mammuth/E+ via Getty Images

Investment Thesis

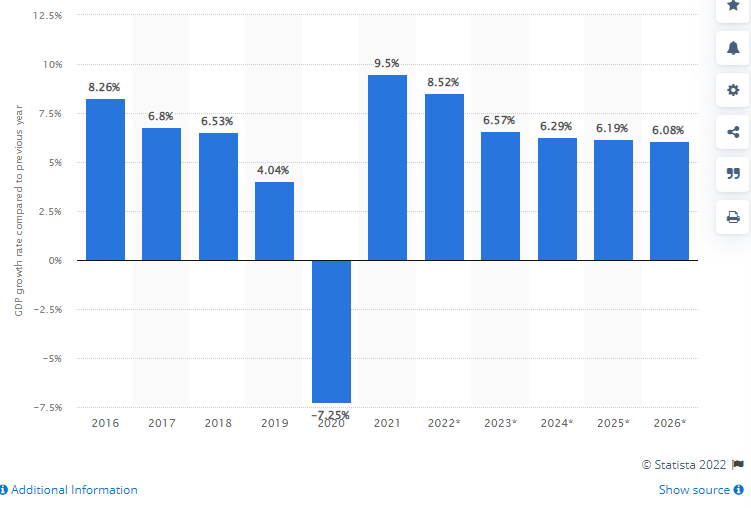

According to Statista, the Indian economy is expected to grow at mid-single-digit rates up until 2026. Therefore, India should grow faster in the future than the US and most European countries.

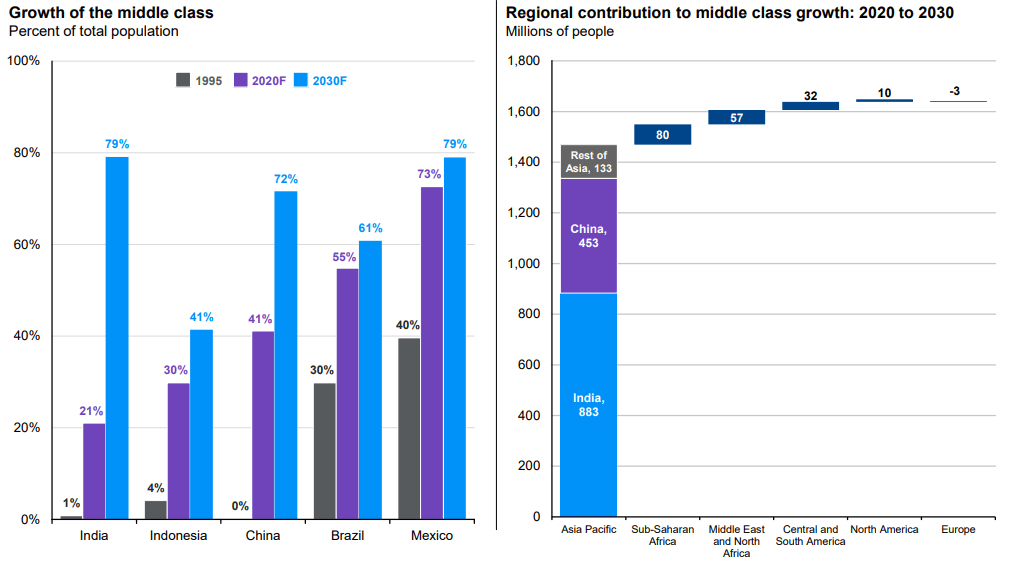

This growth is supported by strong fundamentals. For instance, India is expected to have the highest middle-class growth rate in the world over the next decade. To put it into perspective, more than 880 million people will be lifted out of poverty by the end of the decade.

