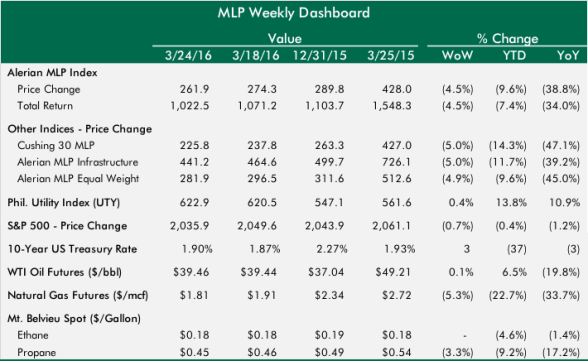

In a short week, MLPs gave up last week's gains with a 4.5% decline overall. The active oil contract shows up as flat week over week, but given the May contract that took over on Tuesday was actually down 4%, and dipped below $40/bbl after closing above $40 on Tuesday for the first time in 2016. MLPs have produced 28.9% off the lows even after this week, and remain on pace for the first positive month since October 2015.

After no equity issuance since November, we got 2 MLP offerings this week. The Shell Midstream Partners (SHLX) deal was upsized and traded well, which was encouraging. We still haven't seen a more distressed MLP issue equity in a public deal since September 2015. Also, a week can't go by without more drama from Energy Transfer Equity (ETE) and Williams Companies, Inc. (WMB), and it looks like the suspense will continue through May (see below for details).

The U.S. dollar reversed some recent weakness to push oil lower. The weekly inventory report was mixed, with a draw at Cushing, strong product demand signals, and lower oil production offset by a large import number that resulted in a big week-over-week inventory build, fairly isolated to the Gulf Coast. Oil's decline reversed a bit on Friday following the rig count numbers that showed a 15 rig decline overall.

Easter Break Down

There aren't many non-animated movies centered around Easter. But two movies do seem somewhat relevant if you think about the MLP sector as the Easter Bunny. The first is Mallrats, the low budget Kevin Smith film from 1995. In that movie, Jay and Silent Bob (dressed in all black, personifying oil) attack the mall's costumed bunny in front of a horrified group of children.

The other bunny-related movie scene that comes to mind is from A Christmas Story, when Ralphie gets a pink bunny suit from his Aunt Clara and is forced to model it for the family. He obliges, but with a miserable look on his face that probably resembles some frustrated MLP investors this week.

While children delight this weekend as they skip around backyards across the country hunting for dyed eggs, investors continue their hunt for sustainable oil price traction that will eventually lead to stability in the MLP sector. Also, like some recent M&A in the midstream sector, finding the most eggs wins you little more than pride and a basket full of inedible eggs that get thrown away. Happy Easter and NCAA basketball to all.

Winners & Losers

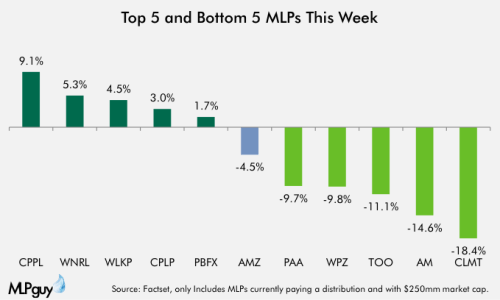

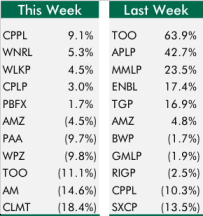

New this week, the charts in this section will focus on relevant MLPs, or those with a market cap above $250mm. Columbia Pipeline Partners (CPPL) led all MLPs after trailing most MLPs last week on the TransCanada acquisition announcement. Small cap refiner-sponsored MLPs Western Refining Logistics (WNRL) and PBF Logistics (PBFX) made the top 5. On the downside, Plains All American Pipeline (PAA) continues to trade in tandem with oil prices. The updated S-4 from Energy Transfer hurt Williams Partner's (WPZ) stock price. Antero Midstream Partners (AM) dropped on the secondary sale from its sponsor on Friday. Teekay Offshore Partners (TOO) gave up some of its massive gains from last week.

