Investment thesis: Europe's decades-long environmental and energy policies have been a drag on the EU economy for decades. Higher than global average prices for energy have been leading to economic, thus technological stagnation. This fall and winter, there is a risk that its energy and environmental policies will converge with a number of other regional and global economic factors to create a perfect energy crisis scenario. A possible oil price rally this fall and winter could further exacerbate an already dangerous energy price inflation trend. Much will depend this fall & winter on Russia being willing to ship extra gas to the EU in order to relieve the regional shortage. If the situation will not ameliorate in the next few months, there is a potential for a disastrous economic crisis, followed by a socio-economic and political crisis that has the potential to derail the global COVID recovery. European asset risk will be the first and foremost danger, followed by contagion effects on global assets. There are also opportunities, such as Gazprom (OGZPY), which now holds the key to whether Europe will face a crisis this winter or not.

Europe's energy costs are shooting up due to low natural gas inventories that are in turn leading to record high emissions credits prices. It could still get far worse from here.

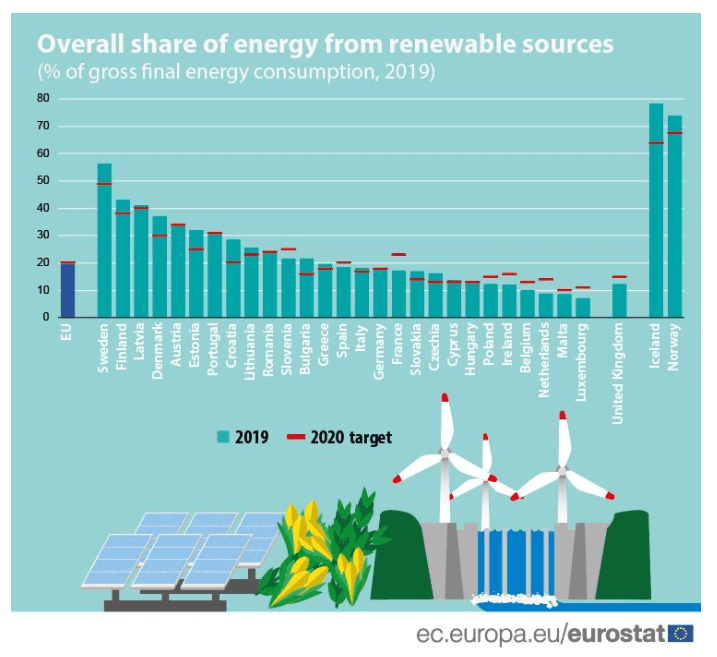

In order to understand the true nature of the crisis that the EU is facing this fall and winter, one has to have a basic understanding of the union's energy policies of the past few decades. The decisions made since around 1990 have been mostly driven by efforts to reduce emissions. Carbon trading schemes, car emissions rules, and regulations, subsidized wind & solar power schemes were all adopted with this goal in mind. To date, the EU managed to cut emissions by 24% between 1990 and 2019. While this fact is hardly being publicized, a great deal of this reduction occurred thanks to a substitution of coal with cleaner-burning natural gas. A great deal of wind & solar power capacity was also added.

Source: EC.

Source: EC.

