Bill Oxford

Beam Therapeutics Inc. (NASDAQ:BEAM) is a biotechnology firm dedicated to developing precision genetic treatments. It uses base editing to correct single DNA letters, chemically changing one DNA base to another without the double-stranded breaks applied in earlier technologies. This innovation offers precise, safer, one-time treatments for genetic disorders like sickle cell disease, beta-thalassemia, alpha-1 antitrypsin deficiency, and T-cell Leukemia/Lymphoma. Additionally, the company secured $675 million in upfront payments from agreements with Pfizer, Apellis, Verve, and Sana. However, from an investment perspective, BEAM appears to be trading at a relatively high valuation multiple, which detracts from its investment appeal. So, on balance, I think its premium valuation offsets its promising fundamentals, and given the lack of Phase 3 drug candidates in its IP portfolio, I think a “hold” rating makes sense for BEAM at this stage.

CRISPR Tech: Business Overview

Beam Therapeutics was established in 2017 in Cambridge, Massachusetts. The company focuses on developing precision genetic treatments utilizing proprietary base editing technology. Their technology, anchored in CRISPR-based methods, allows for precise single-letter changes in the DNA of living cells, potentially enabling therapies for serious diseases. Notably, the company's origins are related to the Broad Institute of the Massachusetts Institute of Technology and Harvard University.

Source: Corporate Presentation. March 2024.

