Sundry Photography

I was bullish about Gilead Sciences (NASDAQ:GILD) for a long time (see past articles) and always stated that a stock price of $60 was not justified. But as the stock could not really move higher for several years, one is getting frustrated and is also questioning if the thesis and analysis is correct. And even when calculating with cautious assumptions, I assumed in my articles that the intrinsic value should be at least $80 to $90.

Now as Gilead Sciences has achieved this “target” I am a bit relieved as I was obviously not a total moron about the company (and stock) but must also ask the question where Gilead Sciences could go from here.

Last Quarterly Results

Gilead Sciences surprised almost everyone with its last quarterly results (Q3/22) and the company could not only beat expectations for earnings per share by $0.47, but also revenue estimates by $900 million (about 15% above analysts’ estimates, which is a huge beat for revenue).

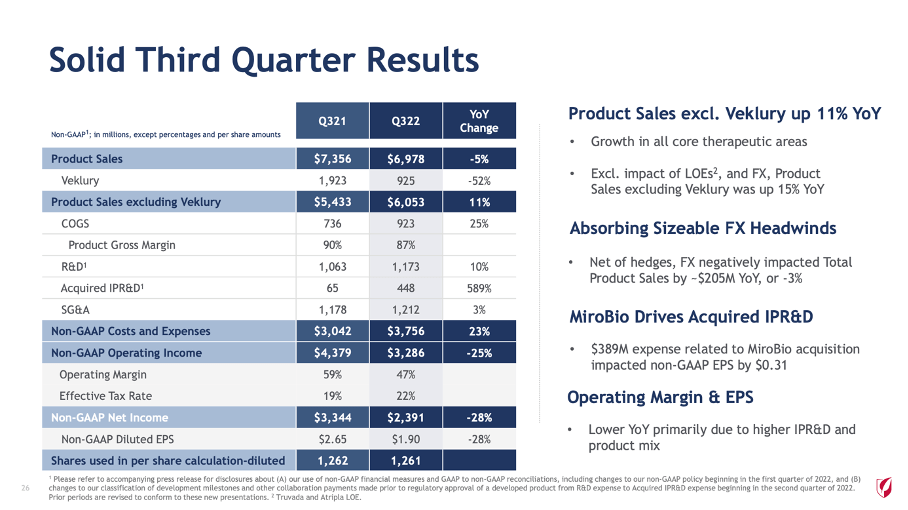

When looking at the third quarter results itself, the reported numbers are not so great. Total revenue declined from $7,421 million in the same quarter last year to $7,042 million this quarter – a decline of 5.1% YoY. Income from operations also declined from $3,842 million in Q3/21 to $2,837 million in Q3/22 – a decline of 26.2% year-over-year. Diluted net income per share declined from $2.05 in Q3/21 to $1.42 in Q3/22 – a decline of 30.7% year-over-year.

Gilead Sciences Q3/22 Presentation

When looking at non-GAAP earnings per share, we see a decline of 28.3% year-over-year from $2.65 in Q3/21 to $1.90 in Q3/22. And Gilead Sciences generated $2,706 million in free cash flow in the third quarter of 2022 – and compared to $3,114 million in the same quarter last year this is a decline of 13.1% YoY.

But before we are too harsh about Gilead Sciences and the third quarter results, we should keep in mind that Veklury sales have a huge impact on the top line (and the bottom line). And over the next few quarters, Veklury sales will most likely decline as these sales are dependent on COVID-19 related hospitalizations. When excluding Veklury sales, the top line actually increased 11% year-over-year to $6.1 billion. Veklury sales declined from $1,923 million in the same quarter last year to $925 million this quarter (also driven by lower rates of COVID-19 related hospitalizations).

