Is E. I. du Pont de Nemours and Company (DuPont) (NYSE:DD) finally a buy?

That's the question on institutional and retail investor minds alike. Is now the time to buy DuPont and hold it forever? It's a good question. I think the answer is still a NO and I think that investors will do well to reconsider the stock after Q2 earnings when management will likely face tough questions and likely have no answers. If I'm right, shares will be punished and investors will have an even "better" opportunity to get long.

Although I've been impressed with management since giving a spirited and unusually clear presentation at a recent conference, management finally coming around to meet the minimums can't change the facts. The facts are that DuPont has clear and long running EPS growth issues (even taking into account questionable accounting of EPS pointed out in a former Trian Fund whitepaper) and no apparent solution on the horizon. Worse, as DuPont-historian and expert analyst "funfun" points out regularly in correspondence to articles - DuPont appears to think that "shrinkage equals growth" is the solution.

Very rarely has this strategy ever been successful, regardless of sector. That said, growth or lack thereof most certainly is the underlined theme at "Current Generation" DuPont - a play on CEO Ellen Kulllman's recent promises of a "Next Generation" DuPont. Next Generation DuPont we've been promised will be a DuPont that is fast growing, focused, innovative, and a defensible leader. While not providing anything specific in making these promises Kullman did promise a more efficient DuPont and one that will undergo extreme cost cuts on its way to becoming optimized. Granularity and accountability has been promised at Q2 reporting. I for one consider this the most anticipated earnings period in the last ten years and will be scrutinizing it under the most powerful of microscopes.

In waiting for this granularity, however, it's up to our crowd sourced research to determine if DuPont has fallen far enough from its bloated, valuation multiple expansion driven market cap highs to be considered a value. This DuPont followers' analysis concludes that it has not based on comparable company analysis both current and forward looking.

1Peer group is comprised of:

- Dow Chemical Co. (DOW) - NYSE

- Monsanto Company (MON) - NYSE

- Eastman Chemical Co. (EMN) - NYSE

- Axalta Coating Systems (AXTA) - NYSE

- Huntsman Corporation (HUN) - NYSE

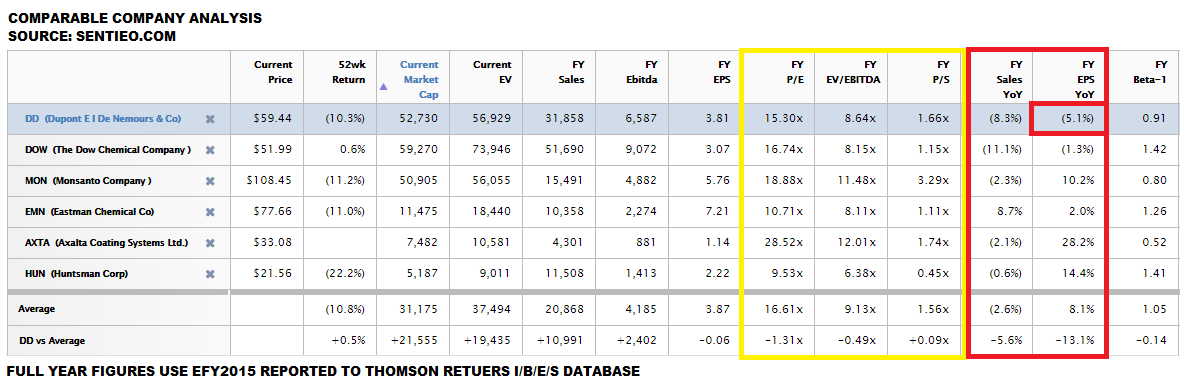

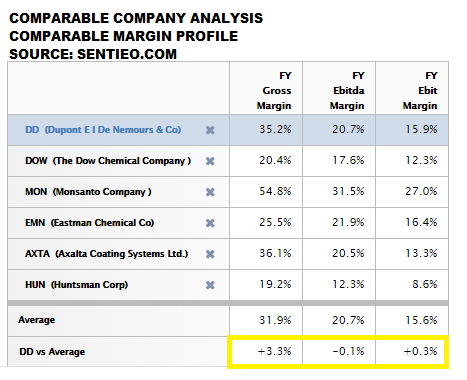

A current comparable company analysis shows that DuPont is only just now being valued in-line with peers1 and that based on EFY15 sales and EPS Y/Y growth it shouldn't even be valued in-line. To be clearer, DuPont has noticeably lower Y/Y expected sales and EPS growth rates, its EPS growth is expected to be 13% slower than the peer group average. It should also be noted that DuPont doesn't have a superior margin profile or any other obvious characteristic that would warrant such a marked and long-standing premium to peers valuation.