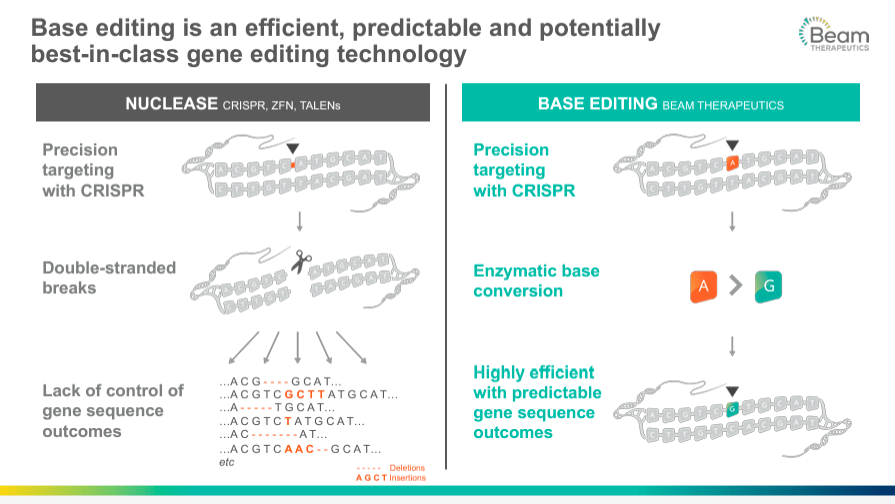

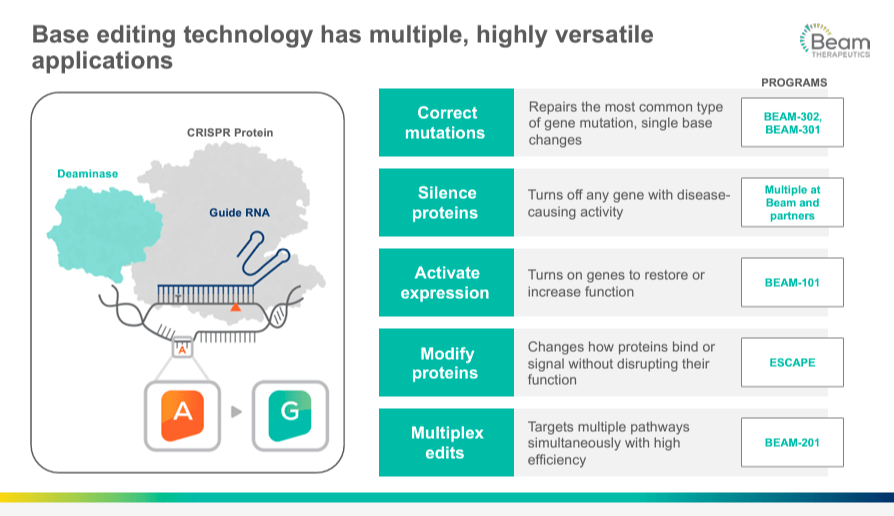

BEAM's pipeline includes a broad portfolio of programs based on gene editing, centered on using a technology known as base editing. This approach is a more precise form of gene editing than the earlier CRISPR-Cas9 system that works by creating double-stranded breaks at specific locations of the DNA. Therefore, the cell's natural repair machinery restores these breaks, and this way, the changes or edits are introduced in the DNA sequence. On the other hand, the base editing technique is a "search and replace" function for DNA, where base editors chemically change a single DNA base into another. For example, cytosine [C] can be converted into thymine [T]. This change does not rely on the cell's DNA repair processes to avoid errors or unintended modifications. With base editing, point mutations can be corrected at the genomic level, providing treatments for many genetic diseases. But more importantly, this precisely targeted approach minimizes the potential for unwanted genomic changes that could lead to negative side effects.

Source: Corporate Presentation. March 2024.

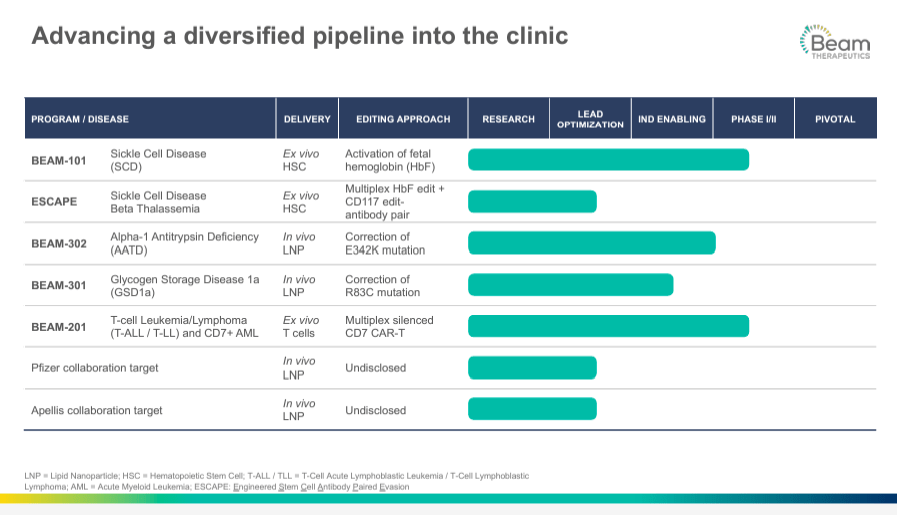

From a bird's-eye perspective, BEAM’s pipeline has five key research programs. First, 1) Beam-101 program that studies the activation of fetal hemoglobin for sickle cell disease [SCD] and beta-thalassemia. This program is in phase I/II of the clinical trials. The company’s 2) Engineered Stem Cell Antibody Paired Evasion [ESCAPE] has the same indication for SCD and beta-thalassemia, with a gene-editing strategy applied simultaneously for the CD117 gene or its expression pathway linked with a specific antibody that targets the edited cells. It is in the preclinical stage. The third 3) Beam-302 is an IND-enabled candidate, starting phase I/II, for treating alpha-1 antitrypsin deficiency [AATD] by editing the mutation of the E342K gene (PiZ mutation) involved in a change in the amino acid sequence of a protein. With this approach, BEAM can potentially restore the correct amino acid mutation for AATD by converting glutamic acid [E] to lysine [K].

