BalkansCat/iStock Editorial via Getty Images

Intro

We wrote about Xerox Holdings Corporation (NASDAQ:XRX) back in March when we stated that the stock was an excellent income play. In fact, shares are basically flat since we penned that piece 10 weeks ago which actually reinforces our initial point of view for the following reason. True income-orientated investors prefer lower prices in their respective dividend stocks because compounding within the portfolio can take place at a much faster clip over standard conditions. Suffice it to say, when one can pick up more income-producing assets (stock) for the same dollar amount every month, quarter, etc., it means more income in the long run off the stated position.

However, given the high inflation environment investors are presently dealing with, earning a substantial above-average dividend yield may in fact not cut the mustard for Xerox investors. Remember, it is all about real returns going forward as nominal returns of say 5.4% (Xerox's forward dividend yield) will simply not be enough if inflation remains much higher than this figure for the foreseeable future. The issue with basing a methodology on just one metric, for example (Dividend Yield), is that the "Total Return" potential of the play is ignored to a large part which brings me to the following which is poignant for all dividend-orientated investors in the current climate.

As long as inflation runs at current high single digit levels, all dividend paying companies simply have to return more than their prevailing yields to ensure investors do not lose significant purchasing power

Therefore, from this perspective, let's look at Xerox from a "Total Return" perspective to see if we can gain insights into the future direction of this play.

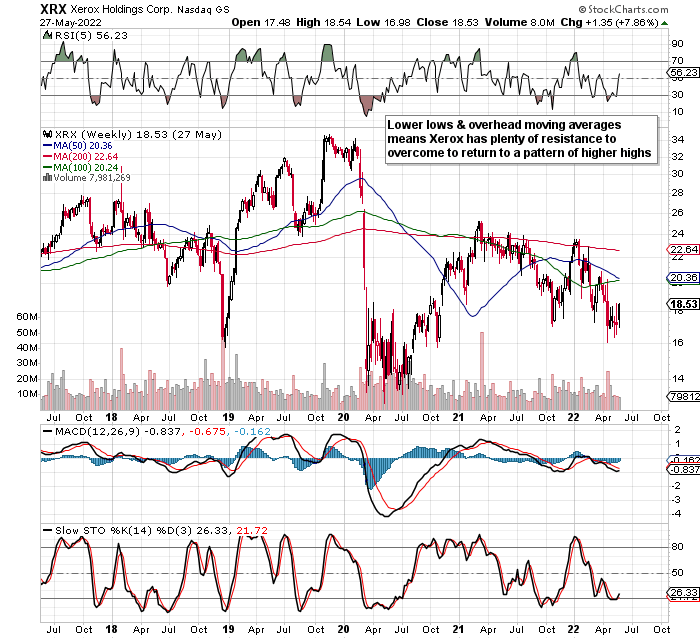

Xerox Weekly Chart (StockCharts.com)

XRX Valuation

Although shares of Xerox are not trading with a positive earnings multiple at present, the company's cash flow multiple of 4.96, book multiple of 0.69, and sales multiple of 0.46 all look ultra-attractive when compared to historic numbers. In fact, Xerox's current free cash flow yield of approximately 18% clearly demonstrates that the company has the financial clout to meet its debts and liabilities. Furthermore, the company's book and sales multiples respectively are expected to come down in this present fiscal year which basically means sales, as well as assets, are both expected to grow. Suffice it to say, growing assets and sales (which are currently cheap by any measure) is exactly the setup we look for in stocks with attractive valuations. An encouraging start to say the least.

Profitability

The reason for the negative net earnings print over the past four quarters is due to the goodwill impairment charge of $750 million in Q4 of last year. Therefore, despite Xerox's clear prowess in generating consistent free cash flow, the hefty charge to the income statement clearly demonstrates how the company's print business has been adversely impacted in recent times. This "need" for a more robust return to the office definitely shows the frailties in the print segment and how margins have been affected as a result further up the income statement. Gross margins of 33.19% over a trailing twelve-month average come in well behind the company's 5-year average number of 38.83%. Moreover, trailing operating margins of 4.4% are now less than half the company's 5-year average of 9%. These adverse margin trends mean that the bottom line earnings estimate for fiscal 2022 is now 27%+ lower than it was just 30 days ago. A worrying trend to say the least.

Shareholder Returns

Despite Xerox's profitability headwinds at present, management continues to buy back stock at a frenetic pace. At the moment of writing, the total number of shares outstanding comes to 154.86 million which means the float has dropped by almost 30 million shares already since the beginning of this fiscal year. The forward dividend yield of 5.4% does not need any introduction although the quarterly payout has been stuck at $0.25 per share for many years now. Due to strong cash flow generation, there is no problem with affordability as Xerox's cash dividend payout ratio currently comes in at 37.71% over a trailing twelve-month average. However, the company's cash balance dropped by about $700 million over the past 12 months to facilitate these returns. Suffice it to say, it is all about stronger profitability going forward as the above trends are unsustainable unless earnings are there to meet these commitments.

Conclusion

A good way to gauge the total return potential of a given stock is to monitor its valuation, profitability trends as well as shareholder compensation. We have no issue with Xerox's valuation nor how management has been rewarding its shareholders. The issue is the company's profitability which simply has to improve for the market to price this stock higher. We look forward to continued coverage.

----------------------

Elevation Code's blueprint is simple. To relentlessly be on the hunt for attractive setups through value plays trading under intrinsic value. To constantly put ourselves in positions where we have limited downside yet significant upside always remains the objective of the portfolio.

-----------------------