SB/iStock via Getty Images

Earnings of First Internet Bancorp (NASDAQ: NASDAQ:INBK) will benefit from organic loan growth on the back of the economic recovery. Further, the upcoming acquisition of First Century Bancorp will boost earning assets, lower deposit costs, and save operating expenses, which will support the bottom line. On the other hand, a higher provision expense and one-time restructuring charges will drag earnings this year. Overall, I'm expecting First Internet Bancorp to report earnings of $4.40 per share in 2022, down from anticipated earnings of $4.65 per share for 2021. Despite the anticipated decline, the earnings for 2022 will likely still be much higher than the pre-pandemic level. The year-end target price suggests a decent upside from the current market price. Therefore, I'm adopting a bullish rating on First Internet Bancorp.

Outlook on Organic Growth has Improved

First Internet Bancorp’s loan portfolio declined by 4% in the first nine months of 2021. The declining trend will most probably turn around soon because of promising signs visible in the third quarter. The management mentioned in the earnings presentation that its commercial loan pipelines, driven by small business, franchise finance, and construction, were quite robust. In fact, commercial pipelines were up 65% over the second quarter of 2021.

Within commercial loans, the management expects to fund $150 million of franchise finance loans during 2022. To put this number in perspective, $150 million is around 5% of total loans at the end of September 2021. Further, the management mentioned in the conference call that the commercial real estate construction team has several new opportunities in the pipeline due to which the management expects unfunded commitments to increase by an additional $100 million in the fourth quarter. According to the management, these construction projects typically fund over 12 to 24 months. Furthermore, the management expects to originate $215 million of small business loans, SBA 7(a), in 2022. To put this number in perspective, $215 million is around 7% of total loans at the end of September 2021.

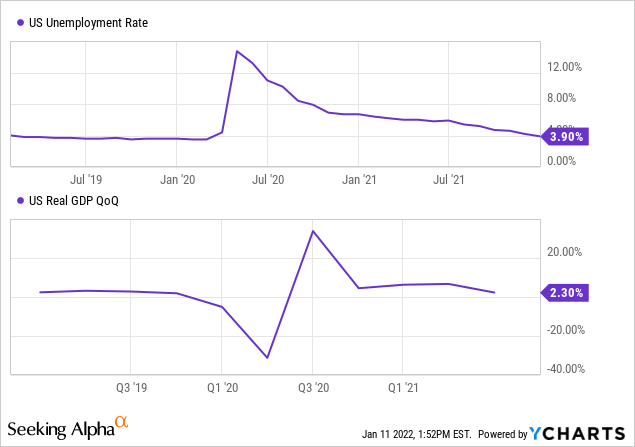

Further, macroeconomic trends appear promising. First Internet Bancorp is a nationwide lender; therefore, the country's GDP and unemployment rates are good metrics to gauge the credit demand. Both metrics have been positive as of late, which bodes well for First Internet Bancorp's credit demand.

Acquisition to Boost Earning Assets, Lower Funding Cost

First Internet Bancorp plans to acquire First Century Bancorp, a technology-driven financial solutions company with lines of business focused on payments, tax product lending, sponsored card programs, and homeowner’s association (“HOA”) services. First Internet Bancorp will pay $80 million in cash as consideration, as mentioned in a press release. The transaction’s expected date of closing has not been disclosed as yet. The merger and acquisition presentation takes two cases for closing dates, with one being March 31, 2022, and the other being December 31, 2022. To be on the safe side, I'm assuming a closing on September 30, 2022, which means my earnings estimates incorporate the acquisition benefit for only one quarter of this year.

According to details given in the merger presentation, First Century Bancorp’s loans totaled $32 million, total assets totaled $408 million, and deposits totaled $330 million at the end of September 2021. Due to the small proportion of loans in total assets, First Century had a lot of excess liquidity. First Internet Bancorp will use around $150 million of the excess liquidity to retire INBK’s high-cost deposits. Further, the company will deploy around $150 million into securities at yields of around 1.5%. Although it would have been better if the target had more loans, this transaction is still beneficial because First Internet Bancorp will get rid of its excess cash earning an average yield of only 0.31%, and gain securities earning around 1.5%. Similarly, the liability side will also improve because First Internet Bancorp will be able to retire its higher-cost deposits. Further, First Century Bancorp had a total cost of funds of only six basis points at the end of September 2021, as mentioned in the merger presentation. In comparison, First Internet Bancorp’s funding cost was 1.28% in the third quarter, as mentioned in the 10-Q filing.

To summarize, the acquisition will benefit First Internet Bancorp’s top line in the following ways.

- Reduce excess cash balances by $80 million that are carrying estimated yields of around 0.31%.

- Add $150 million of securities earning 1.5%, which will increase total securities by 24%.

- Reduce high-cost deposits by $150 million, or 5% of total deposits.

- Add low-cost deposits of $330 million with an average funding cost of only six basis points.

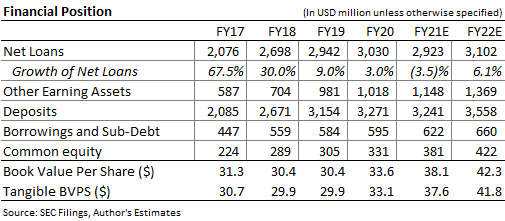

Considering the factors driving organic and acquired growth, I'm expecting loans to increase by 6%, securities and other earning assets to grow by 19%, and deposits to grow by 10% in 2022. The following table shows my balance sheet estimates.