Gilead Sciences Q3/22 Presentation

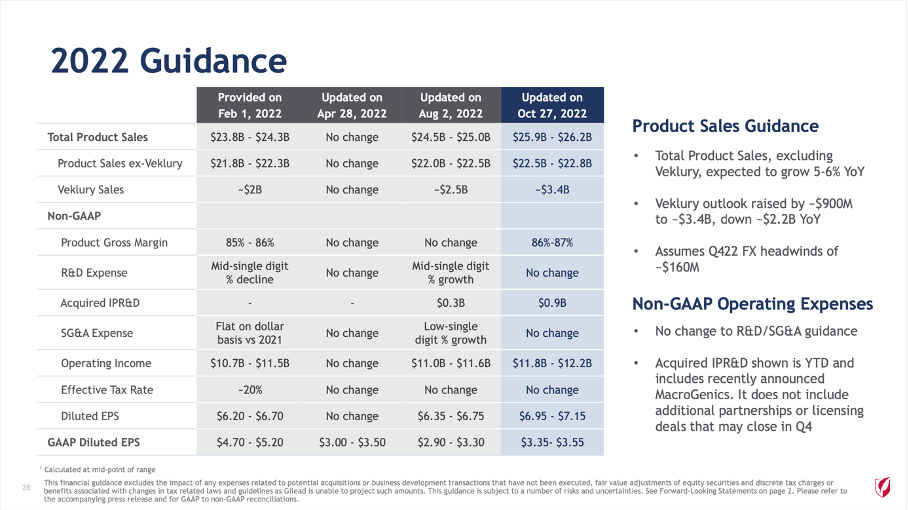

The company also raised its outlook for fiscal 2022. Total product sales are now expected to be between $25.9 billion and $26.2 billion – compared to $27.3 billion in fiscal 2021 this is still a decline, but much higher than the previous guidance. And non-GAAP earnings per share are now expected to be between $6.95 and $7.15 – also lower than $7.28 in fiscal 2021 but much higher than in the previous guidance.

As a result, the stock jumped after earrings were released and in the following weeks the stock gained as much as 27%. And during the last three months, we saw 24 up revisions for revenue in the upcoming quarter (compared to zero down revision) and 25 up revisions for earnings per share (compared to 0 down revisions).

