Company Overview:

Empire State Realty Trust, Inc. (NYSE:ESRT) is a real estate investment trust that owns, manages, operates and acquires the office and retail properties. The company is offering 71,500,000 shares of its Class A common stock in the price range of $13.00 and $15.00 per share. The expected listing date is October 02, 2013 on New York Stock Exchange (Source: IPO prospectus)

Business Overview:

The company operates its business in Manhattan and the greater New York metropolitan area and as of June 30, 2013, it owns 12* office properties, including the Empire State Building.

* One property on long-term ground leasehold interest.

Present revenue generating assets:

- Manhattan assets:

It owns seven office properties in Manhattan with about 5.9 million Sq. feet of rentable office space and about 400615 Sq. feet of rentable premier retail space on the ground floors. Its most precious asset, the Empire State Building, is also located in Manhattan (see the picture below, the tallest is the Empire State building). The company also owns four standalone retail properties aggregating about 183019 Sq. feet of retail space.

- Other assets: (greater New York metropolitan area)

The company also owns five properties, aggregating about 1.8 million of rentable square feet, in Fairfield County, Connecticut and Westchester County, New York. The company also owns two standalone retail properties aggregating about 21433 Sq. feet of retail space.

In total the company owns about 7.7 million Sq. feet of office space and 645067 Sq. feet of retail space. About 83.5% of its office space and 80.5% of its retail space has already been leased.

- Entitled land:

The company also owns some entitled land in Connecticut, which it intends to develop at the appropriate time. The land is expected to support the development of an approximately 380,000 rentable square foot office building and garage, which the company refers to as Metro Tower. This development, whenever materialized, will lead to about a 5% addition to its existing office space.

- Option properties:

"In addition, we have an option to acquire from affiliates of our predecessor two additional Manhattan office properties encompassing approximately 1.5 million rentable square feet of office space and 153,209 rentable square feet of retail space at the base of the buildings. These option properties were subject to recently resolved litigation and we have an option to acquire fee, long-term leasehold, sub-leasehold and/or sub-subleasehold interests in these two properties, as applicable, following the resolution of the recently resolved litigation." (Source: IPO prospectus)

If the company utilized its option to acquire these properties, then these properties will lead to an addition of about 19.5% increase in existing office space and about 23.75% increase in existing retail space.

Intended Distribution:

The company intends to make regular quarterly distributions of $0.085 per share for a full quarter. On an annualized basis, this would be $0.34 per share implies 2.4% yield based on the mid-point of the IPO range.

Corporate Structure:

After the completion of this offering, the company will control and operate the assets. The equity owners will have about 37.8% economic interests in the assets (see the chart below).

Financials:

($ in thousands) | Pro Forma | |

H1 FY 2013 | FY 2012* | |

Total Revenues | 250,709 | 511,266 |

Revenues from ESB | 114,000 (45.5%) | 240,800 (47.1%) |

Income from Operations | 56,895 | 131,822 |

Interest expense, net | 27,659 | 54,156 |

Net Income | 29,236 | 77,666 |

Income attributable to non-controlling interests | (18,185) | (48,308) |

Income attributable to equity owners | 11,051 | 29,358 |

Pro Forma basic earnings per share | $0.12 | $0.32 |

*"During 2012, the Empire State Building also received a real estate tax refund in the amount of $10.1 million, which was 4.5% of its 2012 revenues." (Source: IPO prospectus) | ||

Balance sheet ($ in thousands): | ||

Pro Forma Condensed Consolidated Balance Sheet, June 30, 2013 | ||

Assets | $2,472,322 (includes commercial real estate properties of $1,227,321 and goodwill of $637,639) | |

Liabilities | $1,408,187 (includes mortgage notes payable of $893,269 and term loan and credit facility of $270,500) | |

Total Equity | $1,064,135 | |

Key points:

Key concerns:

1. High dependence on the Empire State Building:

The company to a large extent depends on the Empire State Building for its revenues, which not only generates revenues from its rentable space but also from the observatory operations and broadcasting licenses. The Empire State Building accounts for 47.1% and 45.5% of its revenues in FY 2012 and for the six months ended June 30, 2013, respectively.

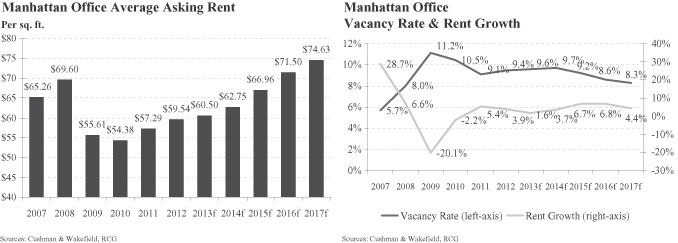

2. Rent trends depend upon economic conditions:

Historically, rent/lease rates tend to move with the economic conditions. Any steep slowdown in economy normally results in steep decline in asking rent and lease rates. The chart below clearly shows how the rent/lease rate in the Manhattan area fell during the 2008-2010 economic slowdown, due to high vacancy rate.

