Bambu Productions/DigitalVision via Getty Images

Mowi ASA (OTCPK:MHGVY) is the world's largest producer of farmed salmon.

I started coverage of Mowi in December 2023, with a Hold rating. My thesis was that Mowi had outstanding operations and global leadership in the industry. However, I also considered that the company faces technical/biological limits to production growth and that extraordinary rents would attract capital-intensive competitors to the market. The multiples of current earnings implied too much growth, making the stock not an opportunity.

In this article, I review the company's 4Q23 and FY23 results and call. FY23 was a fantastic year for this operationally excellent company. It was also the first year in which Norway taxes have been applied in full force. The company also discussed strategic and political issues affecting its long-term profitability. Revisiting the valuation, I don't see substantial changes to the thesis or the stock price since December, so I maintain my Hold rating.

Another year of operational excellence

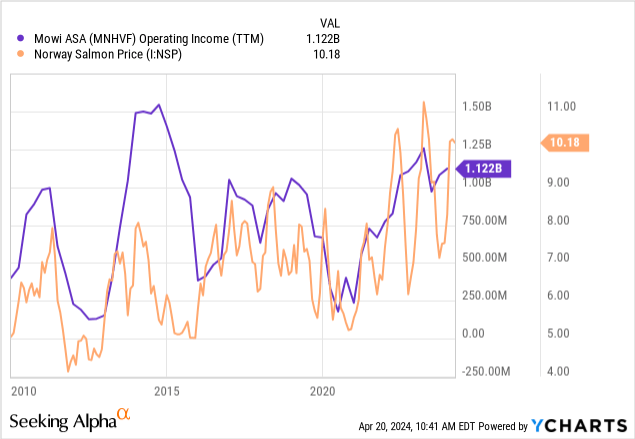

Record year: Mowi broke records in production (500 thousand tonnes for the year), revenues (EUR 5.5 billion), and adjusted EBIT (EUR 1.2 billion).

Generally favorable prices: Since the pandemic, salmon has been on a positive cycle that continued into FY23 despite fears of an economic recession. Global production fell 2%, which helped maintain global price momentum. The chart below reminds us of the strong correlation between salmon prices and Mowi's operational profitability.

Shared across segments: More than 70% of Mowi's operating profit comes from Norway. However, all of the company's segments showed improvements, except for Chile and Canada, two countries where salmon production is heavily affected by biological constraints and that operate at lower margin levels.

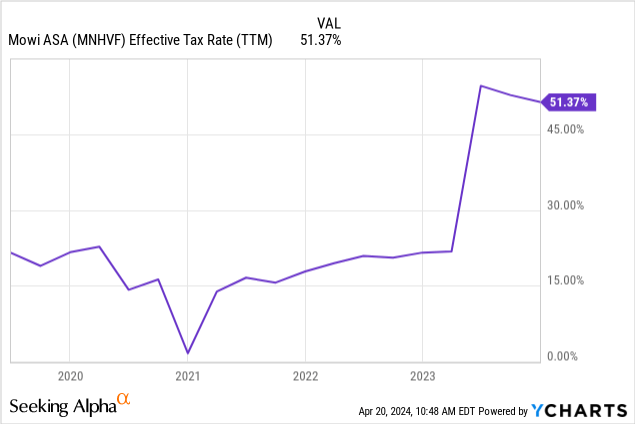

First year of Norway taxes: As commented on my coverage initiation article, the Norwegian government established a 25% income tax on top of the country's 22% tax on salmon farming activities at sea (the resource rent tax). This is because the Norwegian government considers that the activity generates special rents from the natural limitations of the salmon farming space (too much farming leads to algae, lice, or other biological problems).

Mowi expected the tax to increase its effective tax rate by 10% at the corporate level. Unfortunately, this was not the case in FY23, with the effective tax rate jumping almost 30 percentage points. The reason was the recognition of deferred tax liabilities from implementing the resource rent tax. When ignoring these one-time effects, the rate increased to about 27/30% from 20/22%.

Strategies for growth

With sea space limitations, Mowi must find other ways to grow its profitability. The call touched on some possibilities.

Technical improvements at sea: Even when holding basically the same amount of licenses in FY23 as in FY17, the company's production quota increased by 30% from about 250 thousand tonnes per license to 320 thousand tonnes. Quota increases are granted when the regional players maintain good biological control so that pest limits are not crossed.

Land support: Mowi is not investing heavily in adult land salmon farming, which I commented on in my previous post and that I believe is a good strategy. However, the company is investing in young salmon land farming (post-smolt, meaning young salmon that are ready to go into saltwater but remain in land facilities instead of open cages at sea). The company effectively expands its total biological weight capacity by holding the young salmon for longer on land. These projects contribute in the order of 15 thousand additional tonnes.

