krblokhin/iStock via Getty Images

Alico, Inc. (NASDAQ:ALCO) is one of the United States' leading citrus producers. They have been in the agricultural industry for over 62 years. The company has a variety of citrus products, including oranges, grapefruit, and lemons, and is headquartered in Florida. As of this writing, the company has a market capitalization of $314.62 million and is in the midst of its fourth dividend payment after achieving a remarkable 177% dividend rise from its Q1 2021 quarterly rate of $0.18. This firm has a forward dividend yield of 4.80% and a payout ratio of 29.76%.

Orange juice consumption is declining in the US, which may reduce demand, and citrus prices in Florida may increase as a result of the USDA Agricultural Statistics Board's forecast of low orange production. This could have a negative impact on its affordability in today's high inflation environment. Waiting for a meaningful pullback is therefore a viable strategy to consider.

Alico Citrus and Concerns

ALCO has two operating divisions, Alico Citrus and Land Management and Other Operations, with Alico Citrus contributing 98% of revenue in Q2 2021. According to management, they offer early-to-mid season and Valencia oranges to processors who transform the majority of their harvested citrus crops into orange juice. They also sell fresh fruits by the box and provide caretaking services for third parties.

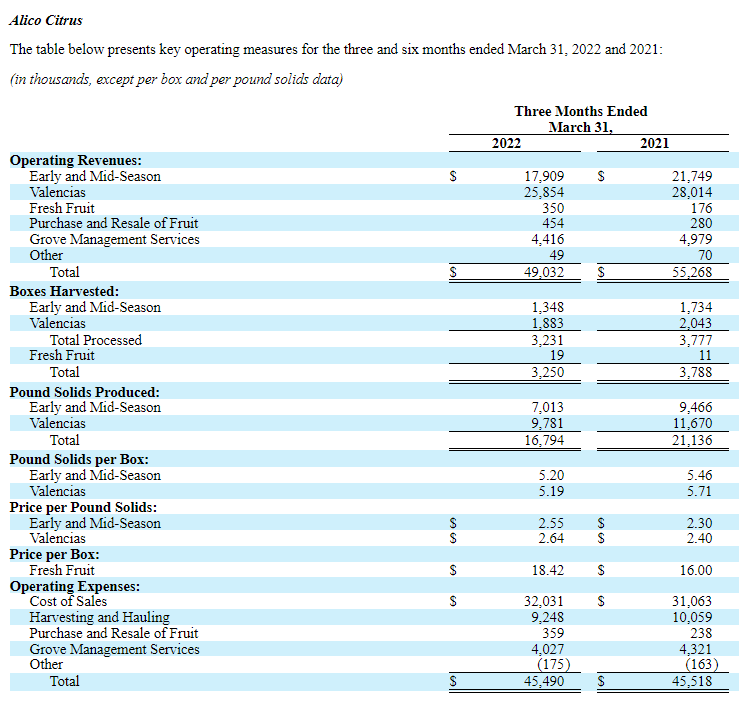

ALCO: Alico Citrus Segment's Revenue (Q2 2022 Financial Report)