Though the company's lease contracts are of long-term, it does renew some contracts almost each year, so during the slowdown the company can have to cut down its asking rates.

3. Dependence on observatory and broadcasting licenses:

The company generates about 18.0% of its revenues in FY 2012 and 17.6% for the six months ended June 30, 2013 from observatory operations and more importantly the company earns about 54.20% and 58.83% of its operating income from said operations during same periods respectively. The observatory operations are not normal real estate operations and mostly depend upon tourist trends and availability of alternative tourist attractions. Observatory business is subject to some seasonality as the number of visitors, on average, has been slightly higher in the third quarter and slightly lower in the first quarter of each year. The company also earns approximately $17.1 million and $10.1 million of revenue, respectively, from its broadcasting licenses related revenue.

4. Tax concerns:

Dividends payable by REITs do not qualify for the reduced tax rates on dividend income from regular corporations.

As mentioned in the IPO prospectus:

"The maximum U.S. federal income tax rate for certain qualified dividends payable to U.S. stockholders that are individuals, trusts and estates is 20%. Dividends payable by REITs, however, are generally not eligible for the reduced rates and therefore may be subject to a 39.6% maximum U.S. federal income tax rate on ordinary income when paid to such stockholders."

Key positives:

1. Operate and control Empire State Building:

The company operates and controls one of the world's most renowned real-estate assets, the Empire State Building. This gives the company unmatched brand recognition.

2. Available Space at Manhattan Office Properties:

Despite being located at prime locations, as of June 30, 2013, its Manhattan office properties vacancy rate was over 15% as compare to the overall vacancy rate of about 9% (see the chart below). The company had approximately 1.1 million rentable square feet of available space, which has the significant potential to generate additional revenues in the future.

3. Diversified and high quality tenants:

As of June 30, 2013, its property portfolio was leased to a diverse base of approximately 1,066 tenants. Its tenants represent a broad array of industries and government entities, including: LF USA, Federal Deposit Insurance Corporation, Warnaco, LinkedIn (LNKD), Bank of America (BAC), JPMorgan (JPM).

4. The future growth potentials:

The company holds the significant growth possibilities as the development of entitled land (whenever done) and acquisition of option properties (if exercised) can significantly increase the rentable assets of the company. Moreover, the revenue from the observatory is expected to show a steady rise every year under normal economic conditions.

Valuations:

At $14 (mid-range of offer price) the company is available at PE of above 50 (annualized H1 FY 13).

Conclusion:

The company is a REIT and holds some prime properties, including the Empire State Building. The company got a stable revenue stream from rents, observatory and broadcasting operations.

The company is managed by an active, experienced and committed team that focuses on improvement of asset quality through renovations, modernization and by installing energy-efficiency retrofits, as a result of these installations, the Empire State Building is now an Energy Star building and has been awarded LEED EBOM-Gold certification. These things not only improve the tenant experience and engagement but also result in the cost saving for the company as well as for the tenants, as mentioned by the company:

"As a result of the energy efficiency retrofits, we currently estimate that the Empire State Building will save at least 38% of its energy use, resulting in at least $4.4 million of annual energy cost savings. Johnson Controls Inc. has guaranteed minimum energy cost savings of $2.2 million annually, from 2010 through 2025, with respect to certain of the energy efficiency retrofits which Johnson Controls Inc. was responsible for installing." (Source: IPO prospectus)

The company holds significant potential to increase its business assets and revenues through land development, re-leasing of expired leases (about 9.3% of its Manhattan office leases are expected to expire through December 31, 2014), lease-up of available space as well as through the acquisition of option properties. However, a lot will depend on the valuations at which the company gets these option properties, and leasing rates (the company hopes to get better rates, but the actual rates will depend on the economic conditions).

In any industry, the quality of customers tells the quality of product/services, in real estate business quality of tenants tells the quality of assets and services. The company is not only improving tenant experience, but it's also focusing on the quality of tenants and is looking forward to deal with fewer but larger and higher credit-quality tenants like LF USA, Federal Deposit Insurance Corporation, Warnaco, LinkedIn, Bank of America, JPMorgan. These world-class tenants tell a lot about its asset quality and related services.

Unlike many other REITs that earn most of its revenues from rent/lease related operations, the company also earns some of its revenues and significant part of its profit from businesses that traditionally don't belong to the real estate business like: observatory and broadcasting licenses (explained above). Fundamentally, the company looks very good with excellent assets and tenant quality. However, for the time being, at offer price it seems to be fully priced, but the presence of the Empire Estate Building can create some enthusiasm.

Data source: IPO prospectus.

Disclaimer:

Investments in stock markets carry significant risk, stock prices can rise or fall without any understandable or fundamental reasons. Enter only if one has the appetite to take risk and heart to withstand the volatile nature of the stock markets.

This article reflects the personal views of the author about the company and one must read offer prospectus and consult its financial adviser before making any decision.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.