It’s also worth noting that 4) Beam-301 is a project that treats glycogen storage disease 1a [GSD1a]. It is also IND-enabled for developing a correction of a specific mutation where arginine [R] is replaced by cysteine [C] at the 83rd position in the protein sequence. Lastly, the company’s 5) Beam-201 is a cell therapy for certain cancers such as T-cell Leukemia/Lymphoma. CAR-T medicine involves modifying T cells (immune cells) to express a Chimeric Antigen Receptor [CAR] that targets cancer cells. Multiple genes, including the gene for CD7, a protein on the surface of T cells, are silenced to prevent the CAR-T cells from attacking each other, increasing the survival of the therapeutic cells. This therapy is indicated for refractory T-cell acute lymphoblastic leukemia/lymphoma and is in phase I/II. Additionally, BEAM's pipeline includes collaborations with Apellis (APLS) and Pfizer (PFE) to develop several preclinical drug candidates.

Source: Corporate Presentation. March 2024.

With such a robust and diverse product pipeline, BEAM is positioned as a leader in precision genetics. They focus on developing innovative therapies using advanced gene editing systems like base and prime editing, which is a key IP differentiator. However, investors must remember that their programs must still be in Phase 3, meaning that FDA approvals are still years away.

Deals Boost BEAM's Innovation and Financials

It’s also worth mentioning that BEAM has strategic deals with Pfizer, Apellis, Verve (VERV), and Sana (SANA), resulting in $675 million in upfront payments and potentially more than $1 billion in milestone payments. These payments correspond to $300 million upfront from Pfizer for three base editing targets, with an option to share costs and profits at the end of phase I/II. From Apellis, BEAM obtained an upfront payment of $75 million license for base editing in complement-mediated diseases and potential additional rights to US rights at the end of phase I trials (50% of US rights). From Verve, BEAM received $250 million, comprising an upfront payment and an equity investment. Additionally, BEAM can receive up to $350 million in future payments based on achieving these program's milestones. Similarly, BEAM has received $50 million upfront from Sana Biotechnology for a non-exclusive license to Cas12b nuclease, a gene editing tool, in developing engineered cell therapies. Cas12b is a type of CRISPR enzyme used to make precise edits to DNA.

Overall, I believe these deals reflect a strong cash inflow potential to support BEAM's research. These collaborations, particularly with Pfizer for base editing targets, and the upfront payments from other strategic partners paint a promising financial outlook for BEAM. However, all of these are still contingent on successfully researching and developing their respective programs, which adds a layer of risk to these otherwise promising partnerships.

Source: Corporate Presentation. March 2024.

Likewise, BEAM has signed innovator deals with Prime Medicine (PRME) and Orbital (OTC:OIGBQ) to gain rights for new and complementary technologies. BEAM has secured exclusive rights to Prime Medicine's prime editing system for precise DNA edits to enhance base editing capabilities, enabling changes such as converting adenine [A] to guanine [G] and cytosine [C] to thymine [T], crucial for addressing mutations in diseases like SCD. Also, BEAM's investment in Orbital's RNA delivery technologies enhances precision and efficiency in gene-editing tools. These technologies improve the accuracy and efficiency of delivering RNA molecules that guide gene-editing tools to the right genome location. These acquisitions allow BEAM to enhance its gene editing capabilities and improve the delivery mechanisms for its therapies, demonstrating its commitment to maintaining a competitive edge in genetic medicine.