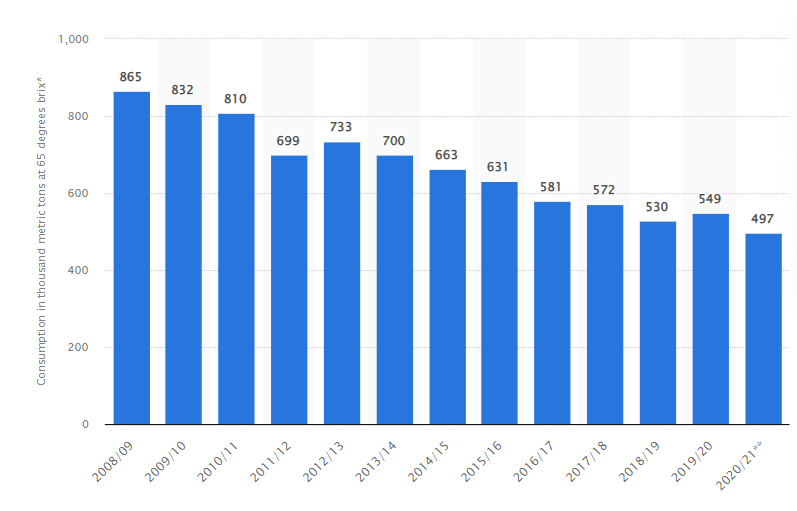

Looking at its performance as of this quarter, ALCO's operational revenue of $49.032 million, down from $55.268 million, indicates a troubling trend. This is mostly due to slower box harvesting, as depicted in the image above, compared to the company's Q2 2021, and even a price increase is insufficient to deliver a positive figure. Moreover, despite a decline of 11.28% in its top line, we can detect an increase in its cost of sales and a relatively flat figure in its total operating expense compared to Q2 2021. If this trend continues, it will be difficult for the company to maintain profitability in the future. In addition to this catalyst, orange juice consumption in the US is decreasing, as depicted in the graphic below.

Orange juice domestic consumption in the United States from 2008/09 to 2020/21 (Statista.com)

Prior to the onset of the pandemic, orange juice consumption was on a downward trend, and given the current consumer budget constraints brought on by high inflation and pandemic-related uncertainty, it will be difficult, in my opinion, to reverse this trend, especially as the price of citrus fruits continues to rise.

Another Set of Concerns

Prior to writing this analysis, I first became aware of ALCO in their Q4 2021 report, in which the management forecasted a generous adjusted net income of around $5.4 million and $7.1 million for FY2022. This is approximately $6.25 million on an average basis, which is flat compared to its normalized net income of $6.5 million recorded in the prior fiscal year and better than its $2.1 million reported in FY2020. Upon revisiting the stock this quarter, it appears that the strong catalyst is challenged by the company's current estimate of negative adjusted net income in the range of -$4.1 million to -$2.3 million for FY2022. In addition to this profitability risk, analysts have a negative valuation forecast for ALCO.

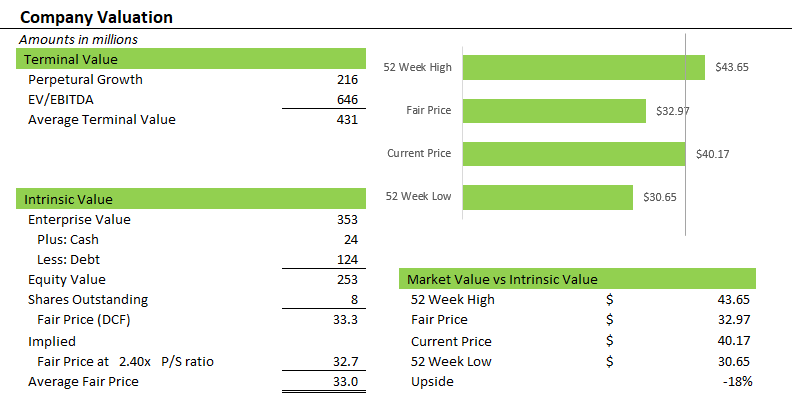

ALCO is Not Cheap as of the Moment

ALCO: Company Valuation (Prepared by InvestOhTrader)

ALCO is not cheap as of the moment in comparison to my fair price target of $33 which is obtained from the average of the DCF model and simple relative valuation. ALCO presently trades at a trailing P/E ratio of 5.52x and when we compare it to its forward estimates, we can find a higher figure of 8.74x and looking further at its estimates for FY2023 of 48.40x, we can say that ALCO is overvalued as of this writing.

