- Tech stocks are on the back foot in premarket trading, with the Nasdaq 100 futures (NDX.IND) (NASDAQ:QQQ) down 0.1% after a strong gain yesterday.

- It's been a positive but underperforming year so far for the homes of the biggest tech stocks, with Info Tech (NYSEARCA:XLK), Communications Services (NYSEARCA:XLC) and Consumer Discretionary (NYSEARCA:XLY) up 9% to 12% year to date, beating the classic defensive sectors, but trailing cyclicals.

- And Societe Generale's Global Strategist (and noted bear) Albert Edwards says megacaps could be a trigger for the correction that many on Wall Street are expecting.

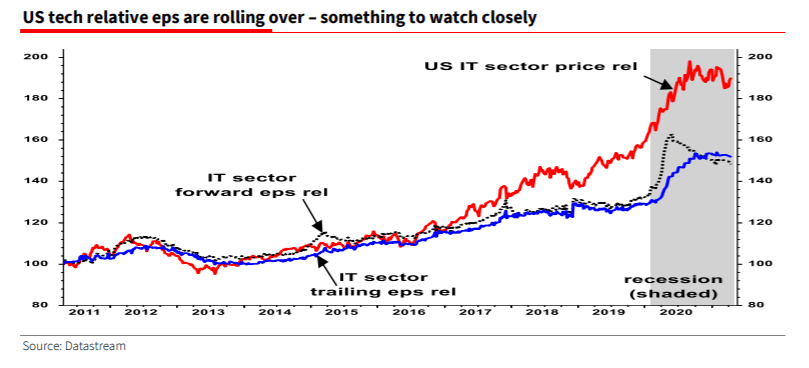

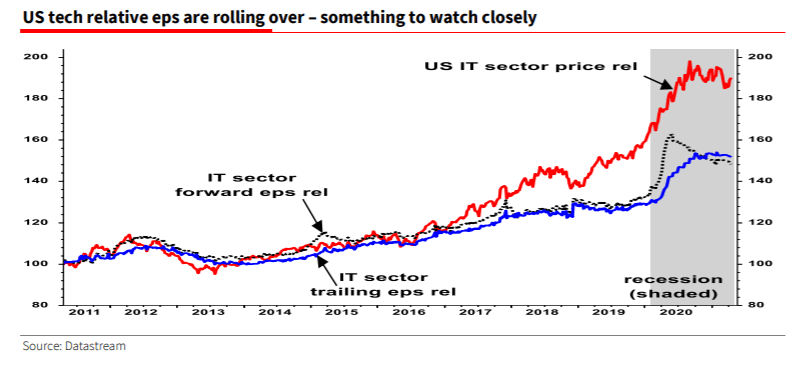

- He points to the "vulnerability" in the FAANG stocks - Facebook (NASDAQ:FB), Amazon (NASDAQ:AMZN), Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL), Apple (NASDAQ:AAPL) and Netflix (NASDAQ:NFLX) originally but now including Microsoft (NASDAQ:MSFT) and Tesla (NASDAQ:TSLA) - and IT stocks in general as earnings roll over.

- "The extreme multiple expansion in excess of the overall market only emerged in the wake of the Dec 2018 Powell Pivot," Edwards writes in a note today.

- "Clearly rising bond yields are a huge threat to the tech sector," he adds.

- The 10-year yields has been fairly quiet this week. This morning it's up 1 basis point to 1.58%, well off this year's highs near 1.75% (NYSEARCA:TBT) (NASDAQ:TLT).

- "But I still think a bigger threat might yet be sliding tech earnings relative to the market, perhaps in the event of a lull in growth as a fiscal cliff edge is reached – maybe later this year."

- "But like everything else, I’m sure it’s nothing to worry about."

- Edwards outlined his reasons earlier this month for how a big economic pothole could develop in H2 2021, saying "the expected pop-up in YoY US core inflation will be back in sharp reverse, leaving the inflation breakevens totally detached from the Q3 inflation rate and GDP growth reality."

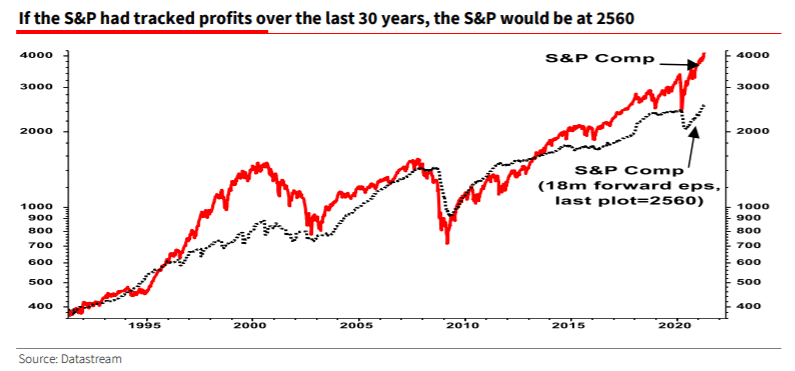

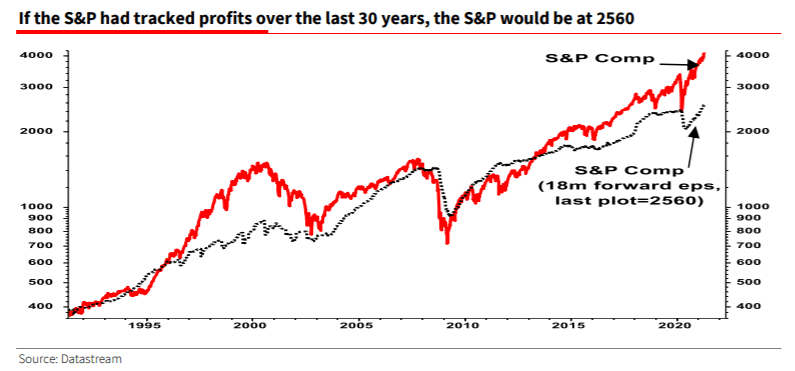

- Today he also notes that while people may say valuations don't matter, in the long run "profits do (sort of)."

- "Taking analysts’ typically overoptimistic 18-month forward earnings and rebasing them to the same level of the S&P 30 years ago, we can see that a huge gap has opened up," he said.