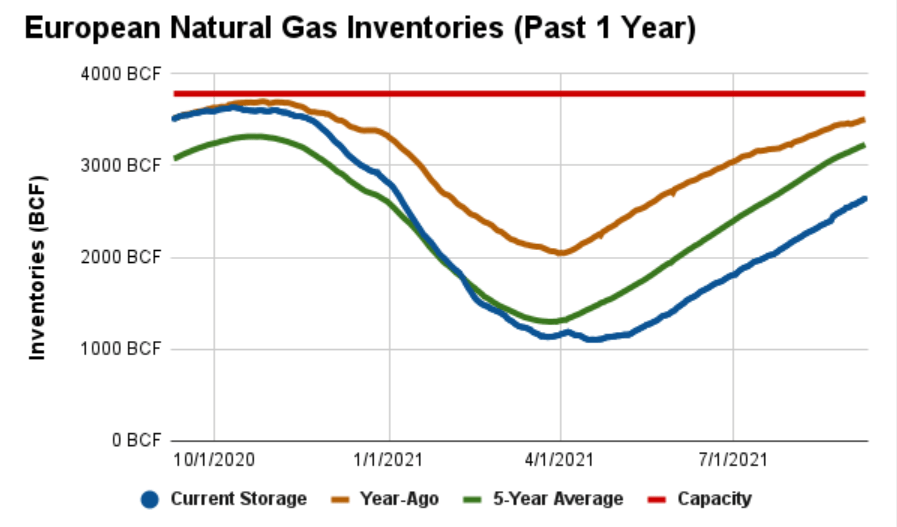

The renewable energy supplies that are captured within the chart above are mostly from three sources, namely hydro, wind & solar power. The fourth major source is biofuel, in other words, crops or biomass. To a great extent, all these sources depend on weather patterns. It is assumed that at most there can be a risk of shorter-term fluctuations in terms of sunlight, wind speeds, water flows and so on that may at most affect one of those sources at a time. What we are learning at this moment, however, is that there can be longer-term variations in renewable power production. Germany's wind power output has been down by about a quarter in the first half of this year. Hydropower, as well as solar output, were also negatively impacted in Germany and elsewhere in the region. What this means is that natural gas and coal had to be burned in order to supply the economy with electricity. Coal power plant output increased by 36% this year, partly due to the recovery but also because of the shortfall in wind power. Natural gas would have been a cleaner alternative backup option, but Europe is facing a depleted natural gas inventory situation this year.

Source: CelsiusEnergy.net.

Source: CelsiusEnergy.net.

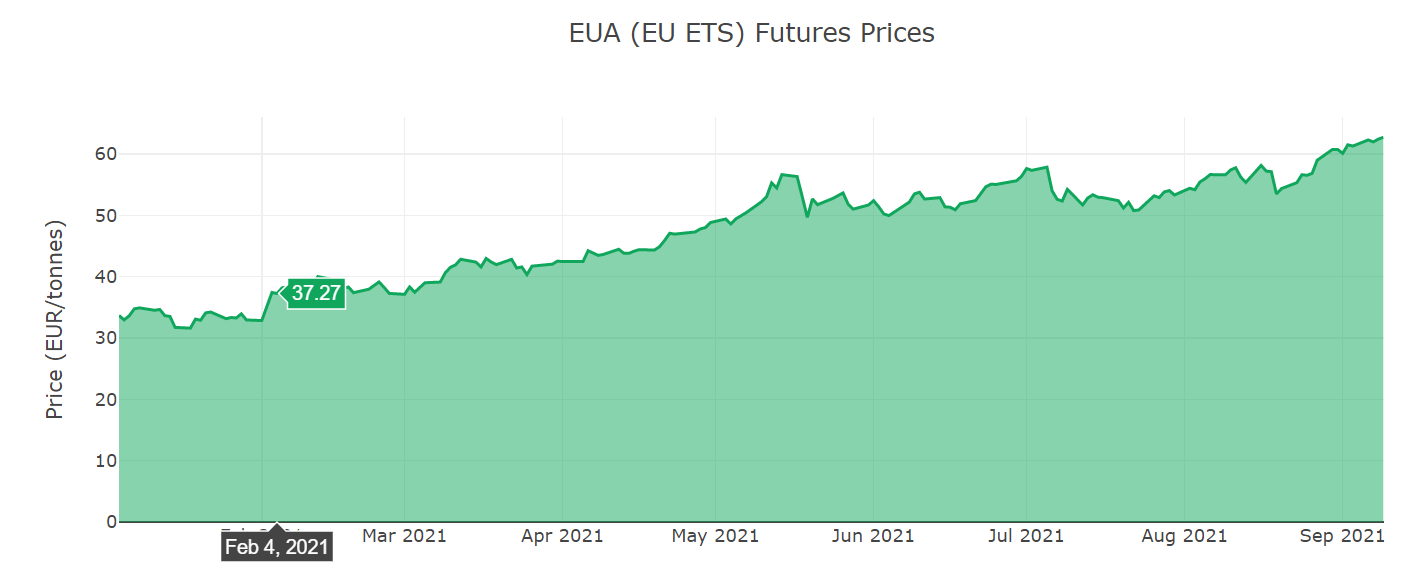

The convergence of factors like the shortfall in wind power in countries like Germany this year and the shortfall in natural gas inventories are causing high natural gas prices, as well as record-high emissions credits prices, all of which are adding up to a spike in energy prices for consumers.