Segment Results

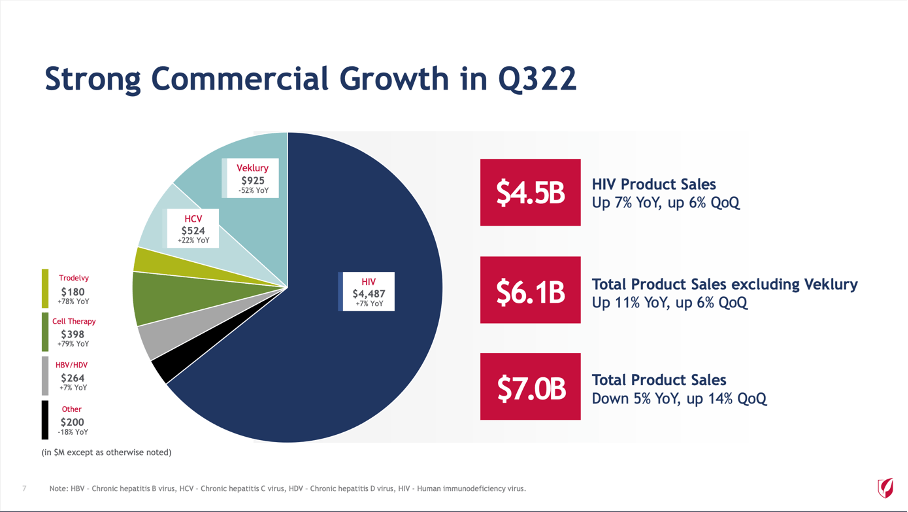

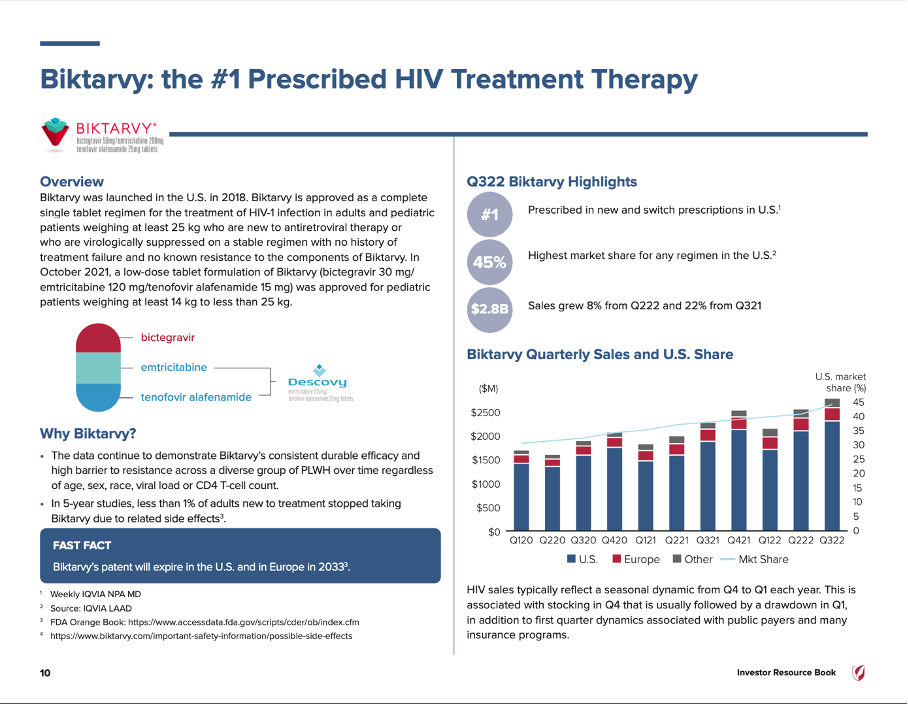

We can also look at the different segments and HIV is contributing the biggest part of revenue. In Q3/22 the segment generated $4,487 million in sales (an increase of 7% YoY) with its biggest growth driver Biktarvy. When excluding Veklury sales, Biktarvy is responsible for 46% of total revenue and it is always problematic when one product is responsible for a huge part of revenue (without doubt, Gilead Sciences knows this from its past). But it is soothing that Biktarvy is patent protected until 2033 (we will get to this).

Gilead Sciences Q3/22 Presentation

HCV sales were $524 million in the third quarter and could increase by 12% year-over-year and when excluding Veklury, Cell Therapy was the third-biggest segment which generated $398 million (79% year-over-year growth). The good news for Gilead Sciences is that basically every segment could grow and only Veklury was responsible for the top line decline.

Growth

I already mentioned in my last article that Gilead Sciences seems to be positioned much better right now than a few years ago. Aside from Veklury, which will most likely see declining sales in the coming quarters, all other blockbuster drugs are patent protected for several years and the risk of declining revenue due to expiring patents is rather low.

And while the risk of declining revenue is limited, Gilead Sciences has several products either in its pipeline or already approved that will contribute to revenue growth in the years to come. In my last article I already mentioned Trodelvy as a potential blockbuster candidate and in Q3/22 the drug generated $180 million in revenue (an increase of 78% compared to $101 million in the same quarter last year). Year-to-date, Trodelvy generated $485 million in sales and although estimates for peak sales have been lowered by some analysts – due to higher competition – Gilead Sciences might still generate $2.5 billion in revenue annually in a few years.

Gilead Sciences Q3/22 Presentation

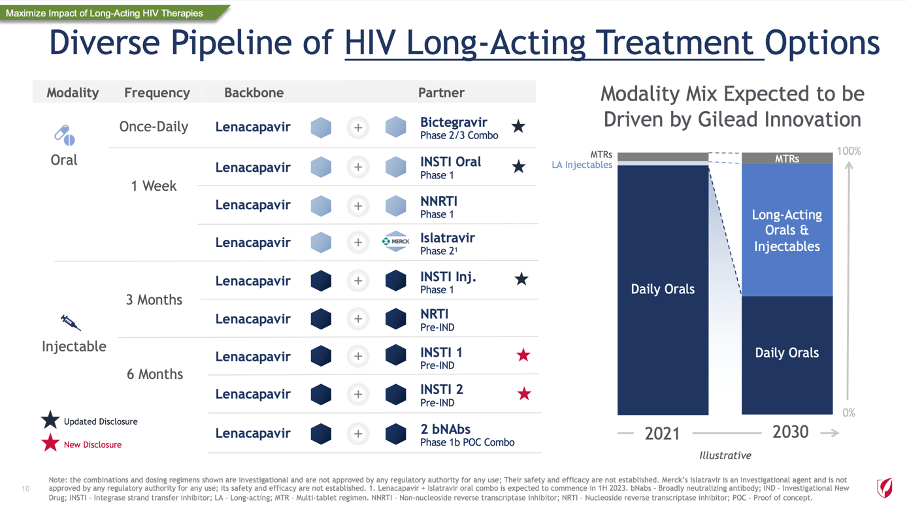

In the second half of 2022, Sunlenca was approved in the European Union as well as in the United States. Sunlenca is the based on lenacapavir as backbone and hopefully only the first product of a diverse pipeline of long-acting HIV-treatments developed by Gilead Sciences. The company’s goal is to move away from oral products that must be taken daily and towards injectable products, which are long-acting (weekly, monthly, or quarterly injections seems possible). At this point, we don’t have any sales data yet, but peak sales are expected to be somewhere in the range of $1.0 billion to $1.5 billion.