Yet for some reason, largely analyst driven I'm sure, investors are still valuing DuPont in-line with the healthier peer group. I believe this was the point that Nelson Peltz and Trian Fund were trying to make clear to investors. That for some unexplained reason (again largely analyst driven) DuPont has been able to mask its fundamental failures of years past. Had DuPont been valued at a true in-line to its comparable fundamental health all along I have no doubt that Peltz would have been successful in his coup attempts. Investors would have been fatigued and surely impatient with management, ultimately allowing a change to be facilitated.

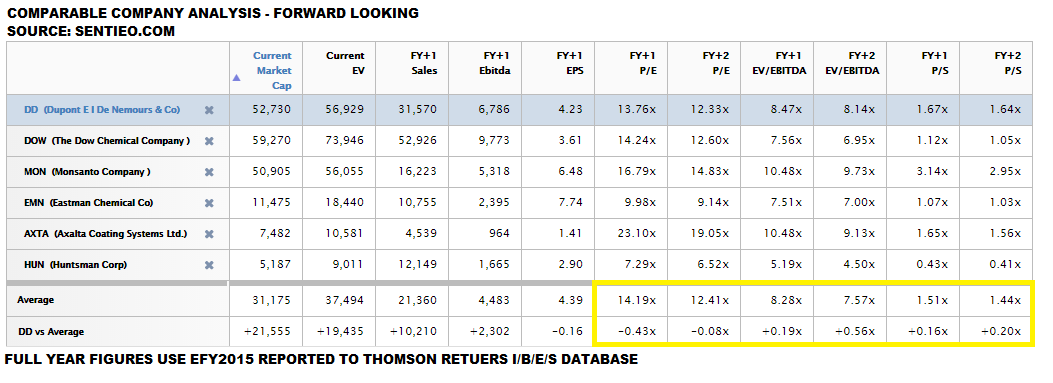

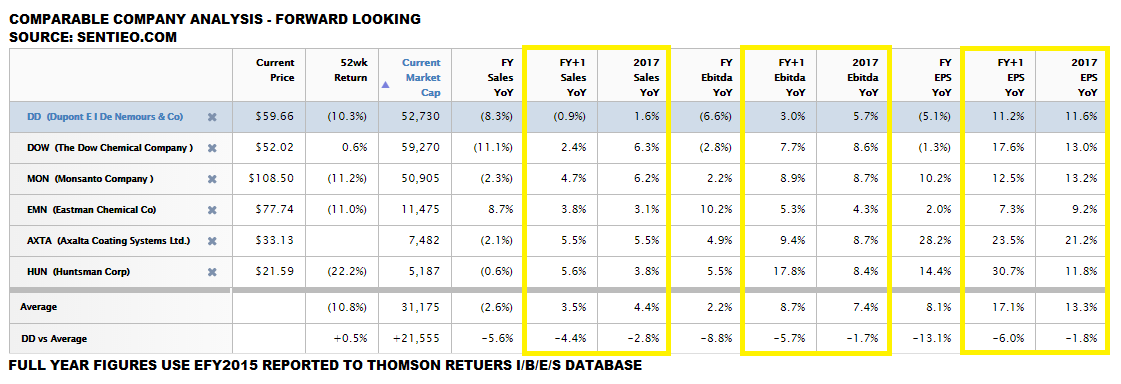

When looking at DuPont on a comparable forward looking basis the status quo holds over:

Again DuPont is expected to achieve comparable valuation multiples on sub-peer group growth. While the growth gap is expected to close one is still expected to exist at full year 2017 end. This, by the way, is absent the expectation for massive cost cuts and whatever else DuPont management has cooked up as a "fix". Again, I have to ask myself considering a DuPont long position is this really a position that I want to take? Is this really a position that should be put on at anything of comparable multiples to peers? I don't think it is.

So, how has DuPont been able to achieve such an enviable record of premium valuation multiple to peers and how has it remained the only Teflon name in the space? I believe analysts. I believe the raging bull analyst community has been responsible for floating DuPont on the back of Ellen Kullman's "just enough" information management. But, at least according to Kullman, that "just enough" information (along with the aforementioned questionable accounting) is set to change. Will this mean the end of the analyst catalyst? I believe even the possibility is reason enough to avoid shares for now.