SEC and Author's Estimates

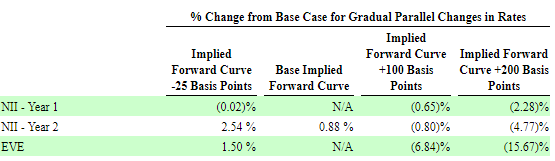

Unlike most other banks, First Internet Bancorp's books are positioned in a manner such that the net interest margin gets reduced in a rising interest-rate environment. According to the management’s interest-rate sensitivity analysis, a 100-basis points increase in the interest rate can reduce the net-interest income by 0.65% over twelve months. The table below shows the results of the management’s interest-rate sensitivity analysis.

As a result, a rising interest-rate environment will likely counter the benefit of the acquisition of First Century Bancorp. Overall, I'm expecting the margin to increase by only four basis points in 2022.

Expecting Provision Expense to Normalize After Further Reserve Releases

First Internet Bancorp’s provisioning for loan losses remained subdued in the first nine months of 2021. The provisioning will likely remain subdued through early 2022 because the allowances appear excessive relative to nonperforming loans. Allowances made up 0.95% of total loans, while nonperforming loans made up 0.27% of total loans at the end of the last quarter, as mentioned in the earnings presentation. As a result, provision reversals will likely remain elevated through early 2022.

However, the provision expense will likely increase this year relative to 2021 because of higher loan growth, as discussed above. Overall, I'm expecting the provision expense, net of reversals, to make up around 0.19% of total loans in 2022. In comparison, the net provision expense made up around 0.23% of total loans from 2016 to 2019.

Expecting 2022 Earnings of $4.40 per Share

The anticipated organic growth in loans, margin expansion, and benefit from the acquisition will likely drive earnings this year. Further, the management expects to achieve cost savings of $1.8 million annually, or around 15%, from the acquisition of First Century Bancorp, as mentioned in the merger presentation.

On the other hand, a higher provision expense will constrain the bottom line. Further, First Internet Bancorp expects to incur a one-time restructuring charge of $6.5 million due to the acquisition of First Century Bancorp, as mentioned in the merger presentation.

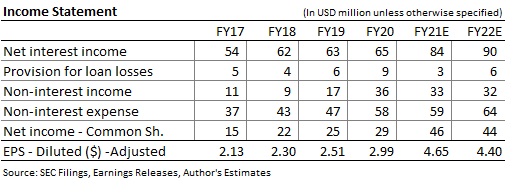

Overall, I'm expecting the company to report earnings of $4.40 per share in 2022. For the last quarter of 2021, I'm expecting the company to report earnings of $1.08 per share, which will take full-year earnings to $4.65 per share. First Internet Bancorp is scheduled to announce its fourth-quarter results on January 19, 2022. The following table shows my income statement estimates.

SEC Filings and Author's Estimates

Actual earnings may differ materially from estimates because of the risks and uncertainties related to the COVID-19 pandemic, especially the Omicron Variant.

Year-End Target Price Suggests a Decent Potential for Capital Appreciation

First Internet Bancorp is offering a dividend yield of only 0.5% at the current quarterly dividend rate of $0.06 per share. The company has maintained its quarterly dividend at this level since 2013. Although the expected payout ratio for 2022 is only 6%, I’m not expecting a hike in the dividend rate because the company has not made any indication that it will break its tradition any time soon.

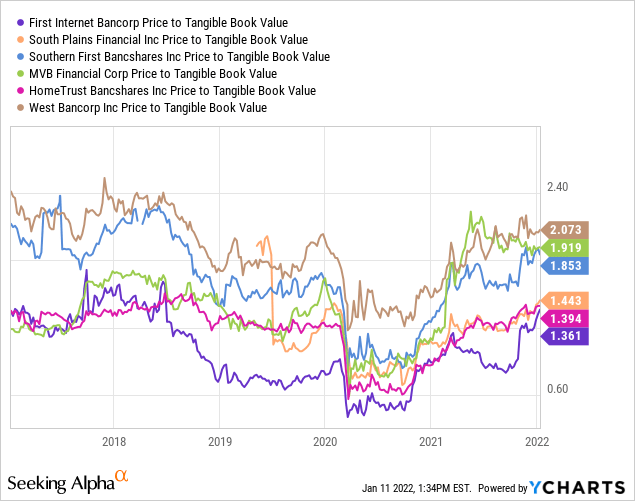

I’m using the peer price-to-tangible book (“P/TB”) and historical price-to-earnings (“P/E”) multiples to value First Internet Bancorp. The stock’s historical P/TB ratio has been unreasonably low in the past; therefore, I have decided to take the peer average.

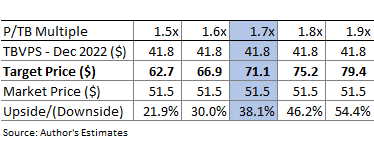

Multiplying the average P/TB multiple with the forecast tangible book value per share of $41.8 gives a target price of $71.1 for the end of 2022. This price target implies a 38.1% upside from the January 10 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

Author's Estimates

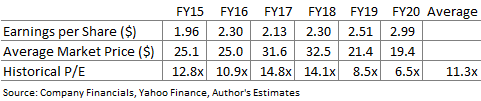

The stock has traded at an average P/E ratio of around 11.3x in the past, as shown below.

Author's Estimates

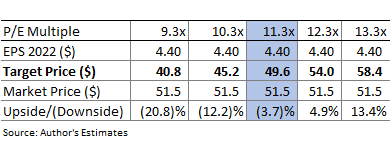

Multiplying the average P/E multiple with the forecast earnings per share of $4.40 gives a target price of $49.6 for the end of 2022. This price target implies a 3.7% downside from the January 10 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

Author's Estimates

Equally weighting the target prices from the two valuation methods gives a combined target price of $60.3, which implies a 17.2% upside from the current market price. Adding the forward dividend yield gives a total expected return of 17.7%. Hence, I’m adopting a bullish rating on First Internet Bancorp.