Gilead Sciences JPM Presentation

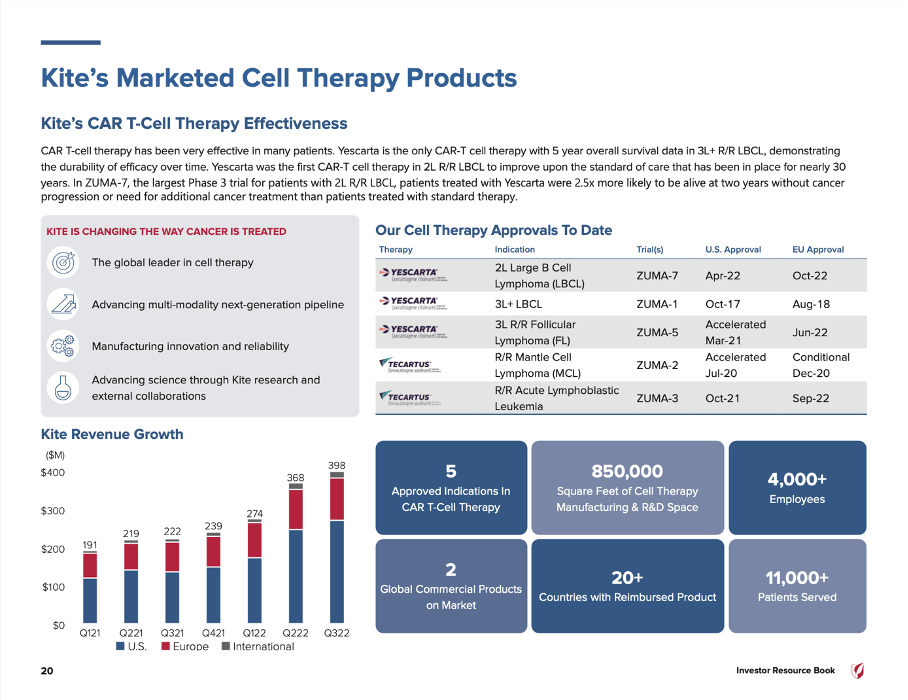

In 2017, Gilead Sciences acquired Kite Pharma for $11.9 billion and while the acquisition was criticized heavily at the beginning it seems to make sense. The revenue from Kite’s products is growing at a solid pace and so far, Yescarta as well as Tecartus are contributing to revenue. In Q3/22 both products generated $398 million in revenue and in the last twelve months the generated revenue was $1,279 million. But peak sales estimates for Yescarta alone are as high as $2.2 billion and expected revenue for Kite’s products could be $3 billion annually in the years to come.

Gilead Sciences Q3/22 Investor Resource Book

And finally, Gilead Sciences’ current blockbuster – Biktarvy – is also worth mentioning as it might contribute to growth. In the third quarter of fiscal 2022, Biktarvy generated $2,766 million in revenue and year-to-date it generated $7,472 million. And although Biktarvy is close to generating $10 billion annually I see further growth potential. First, Biktarvy is patent protected until 2033 in the United States and Europe holding potential competitors at bay for the next ten years. Second, Biktarvy already has a market share of 45% in U.S. treatment TRx share but it could still grow its share by 4pp over the last twelve months and we can assume this growth to continue – but maybe with a slower pace. Third, even if Biktarvy can’t gain additional market shares or new patients, Gilead Sciences can – and most likely will – increase prices, which will lead to higher revenue. Recently, Gilead Sciences increased the price for Biktarvy by 5.9% in the United States.

Gilead Sciences Q3/22 Investor Resource Book

Assuming that Gilead Sciences should be able to increase its revenue 5% annually for the next five years (we will return to this assumption in our intrinsic value calculation), it would generate about $33 billion in revenue in 2027, which means about $7 billion in additional revenue. And when assuming that Trodelvy might contribute about $1.5 - $2.0 billion in additional revenue, Kite’s products contribute also about $1.5 - $2.0 billion, Sunlenca will contribute about $1.5 billion and for Biktarvy it is not unlikely to contribute additional $2.0 - $3.0 billion in sales, this might almost be enough to compensate declining Veklury sales and grow the top line by 5% annually.

Still Three Reasons To Buy?

In my last article about Gilead Sciences, I offered three reasons to buy – the valuation, the dividend, and the upcoming recession. Let’s take a closer look if these reasons still exist and we start with the possibility of a recession.

