After an illiquid final week in 2010, the U.S. stock market will embrace a data-heavy week in the beginning of 2011. The most significant ones are the December PMI and the December nonfarm payrolls.

On Monday, the December U.S. PMI will be released. As one of the most important leading indicators on manufacturing activities, the U.S. PMI in the first half of 2010 had been very strong. However, in the second half of 2010, PMI dropped to 54.4 in September. With the new order index at 51.1, that's slightly above the 50 level that edges closer to the territory of economic declinr. With the support of QE2, the October and November PMI showed strong growth again.

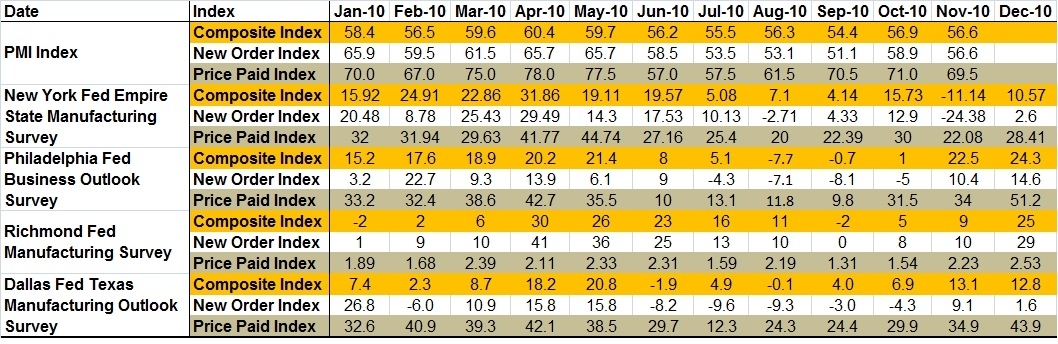

As the first important economic indicator to be released in 2011, the December PMI could set the tone of markets as investors come back from long vacations. For those who want to make an educated guess on this number, some recent economic data already gave out some hints. Table 1 lists economic indicators from Fed that lead PMI and measure manufacturing activities in the US.

Table 1: Regional Fed Manufacturing Surveys and the U.S. PMI (Click to enlarge)

Three out of four regional Fed economic composite indices show manufacturing activities accelerating in December in those regions. The Dallas survey is the only exception, showing a slight drop. Also, three out of four surveys show that in the New York Fed district, the Philadelphia Fed district, and the Richmond Fed district more manufacturers received new orders in December than in November. The increase in the new order is a good sign for manufacturing employment in regions covered by the four Fed districts. Of course, these are not guarantees that the national December PMI will be higher than in November. But significant gains in December's regional survey results definitely increase the chances of a higher December PMI and raise market expectations accordingly.

Indices of prices paid by manufacturers in all four Fed districts are up from November. In the Philadelphia Fed district and the Dallas Fed district, the increase in manufacturing input costs are quite significant. This probably represents a macro trend of increasing production costs. As I argued before, I suspect that manufacturers will have to bear a large portion of the increased costs themselves.

The last notice is that of the December HSBC China PMI, which is just out: 54.4, a three-month low as output and new orders both eased. Though the HSBC China PMI is not as influential as the official China PMI (which will be released on January 1, 2011 for December), it usually moves with the official PMI.

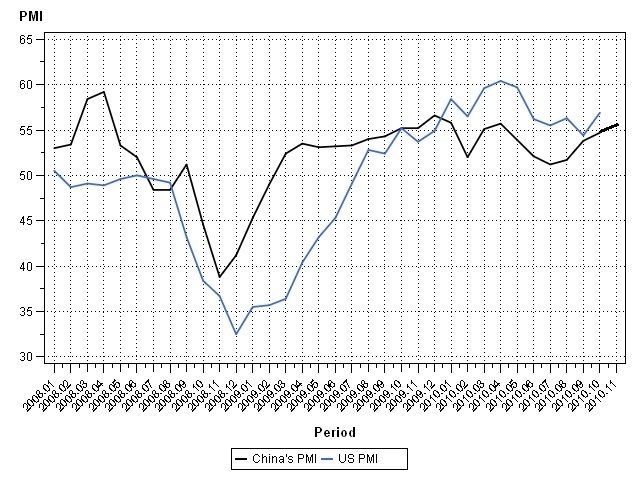

The HSBC China PMI shows that new orders in December mostly came from the Chinese domestic market, which could imply that there is potential weakness in the U.S. final demand part of the supply chain, as the China PMI often leads the U.S. manufacturing activities by a few months. This is seen in Chart 1 (reproduced from previous post).

Chart 1: The China Official PMI and the U.S. PMI

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.