Sunshine Seeds/iStock via Getty Images

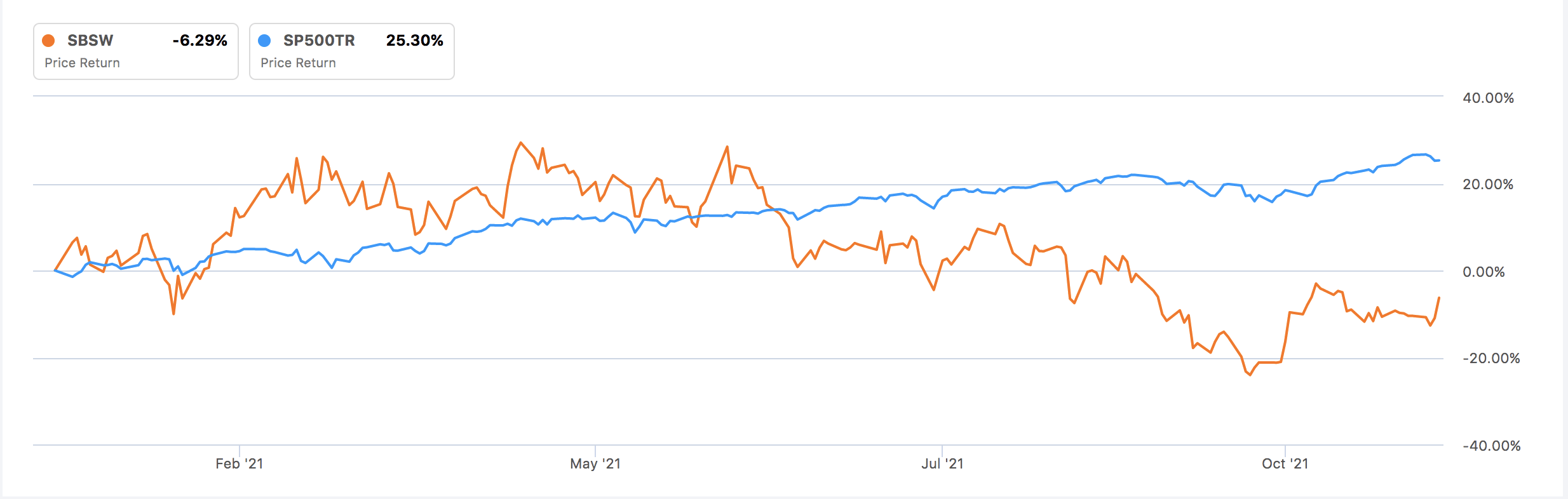

Sibanye Stillwater stock (NYSE:NYSE:SBSW) probably hasn't had the most bullish of times, considering it has paid a considerable amount of its cash flow to stockholders in the form of dividends.

Furthermore, the company has faced headwinds such as geopolitical risk, stagnation in commodity prices, and disruption of the commodity cycle due to China's hard-line leverage policies.

After careful consideration, we think this is the ideal time to invest in Sibanye stock. For an in-depth company overview, take a look at one of our previous articles.

Recent Performance

The stock has retraced a tad as it paid out a mass amount of dividends with a payout ratio of 45.07% during the past half-year. There's also been an issue of stagnating commodity prices after an initial surge earlier in 2021, which has halted the stock price's progress.

Sibanye reported a 10% rise in EBITDA during Q-3. Leading the charge was Gold production, which has increased by 1.7% year-over-year at an average price of $1781 per ounce.

The mining house reiterated its full-year gold production of 884K-948K ounce; however, it experienced raised sustaining costs to $1,690-$1,742/oz due to increased electricity tariff costs and rising input costs.

All considered it's fair to say that it's been a rough patch for Sibanye that's been unjustified.

Developments and Trajectory

Sibanye's dominance in platinum group metals has allowed it to facilitate any potential demand for renewable energy due to its by-products. The mining house has chosen to leverage its bet by investing in further sustainable exploits.

Recently, the firm closed a deal for a Nevada lithium project, which it paid $490 million for, and the agreement includes a further $50 million investment for 50% in an additional project. Sibanye's sharing the current rights and potential rights with Nevadan company ioneer (OTCPK:GSCCF). It's thought that Sibanye actually got the good end of the stick here as its capital injection is somewhat of a realization savior of the project/s.

Further to these deals, Sibanye is also nearing significant acquisitions in Brazil. The firm is in the process of acquiring Atlantic Nickel, which operates one of the largest open-pit nickel mines in the world; in addition, Sibanye's due to acquiring Mineracao Vale, which is developing a copper and gold mine.

