banking System

The numbers for the rest of the banking system follow a similar pattern, although they do not present such a dramatic picture.

The rest of the banking system held $817.7 billion in Commercial and Industrial Loans on August 18, 2021, down by about 13 percent from a total of $945.2 billion in July 2020.

Cash assets rose from a total of $564.8 billion in July 2020, to $872.4 billion on August 18, 2021. This rise amounted to about 55 percent.

Other Borrowing

Note, however, that money is flowing into the banks on the other side of the ledger.

As Matt Phillips writes in the New York Times, deposits are up by 30 percent "since just before the pandemic."

"Much of that money has poured into the bank accounts of American households and companies. By the end of May, nearly $830 billion in stimulus check payments had been sent to individuals. Roughly $800 billion more was sent to businesses in the form of programs such as the Paycheck Protection Program. And, about $570 billion was spent on extended and enhanced unemployment insurance benefits, according to data from Government Accountability Office."

Small businesses and consumers did not have to borrow. They had cash in the bank.

Consumers, "they just have more cash. And so they paid off their credit cards, which is a completely responsible thing for them to do."

And so, across the board, loan demand at commercial banks has been down.

The Future

So, when will bank lending pick up again?

Well, there are two thoughts on this. First, as the economy picks up, commercial bank lending will also pick up.

As I have just written, corporations are building up their borrowing sources as they work to financially engineer their ways through the current period of economic recovery. These corporations are building up their lines of credit at banks and are arranging other sources of bank credit, mostly that are short term and easily accessible.

The corporations have the sources, whether or not they use them.

Second, however, there has been a fantastic change in the world over the past two years or so, building upon the foundation of information technology that had been developing before.

The pandemic and its consequences have changed the financial world and there are more sources of money and more different ways to obtain money than ever before.

Many analysts are saying that the smaller banks helped save many, many companies during the pandemic, but, as the economy comes out of the critical part of the downturn, many, many more lending sources are available, electronically, to the potential borrowers and these borrowers have been turning to these other areas.

The point is that borrowers are turning, more and more, to the new sources of money because they are easier to obtain and more available. And, this movement is having a significant impact on the smaller banks.

The big banks will prosper in this environment. Otherwise, however, the world of the smaller banks looks like it is in for some major changes. One consequence will be that the banking system will shrink further.

There is so much money around and there are so many new ways to access it.