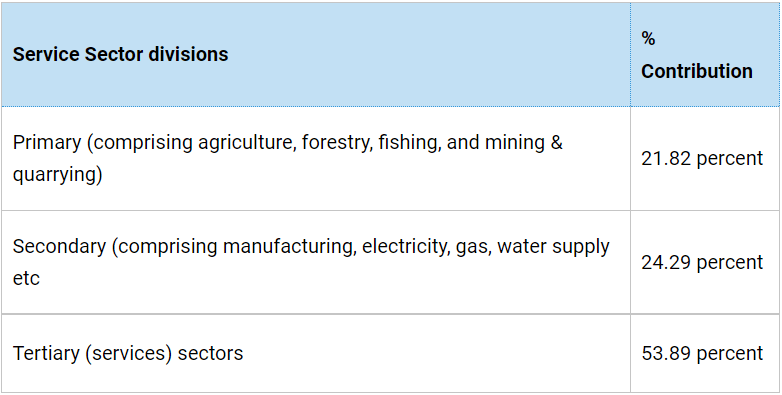

Furthermore, despite being considered as an emerging market, India offers highly qualified workers. For instance, India dominates the global outsourcing market and derives approximately 54% of its domestic product from tertiary sector activities.

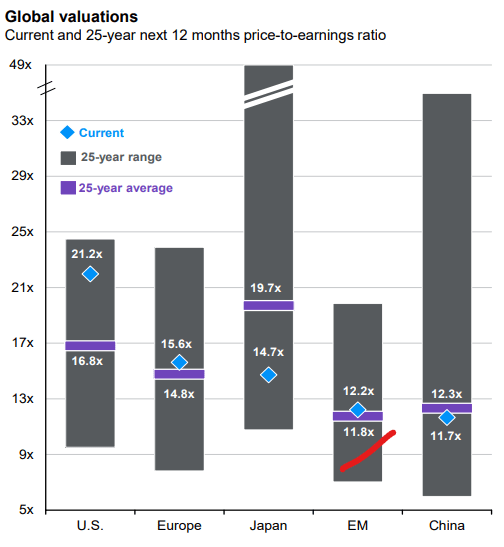

Despite the exciting tailwinds, the Nifty 50 index, which tracks the 50 largest Indian companies, trades at ~25x earnings and has a dividend yield of 1.13%, which is way more expensive than the emerging market P/E average of 12.2. In this article, I will be reviewing the Invesco India ETF (NYSEARCA:PIN) which provides exposure to a basket of Indian equities, and more broadly, to the Indian economy.

Strategy Details

The Invesco India ETF tracks the performance of the FTSE India Quality And Yield Select Index. The Index is constructed by evaluating all securities in the FTSE India Index and first excluding securities in the bottom 10% based on their 12-month trailing dividend yield. Of the remaining securities, those ranked in the bottom 10% by their quality scores are also then excluded.

If you want to learn more about the strategy, please click here.

Portfolio Composition

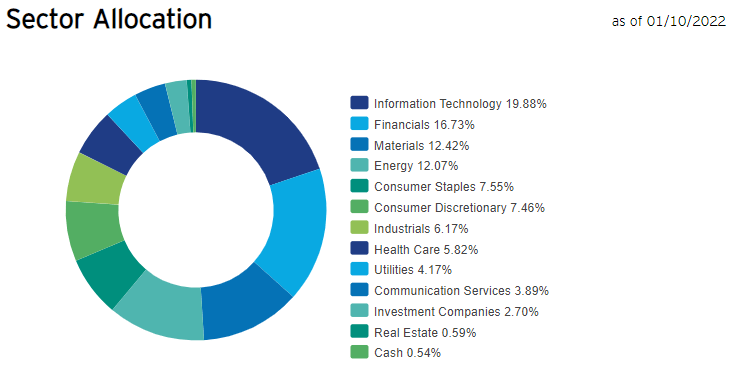

From the sector allocation chart below, we can see that the index places a high weight on Information Technology (representing around 19.88 % of the index) followed by Financials (accounting for 16.73% of the index) and Materials (representing around 12.42% of the fund). The largest three sectors have a combined allocation of approximately 49%. I like the fact that the ETF is well diversified, with no single sector accounting for more than 20% of the total fund. In terms of geographical allocation, PIN invests in India.