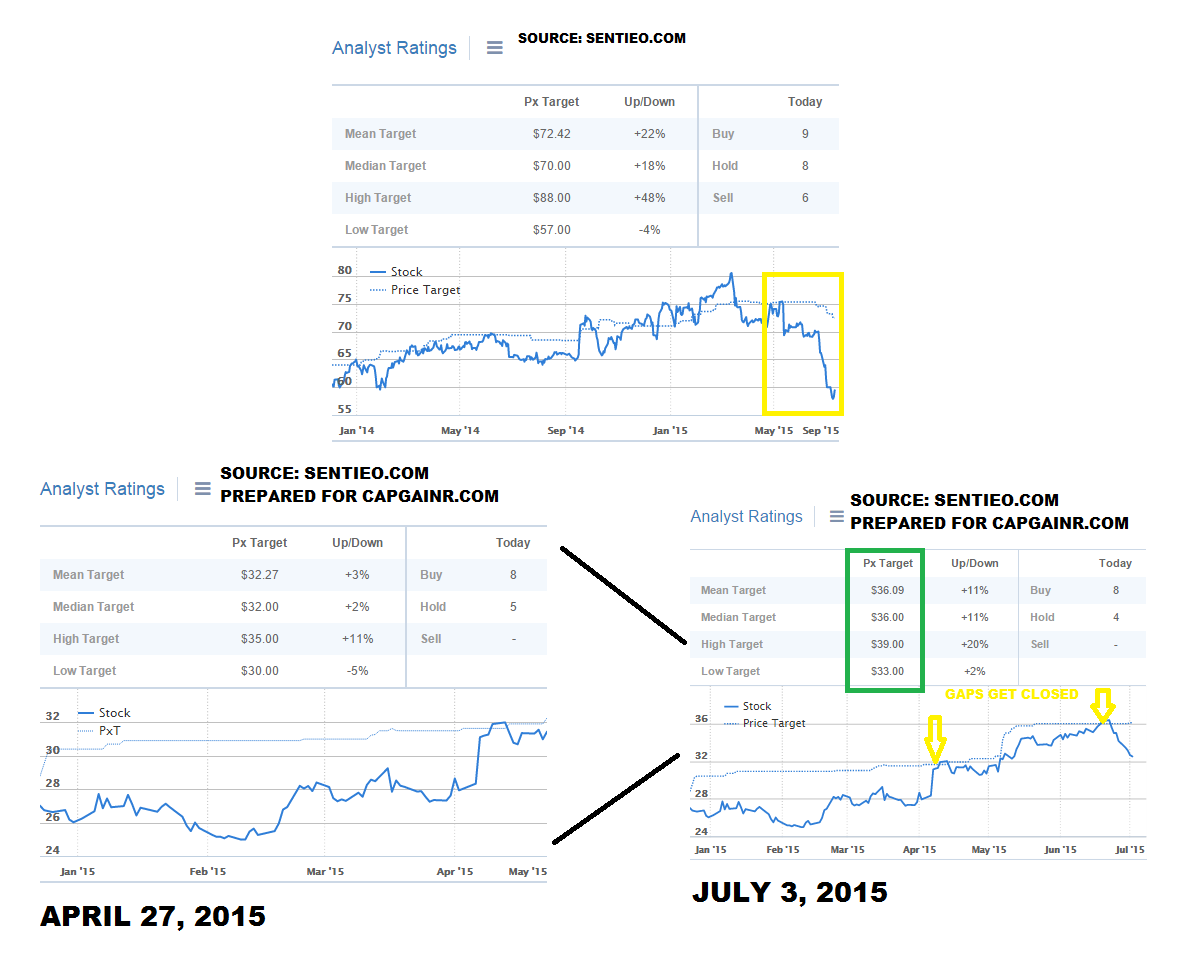

In the graphic above you can see a clear share price magnet created by analyst price targets. The DuPont share price always seems to pull towards and meet the consensus price targets despite a clear fundamental lacking when compared to peers. This magnet pull has also taken place in the face of continued secrecy, lack of accountability, and a failure to innovate. Time and time again the analyst community has been there for DuPont with raging price targets. Complicit in what has long been DuPont's game of Ellen Kullman's Three Card Monte. Kullman and the community have been the hustlers, we've long been the mark.

But again now the second player this Street Hustle is being forced to leave the game as Kullman and DuPont are being forced into full disclosure. This should mean, if the analysts covering DuPont have any intention of saving face, honest price targets. That should further mean negative price target revisions from what are currently 22% to 48% expectations of upside. If the DuPont Q2 reporting/guidance/and plan are anything but virtuoso expect the one dependable analyst catalyst to be removed.

I recommend investors wait on DuPont until post Q2 reporting. While DuPont has become "cheaper" over the last month or so the fundamentals and comparables say it can still get cheaper.

Good luck everybody.