We're also in favor of Sibanye's trajectory in deep mining. The planned abandonment of the Kloof and Beatrix gold mines means the company's pivoting towards the future of less deep, less expensive mines.

Finally and most importantly, the PGM (Platinum Group Metals) division is doing well. In Rustenburg, Sibanye has claimed the UG2 and Merensky reefs as a consequence of its Lonmin acquisition.

Platinum Group Metals is a very lucrative business at the moment due to the scarcity of Platinum and the renewable energy prospects of its by-products. Sibanye certainly has a strong foothold in the platinum space, being the largest producer in the world.

Valuation & Momentum

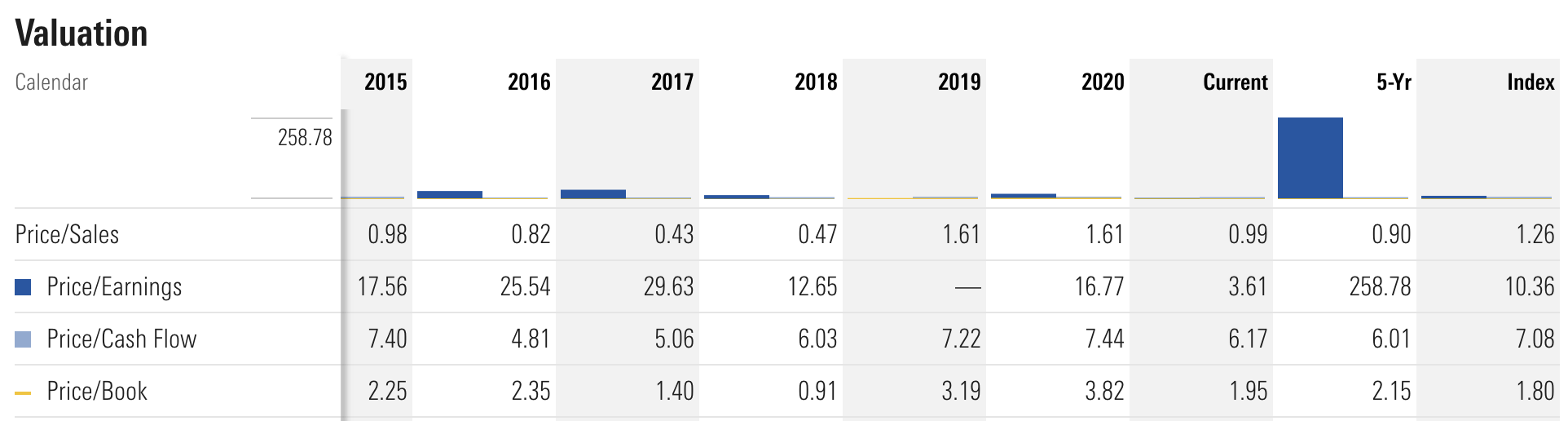

Whether we're in a cyclical upturn or not, Sibanye stock is significantly undervalued according to its valuation metrics.

The price to sales ratio isn't just below its 5-year average; it's also below the generally accepted over/undervalued threshold of 2.00. Furthermore, we're looking at a stock with a P/E ratio well below the index and 5-year average, and if we consider a PEG ratio of 0.01, it's evident that the company's earnings are growing much faster than its stock price.

As an add-on Sibanye's price to sales is also trading at a 91.69% sector to the discount while its price to cash flow is also trading at a discount, signaling that there's value in abundance.