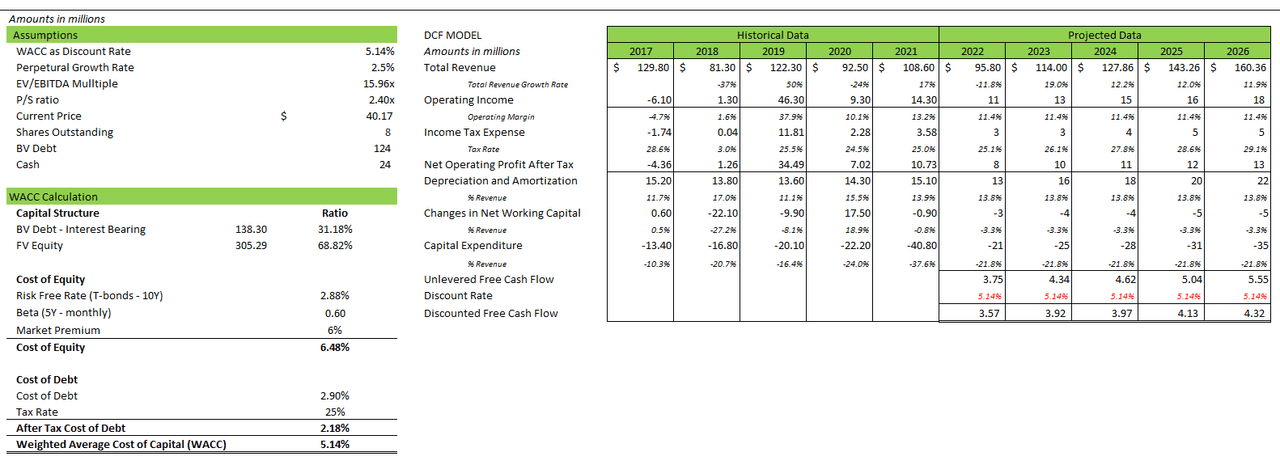

ALCO: DCF Model (Data from Seeking Alpha and Yahoo! Finance. Prepared by InvestOhTrader)

Here are my assumptions depicted in the image above. I used the analysts' forecast for FY2022 and FY2023 and projected a continuing growth of 11.9% by the end of the model with the assumption of normalization of harvesting seasons and continued shift of consumers to healthy lifestyles. I used a constant 11.4% operating margin to forecast a growing operating income to $18 million by FY2026. I use a WACC of 5.14% as my discount rate to arrive at a generous $33.3 intrinsic value. I believe this is quite generous, compared to its target adjusted EBITDA ranging between $13 to $16 million for FY2022. However, as a small company, potential merger and acquisition activities may change its topline projection drastically, investors and traders should monitor.

Near Logical Resistance

ALCO: Weekly Chart (TradingView.com)

As depicted in the chart above, ALCO is currently near its logical resistance of roughly $45 per share. With its present sentiment based on its fundamentals, I believe a price above $45 will be an excellent area to initiate a short position or unload your long position. Its simple moving averages are fanned in a bullish manner, indicating that bulls are still in control as of the time of writing. Potential bearish crossover from its simple moving average and MACD could serve as another confluence with my bearish look on ALCO. Currently, there is a short interest of 1.56% in ALCO and there are 450,000 shares available to be shorted at a borrowing cost of 0.41%.

Key Notes

On the bright side, management reassures investors that citrus fruit consumption is gaining some momentum, indicating continued growth in demand as people adopt healthier lifestyles due to the pandemic.

While consumption has dropped from its highest levels when the COVID-19 pandemic initially started back in March 2020, consumption, as reported by Nielsen data on April 9, 2022, has increased approximately 7.4% for the 24-week period ended March 26, 2022, as compared to the similar 24-week period prior to the COVID-19 pandemic. Source: Q2 2022 Earnings Call Transcript

The company's capacity to pay dividends is threatened by its negative trailing free cash flow of -$23.7 million, resulting in a worrying FCF margin of -22.77%, notwithstanding the attractiveness of its high yield. It is worth noting that, despite a lower trailer CAPEX investment of $22.90 million compared to $40.8 million in FY2021, the company nevertheless produced a negative FCF, owing mostly to a weaker cash flow from operations.

Checking the company's liquidity, ALCO's current ratio increased to 2.88x from 2.46x in the prior fiscal year. In contrast, the company's debt-to-EBITDA ratio increased to 6.26x from 4.16x in the prior fiscal year as a result of its declining profitability. On the brighter side, its debt-to-equity ratio improved to 0.47x from 0.52x in the previous fiscal year. I believe the company is still liquid and is able to finance its obligations. I believe Alico is an excellent target for short selling due to its profitability and dividend safety concerns.

Thank you for reading and stay safe everyone!