Source: Ember.

Source: Ember.

Emissions credits prices, combined with higher natural gas prices and a number of other factors, are leading to end-consumers of energy having to put up with higher utility bills. In an extreme case, in Romania, where the recent spike in prices, combined with some other market reforms the government just implemented in accordance with EU rules, are reportedly causing household consumers to receive notice from utilities of an increase in their electricity bills that sometimes surpasses 100%. Based on media reports there, it seems that the rise in utility bills is largely blamed on the record-high cost of emissions credits. Only 10% of the households will be eligible for government assistance, therefore 90% of households will have to live with it. Businesses will suffer as well, and this could reverberate throughout the economy. While the increase in utility bills will not be as dramatic in most other EU member states, it will have an impact on most households. It could ignite an inflationary crisis as businesses will find it necessary to pass on at least some of the cost to consumers.

A final blow this winter for European energy consumers might be a further increase in oil prices, which will then increase private and commercial transport costs. There are some oil market scenarios, where in the event that OPEC+ will not be increasing oil supplies fast enough to meet rebounding demand, that can potentially lead to $100+ dollars/barrel oil, according to Barclays. In other words, not only does the EU depend on Russia to relieve the pressure on electricity and natural gas bills this winter by selling more gas to the EU than has been contracted, but it also depends on Russia's decisions within OPEC+ in the next few months. As we know, Russia has become an influential player within the OPEC+ format.

The worst-case scenario can plunge Europe into a socio-economic & political crisis, with unpredictable outcomes.

Most of us may still remember the French Yellow Vest protests that rocked the government for months. It all started with what was a comparatively moderate increase in energy prices, namely a tax on motor fuel meant to promote emissions reductions. The increase in energy costs that will directly affect most households in the EU this winter will have a much bigger impact on household budgets than the proposed motor fuel tax would have ever had. The indirect effects such as rising costs of goods and services will also take a bite into consumer finances, especially among the working lower middle class.

Going back to the example of Romania, where electricity and also natural gas bills are set to soar, the net result will be a retreat in consumer spending throughout the economy. At the same time, prices are set to rise throughout the economy given that it will not be only households that will see their utility bills rise. Because Romania has one of the lowest net wages in the EU and it is also likely to see the largest increase in utility costs, it is likely to see a massive decline in consumer spending. It might be the first candidate to be a canary in the mine in regards to what stagflation will look like throughout the EU. Other Eastern countries will follow, given that lower income levels will lead to an outsized impact on household and company budgets. Then it will move to the Southern Mediterranean countries, where high unemployment rates, lower wages compared with Northern EU peers will bite harder for more households.

While many other countries in the EU will be hit a lot harder by the energy price inflation that is occurring, France will most likely lead in terms of protest outbreaks and it will spread from there. As hard as it may be to imagine, the ferocity and magnitude of the protests we saw before in regards to energy prices are likely to be surpassed this time around. What is worse, there may be few remedies available for the EU or individual governments to try to avoid this crisis or the public anger that will likely show up on the streets and at the ballot box as a result.

Russia has the resources to relieve Europe of its crisis, but it remains to be seen whether it will act.

A few years ago, a late winter to early spring cold spell left most of the EU scrambling to keep the heat and the lights on. The natural gas stockpiles were emptied and there was growing talk of having to shut down industrial activities in order to keep households from freezing in their homes. Gazprom was the only entity that was in the position to prevent Europe from experiencing an all-out crisis, which it did by quickly diverting more natural gas to Europe. This time around, it seems to be content with supplying natural gas to Europe only within the parameters agreed to in its contractual obligations, not beyond it. First of all, it is a way to pressure the EU and Germany to give the legal go-ahead for the now completed Nord Stream 2 pipeline. Second, it seems that Gazprom is no longer as interested in gaining market share in Europe. It is most likely a response to an overall hostile political environment to Gazprom, as well as Europe's own assumptions, namely that it will not be long before they will not need Russian gas anymore, because of the green economic revolution they are undertaking. It is not exactly the message that one wants to send to the only entity that can still defuse this brewing crisis.