Downstream: Mowi is also investing in product processing, being able to offer packaged, sliced, and even pre-cooked products to supermarkets and food distributors. The company's downstream segment generated EUR 150 million in EBIT in 2023, making it its second-largest segment (above any salmon geography except for Norway). Again, compared with 2017, the Consumer Products segment generated only EUR 60 million in profit. The segment grew earnings by 150% in 7 years, or a CAGR of 14%.

Cost leadership: Management commented that production has increased by 9% since 2019, whereas FTEs have decreased by 6%, resulting in employee productivity growth (in harvested kilograms) of 15%. Employees make up a big portion of Mowi's cost (about EUR 700 million currently). This shows a final way of increasing profitability by driving efficiency improvements and decreasing costs.

Political risk

Salmon farming is not a loved industry everywhere. Farmers are accused of polluting the fjords (sea lakes) where salmon can be grown, which increases the industry's political risk globally.

Rent tax: In Norway, we saw the introduction of the resource rent tax. This was not a climate-related action but rather a recognition of extraordinary rents (Norway is famous for having oil effective tax rates above 75%).

Lack of support in Iceland: The latest call also had one analyst mentioning that 70% of Icelanders are against sea salmon farming. Iceland is a negligible segment for Mowi, but it is a sample of social risks. It is also one of the least exploited geographies, offering one of the last blue oceans for the industry.

Anti-trust litigation: Management also mentioned a European task force accusing Mowi and other Norwegian players of sharing market information to avoid competition in the European export spot market between 2011 and 2019. The current state of the investigation is a formal accusation, but if found guilty, fines could reach 10% of company turnover.

Valuation

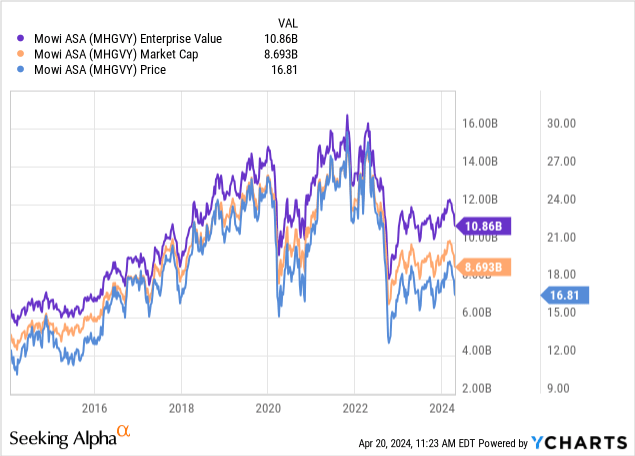

Since my last article in December, Mowi's stock price has not moved significantly, down 1.6% as of last Friday.

From an EV/NOPAT perspective, we can believe the company, and consider that the effective tax rate of its operations will increase from about 22% to 32% over the long term. With an EV of $10.9 billion, and operating profits of EUR 980 million for the year, the company generated a NOPAT of EUR 665 million ($710 million) for an EV/NOPAT multiple of 15x.

Today, Mowi trades for a market cap of $8.7 billion, and generated a net income of EUR 440 million ($470 million), or a P/E ratio of 18x. However, the company recorded EUR 230 million in deferred taxes from the Norway resource rent tax, which are not attributable to this year's operations. Part of these should be added back for a more recurring figure. As in the EV/NOPAT example, we can use 32% as a long-term rate. From the pre-tax income of EUR 900 million, we would reach an adjusted net income of EUR 610 million ($650 million), or a P/E ratio of 13.5x.

If we consider that Mowi pays most profits as dividends and that after five years, we can sell the stock for the same P/E ratio (13x does not seem super optimistic in this respect), then in order to generate a 10% return, the company needs to grow profits at a 5% CAGR.

We should also consider that Mowi's current profits are coincident with a three-year bull market in salmon prices, which could revert. The salmon industry is not as cyclical as other food industries because of the structural limitations to production growth. Overall, though, the company has grown EBIT at a CAGR of about 5% since 2010, spanning at least three to four cycles, so our 5% forward growth assumption is not crazy optimistic.

For a company of Mowi's quality and leadership characteristics, a P/E of 13x, or an expectation of 5 years of 5% profit CAGR for a return of 10% does not seem exaggerated. I believe the company is fairly valued. However, in order to consider it an opportunity I would like to see lower prices, offering a higher potential return.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.