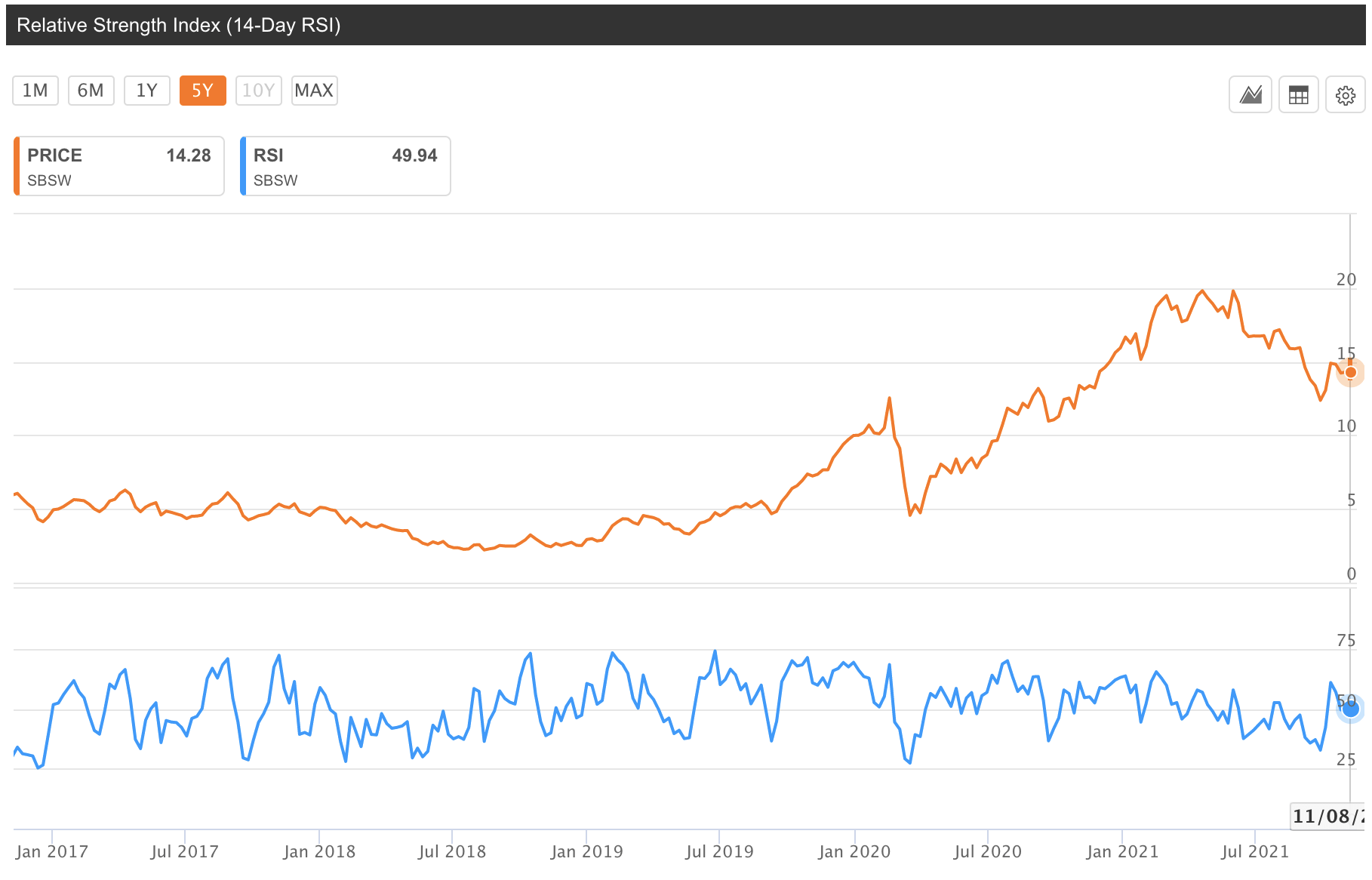

The stock has just exceeded its 10-, and 50-day moving averages indicating a momentum pattern. I wouldn't say that the stock is oversold, but an RSI of 49.94 is well below recent highs, and I wouldn't be surprised if there's an uptick in the near future, which would cause stock price appreciation.

Dividends

| Dividend Yield | 11.07% |

| Cash From Operations | 1.82B |

| Interest Coverage | 32.30 |

Source: Seeking Alpha

First of all, let's concede that a dividend yield of 11.07% is ridiculous, and it's mouth-watering. If a stock is trading at that high of a yield, it could usually mean that it's undervalued and the equity residual is abundant.

Will that yield be ascertained? Well, that depends on how high the stock price moves, but even if it moves higher, Sibanye has cash from operations at 126.87% higher than its 5-year average and a free cash flow yield of 17.21%.

Why is this important? Well, many think that dividends get paid out of net income, but it actually originates from operating cash flow according to U.S. GAAP accounting standards. If cash flows continue to grow at this rate, dividend-seeking investors will be satisfied for years regardless of stock price appreciation.

Finally, the interest coverage ratio is astronomical, meaning there won't be any unforeseen refinancing of debt, which could dent dividend payments. Sibanye is a fantastic dividend play as things stand.

Risks

Mining stocks are cyclical, and the boom in platinum group metals could have been one of the decisive factors in Sibanye's stock price rise. As inflation calms down into 2022, it remains to be seen whether the stock will maintain its year-over-year performance.

Another risk to look out for is Sibanye's Lithium exploits. The company has spent a significant amount of capital on greenfield lithium projects in Europe and Nevada. Lithium will obviously be in high demand moving forward, but it's easy to produce (it's basically a dam of differentiated water laying there), and we're not keen on the company allocating a significant amount of its budget towards it; we'd rather it stock to PGM, which is difficult to mine but very rewarding.

Final Word

Sibanye stock has had a drawdown due to dividend payouts. Another component of the drawdown has also been due to geopolitical risks that we've mentioned in previous articles. The stock is undervalued and remains a quality dividend play as things stand.