Recession

In my last article I argued that Gilead Sciences is a good buy as healthcare companies are usually performing well during a recession. The demand for the products is stable – no matter what happens. And although investors might have gotten more optimistic again about a soft landing or the economy even being able to avoid a recession, I still see the risk for a recession rather high. Many early warning indicators are hinting towards a recession and we can still expect a solid performance for Gilead Sciences during a recession (compared to many other assets, which should not be bought before or during the early stages of a recession).

Dividend

A second strong argument for Gilead Sciences as an investment was the high dividend yield of almost 5%. Right now, Gilead Sciences has a dividend yield of 3.4%, which is still solid but not as high as it has been before. And considering that the U.S. 10-year treasury yield is slightly higher, we should not buy Gilead Sciences just for the dividend.

Nevertheless, we can expect Gilead Sciences to increase the dividend again when the company will report Q4/22 results in about two weeks from now. And I expect a raise at least to $0.75 and as management is getting more optimistic about its business, a quarterly dividend between $0.75 and $0.80 also seems to be in the cards. And as the dividend is well covered, a raise should not be a problem. In the last four quarters, Gilead Sciences paid $3,688 million in dividends and generated $9,007 million in free cash flow – resulting in a payout ratio of 41%, which is no reason to worry. Of course, we can point out that earnings per share for fiscal 2022 will be around $3.45 and Gilead Sciences paid $2.92 in dividends resulting in a payout ratio of 85%. However, I would rather focus on free cash flow instead of earnings per share.

Valuation

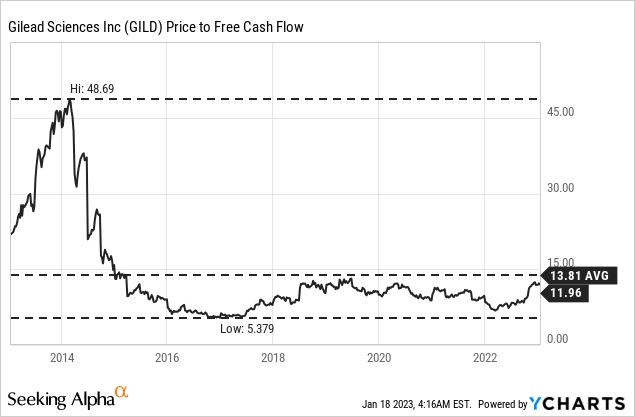

A third and final reason to buy Gilead Sciences was the extremely low valuation the stock was trading for. And similar to the dividend yield, which went down, the valuation multiples went up in the last few months. And when looking at the price-free-cash-flow ratio, Gilead Sciences is actually trading for one of the highest valuation multiples in the last five years. Nevertheless, Gilead Sciences is trading only for 12 times free cash flow and such a valuation multiple seems more than reasonable for the business.

When using a discount cash flow calculation to determine an intrinsic value, we can take the free cash flow of the last four quarters as basis ($9,007 million). And when assuming 10% discount rate as well as 1,261 million in outstanding shares, Gilead Sciences must grow slightly below 2% annually from now till perpetuity to be fairly valued.

And while I don’t think we have to argue if Gilead Sciences is able to grow between 1% and 2% annually in the years to come, we can ask the question if higher growth rates are possible. We can start by looking at the growth rates in the last ten years and while earnings per share increased with a CAGR slightly below 11%, free cash flow increased even with a CAGR slightly above 12%. One could argue that Gilead Sciences was profiting from Harvoni and Sovaldi, but when looking at the last 10 years we can see that Gilead Sciences profited from those two in the years between 2014 and 2018, but it does not really have an effect on the 10-year growth rate anymore.

In my opinion, Gilead Sciences should be able to grow at least in the mid-single digits in the years to come. A growth rate in the mid-single digits can already be achieved by share buybacks. In the last ten years, Gilead Sciences decreased the number of outstanding shares with a CAGR of 3% and when subtracting the payments necessary for the dividend from the current free cash flow, Gilead Sciences is generating enough FCF to repurchase about 5% of outstanding shares. And when assuming a growth rate of 5% till perpetuity, we get an intrinsic value of $142.85 for the stock.

Conclusion

I understand that analysts are not willing to assume higher growth rates for Gilead Sciences when considering the last few years. And I am also not willing to bet on Gilead Sciences trading for $140 anytime soon, but the stock still seems to be undervalued and I remain bullish about Gilead Sciences. To answer the question where Gilead Sciences might be going – in my opinion, chances are high for the stock to continue its bullish upward trend.