In the absence of a Russian intervention, with more natural gas being diverted to the European market, the energy price crisis will continue. If that is the case, there is only one way to avoid a socio-economic and eventually political crisis, and that is to provide most households in Europe with financial support so they can more easily cope with the higher utility costs that we are about to see this winter. The problem with this is that higher energy costs are already adding to inflationary pressures in the Euro area, where the latest reading confirms that inflation is now at 3%, which is a full point higher than the ECB target of 2%. Germany, where household savings tend to be higher, is starting to experience some grumbling over the fact that their cash savings are starting to lose their value. If the ECB were to pump more money into the system in partnership with national governments, there is a very real risk of inflation getting out of control, and it may not be transitory. There are voices in the EU calling for a return to fiscal and monetary discipline.

Investment implications

The initial outcome of an EU crisis will be an outflow of money out of European markets, that will largely end up in the US, which will further boost US stock market valuations. Investors who own European stocks or funds that are primarily dependent on the European market for their revenues are a risky bet at this point. For instance, Renault (OTCPK:RNLSY) is far more dependent on EU sales than Daimler (DMLRY). The risk to Renault is, therefore, potentially more immediate and higher than it is for Daimler. The US and other assets will eventually also see a downturn because there will be contagion effects, including a drop in exports to the EU while companies that produce and sell goods and services in the EU will take a major hit. The global investment environment is set to take a hit eventually as a result of an EU-wide crisis, even if at some point financial outflows will initially make it seem like a good thing that will further boost major alternative markets.

Gazprom will be an obvious winner in all this, as natural gas prices are increasing its profit margins. Its second quarter earnings were already positively impacted by the higher natural gas prices. Things are likely to get even better in coming quarters, and it increasingly looks like investors are waking up to this fact, based on its recent stock performance. LNG suppliers are also set to see a boost in revenues. Western LNG suppliers, however, may not benefit as much as we see with Gazprom, especially when it comes to their stock performance. Fears of green initiative penalties on their longer-term outlook have long-term investors spooked and taking advantage of any upward momentum to get rid of their positions. Shell (RDS.A) (RDS.B) has been a classic example of this trend lately. Cheniere (LNG) may be a better bet, because it is all about LNG exports and it may escape environmentalist activism to some extent, given that it does not have a very prominent corporate profile outside the investment community. Its only problem may be the rising cost of US shale gas, given that the shale boom is now pretty much over.

A final observation I would like to make is the effect that such a crisis will have on Central Bank decisions. The ECB will have little choice but to allow for inflation to rise higher in order to prevent a debt crisis as national governments will find themselves needing to spend more money in order to address resulting social issues. In other words, it will continue its expansionary monetary policies, which will drive the Euro down. Most major competitors and partners will have to follow suit in order to prevent their own currencies from getting too strong in relation to the Euro, which would hurt their exports. The end result can end up being unstoppable inflation, worldwide. This will, on one hand, be positive for stock prices in nominal terms. On the other hand, an economic crisis will have a dampening effect on the real value of revenues and profits when adjusted for inflation.

It is still possible that the EU will once again muddle through and solve the impending energy price crisis it is faced with this winter. An agreement with Russia, which would have to happen soon in order to make a difference would go a long way. Perhaps the weather will play in its favor and the wind will blow harder in the coming months, even as temperatures will be milder than expected this winter. In the absence of wise policy decisions, namely, reach out to Russia and do it right away, if they did not already, or just plain luck in regards to favorable weather patterns coming to the rescue just at the right time, there will be a severe crisis. It will be a crisis that will manifest itself perhaps in ways that can be expected, with the symptoms more or less following along the path I laid out. It can also manifest itself in unpredictable ways that no one might expect. Regardless, investors need to keep an eye on this, because it has all the makings of a perfect economic storm and it will affect the investment environment.