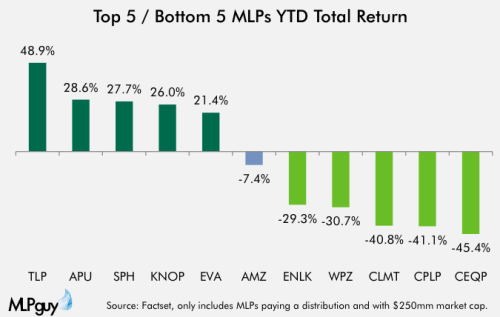

Crestwood Equity Partners (CEQP) traded up slightly this week, but remains at the bottom of the sector. WPZ and EnLink Midstream Partners (ENLK) are the biggest MLPs in the bottom 5. Each of the top 5 year-to-date declined this week, with the exception of AmeriGas Partners (APU), which was slightly better than flat.

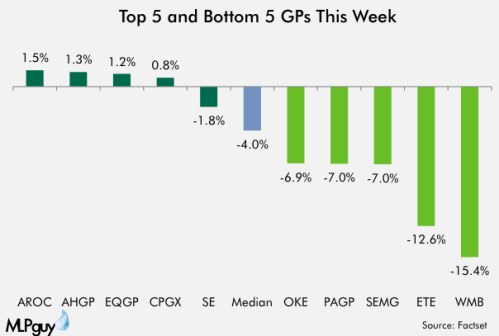

General Partner Holding Companies

General partners outperformed MLPs on average again this week, but no single GP managed to gain 2% this week. ETE and WMB volatility continued, taking the bottom 2 spots after taking the top 2 spots last week.

News of the (MLP) World

Equity offerings and fresh ETE/WMB drama were the focus this week. Expect at least one equity deal this week now that the ice is broken, but it will probably be more of the same low-risk bought deals from premium MLPs.

Financing

- Shell Midstream priced public offering of 11.0mm units at $31.75/unit, raising $349.3mm in gross proceeds (press release)

- Offering was upsized from 8.5mm units originally offered

- Bought deal, re-offered at 6.7% discount to prior closing price, traded up 4.9% from pricing in the next session

- Antero Midstream priced public offering of 8.0mm units at $22.40/unit, raising $179.2mm in gross proceeds for the selling unitholder, Antero Resources (press release)

- 100% secondary offering, no new units issued

- Bought deal, re-offered at 10.2% discount to prior closing price, traded down 2.9% from pricing in the next session

M&A

- Energy Transfer Corp (ETC) filed revised S-4 with updated information, including dramatically lower commercial synergy estimates, discussion of reduced corporate footprint in Tulsa, and unit awards that could increase dilution experienced by WMB shareholders (filing)

- Commercial synergies estimate reduced from $2bn annually by 2020 to $170mm annually in a base case commodity scenario and $590mm in a recovery oil price scenario

- New disclosure on unit awards under long-term incentive plan would reduce WMB shareholder ownership of ETC to 74% from 81%

- Merger will not close prior to May 31st

- ETE and WMB corporate headquarters will be consolidated in Dallas, "as a result, the current presence in WMB in Tulsa, OK and Oklahoma City, OK will need to be significantly reduced"

- ETE management remains consistent in their efforts to make ETE paper look at unattractive as possible to encourage a "no" vote from WMB shareholders, which is one of the only ways ETE can get out of the deal

Other

- Oil production declines will not be replaced for the next several years (Bloomberg)

- Natural production declines haven't materialized due to increased shale productivity and the start-up of large scale projects developed when oil prices were much higher

- Combined oil & natural gas rig count dropped by 15 this week to new all-time low (Houston Chronicle)

- Shale producers add hedges at higher pace lately, locking in breakeven-ish prices (Reuters)