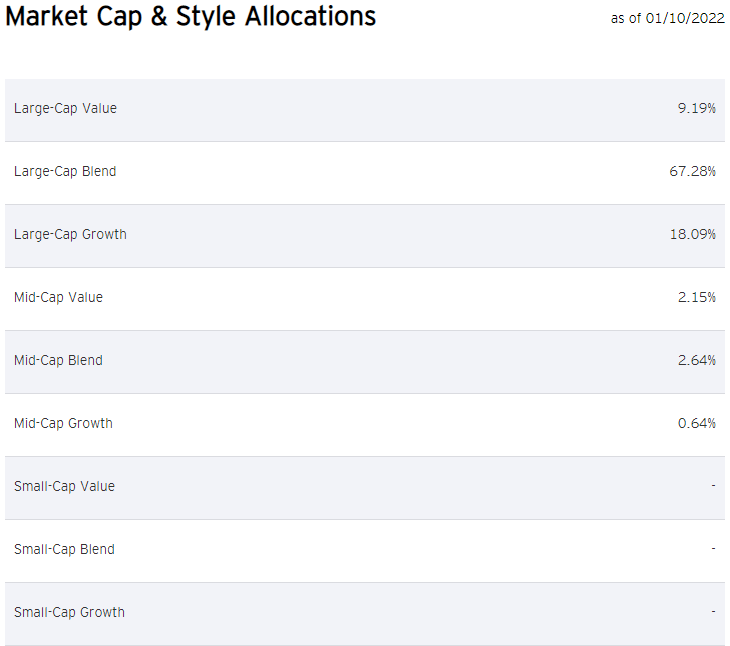

PIN invests over 67.28% of the funds into large-cap blend issuers, characterized as large-sized companies where neither growth nor value characteristics predominate. Large-cap issuers are generally defined as companies with a market capitalization above $8 billion. The second-largest allocation is large-cap growth equities at ~18% of the fund. This ETF allocates 94.56% of the funds to large-caps and nothing to small-cap equities, which generally have a larger runway to compound than large-cap issuers. I think it is important to see how that fits your investment goals.

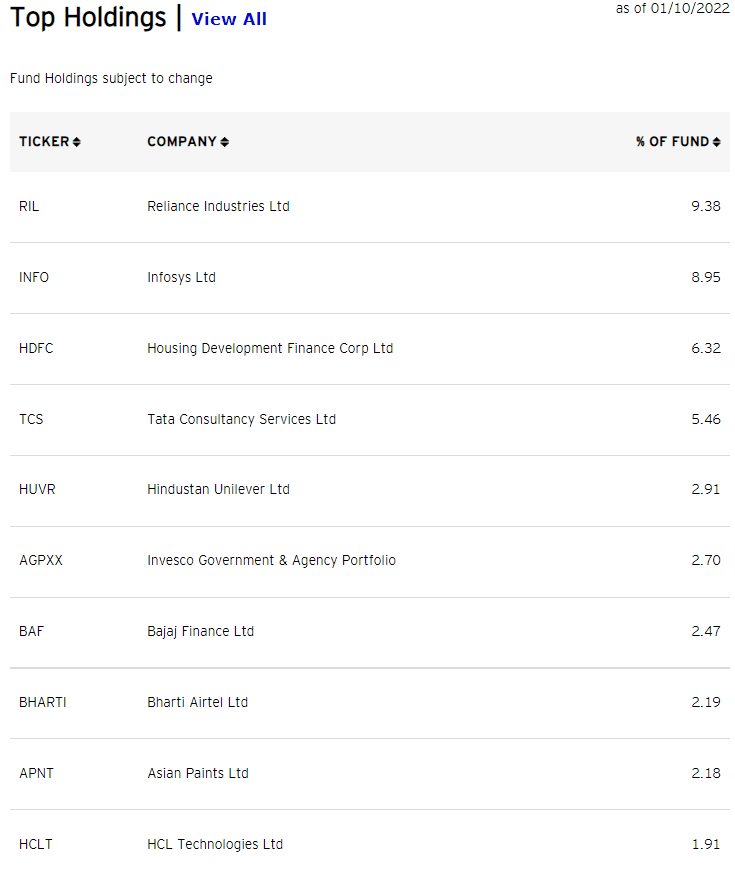

The fund is currently invested in 141 different stocks. The top ten holdings account for 44.47% of the portfolio, with no single stock weighting more than 10%. All in all, I would say that PIN is pretty well-diversified across issuers.

Since we are dealing with equities, one important characteristic is the valuation of the portfolio. According to Invesco, the fund currently trades at an average price-to-book ratio of 3.70 and at an average forward price-to-earnings ratio of 22.16. In addition to that, the portfolio has a return on equity of 22.95%. I generally consider a company trading at a forward price-to-earnings ratio above 20 to be richly valued. That said, I think there are some exceptions where you can pay a premium for an outstanding business that delivers a high return on capital and has good growth prospects. In PIN's case, these companies generate a high return on equity (close to 23%) which could explain why the market is paying a premium for these stocks.

Is This ETF Right for Me?

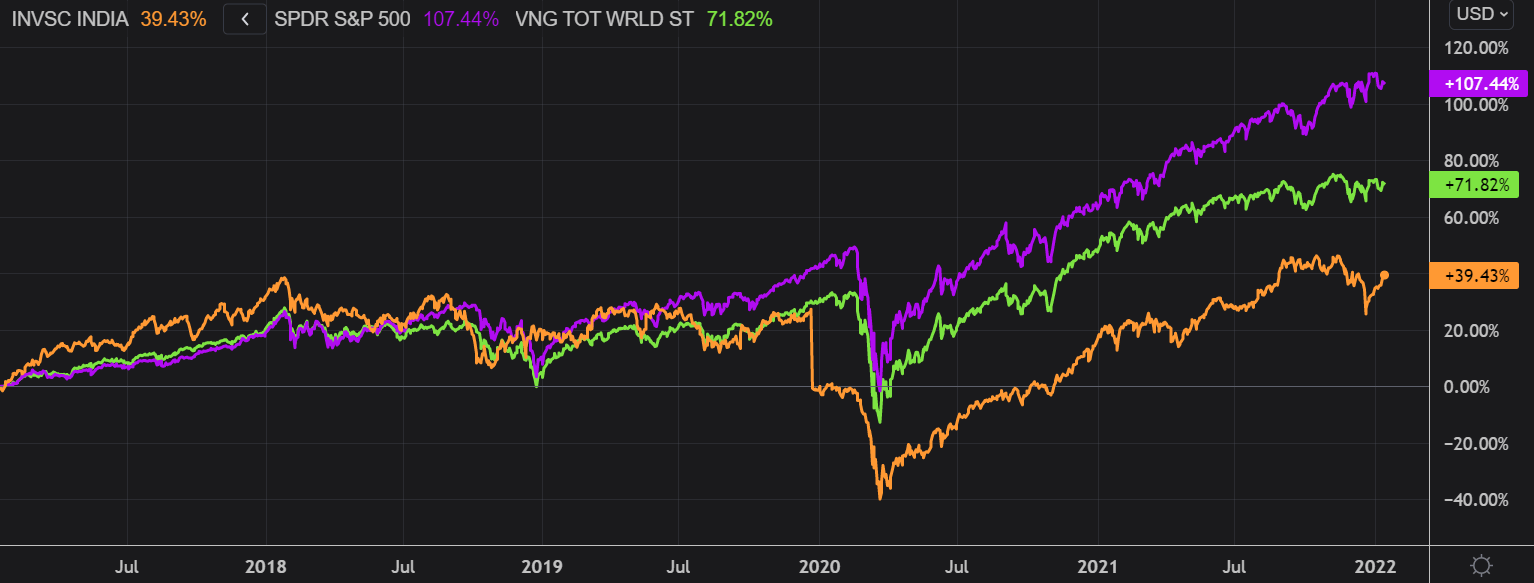

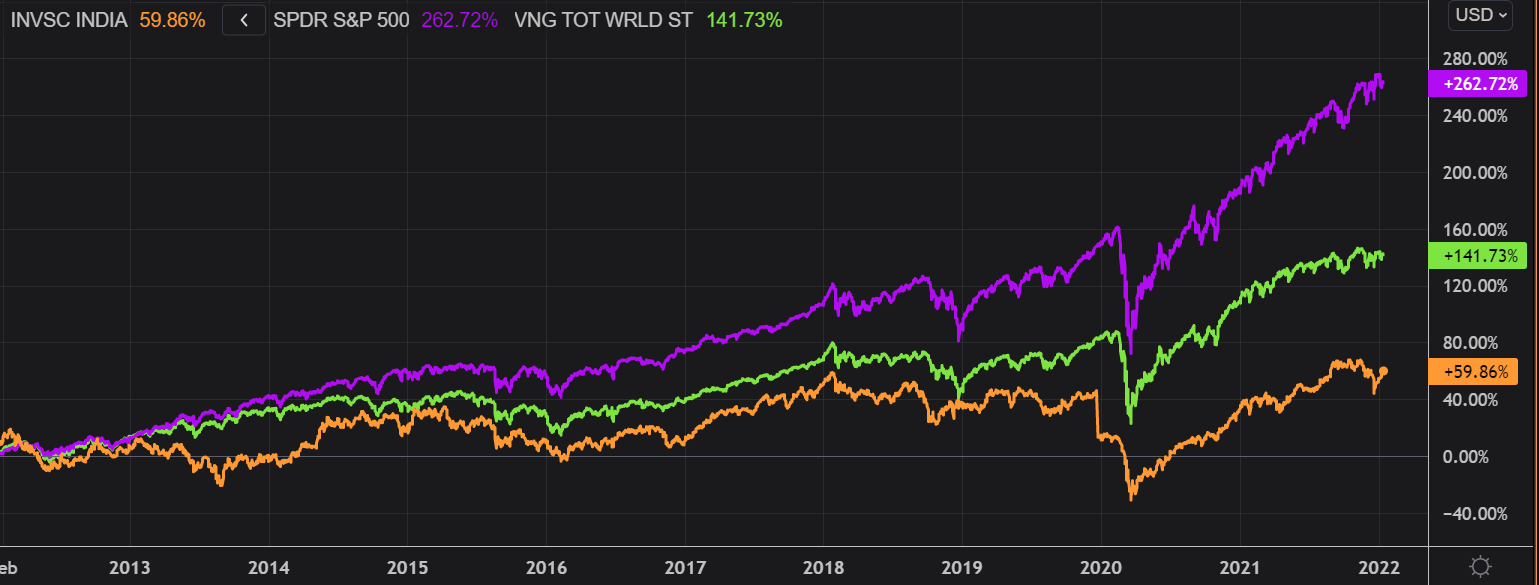

In terms of capital appreciation, PIN disappointed long-term when compared to other international indices. I have measured below the price performance of PIN against the price performance of the SPDR S&P 500 Trust ETF (SPY) and the Vanguard Total World Stock ETF (VT) over a 5-year period to assess which one was a better investment. Over the five-year period, PIN failed to beat both strategies, although it is important to note that the major divergence in performance happened after the COVID-19 pandemic, which was an excellent period for US equities. All in all, PIN delivered mediocre results for long-term investors that purchased this ETF five years ago. To put it into perspective, a $100 investment in PIN five years ago would now be worth $139.43. This represents a compounded annual growth rate of 6.8%.

Refinitiv Eikon

The result doesn't change much from a 10-year perspective. SPY and VT came once again on top. However, I think that past results are a poor proxy to estimate future returns. Given the solid growth prospects of the Indian economy, it is possible PIN will outperform going forward.

Refinitiv Eikon

Lastly, this is a dividend-paying ETF and it can be suitable for the income investor. However, it is important to mention that the frequency of payments and the dividend amount are highly volatile. For instance, PIN paid a total of $1.86 per share in dividends in 2021 and only $0.167 in 2020.

Key Takeaways

India is likely to grow faster than the majority of western economies. Given the fact that GDP growth is a key driver for equity market performance, I think that investing in India today is appealing to investors that wish to diversify their portfolio beyond developed markets. In my opinion, PIN provides a good exposure to the Indian economy and good diversification across sectors and issuers. I would personally like to see some exposure to small-cap equities but I'm sure that this can be added in the future. On the valuation side, I think the index is expensive at the moment and does not offer any emerging market risk premium. As a result, I think it is better to wait for a 10-20% pullback in Indian equities before purchasing PIN.