Embedded Premium and Catalysts: Valuation Analysis

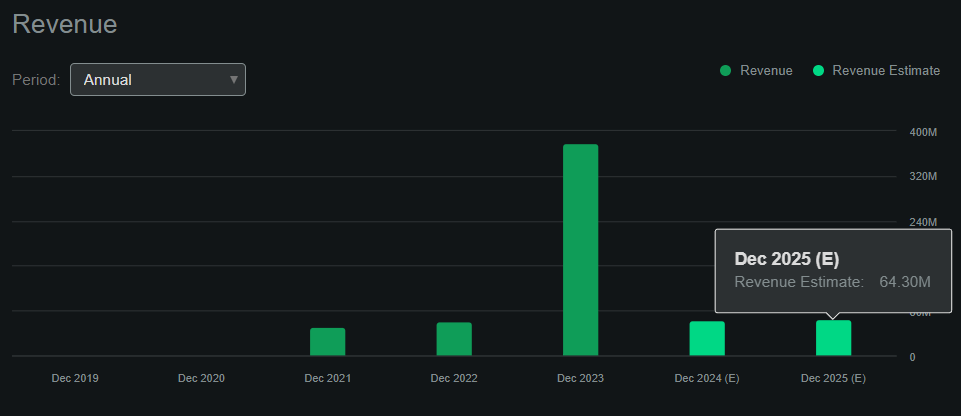

From a valuation perspective, BEAM currently has a $1.88 billion market cap, which is relatively big for a biotech company that is still in the research stages. It’s noteworthy that their revenue for 2023 jumped significantly to $377.71 million, but it was mostly related to license and collaboration agreements, which is why their future revenues are much lower. According to Seeking Alpha’s dashboard on BEAM, the company is projected to generate just $64.3 million in revenue by 2025. Also, note that by yearend 2023, BEAM had deferred revenue of roughly $178.6 million related to these partnerships. While this is noteworthy, it’s also clear that the company isn’t generating any revenue from product sales yet, which somewhat caps more predictable revenue-generation forecasting methods.

Source: Seeking Alpha.

Nevertheless, BEAM’s balance sheet is well capitalized for now, with $435.9 million in cash and $754.0 in marketable securities it can sell if needed. Even though BEAM holds essentially no debt, it's worth noting that the company has $172.7 million in lease liabilities, which will eventually be cash obligations. If we look at its latest quarterly cash flow statement, I estimate the company burned through $138.7 million. I obtained this figure by adding its CFOs and Net CAPEX. If we annualized that quarterly cash burn, it implies BEAM burns through $554.8 million yearly. This means that the implied cash runway is about 2.1 years, which is healthy but not outstanding. Plus, BEAM had to sell some of its marketable securities in Q4 2023 to fund its operations, which shows that its cash balances may be running low already.

Hence, it's unsurprising that at the end of 2024, BEAM will likely need to start looking for additional financing sources, assuming it doesn’t implement cost-cutting measures. For now, it’s safe to say that the company has enough liquidity to maneuver and continue developing its product pipeline. I think the latest filing for an additional capital raise as needed is a yellow flag. Still, it is necessary as it would give the company more financial flexibility if required. However, if they do it through equity, it would lead to significant stock dilution.

Source: BEAM's 2023 10-K.

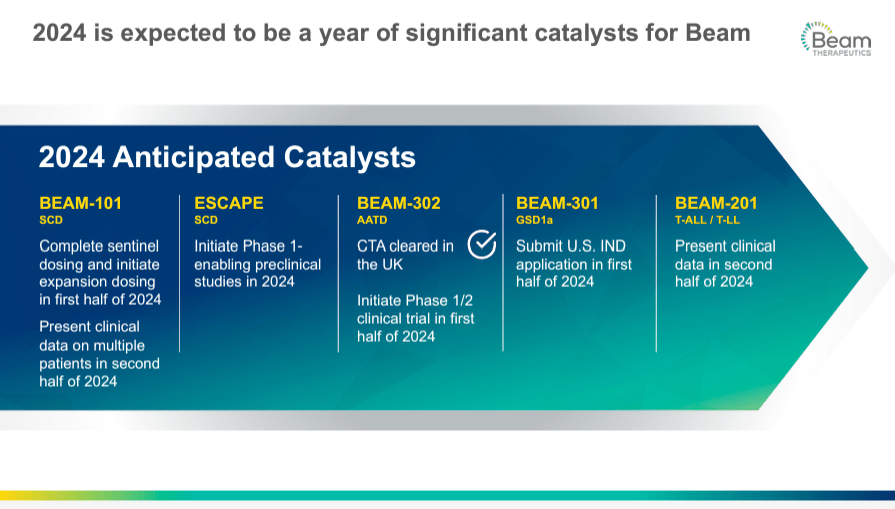

As for upcoming catalysts, Beam-301 and Beam-201 are particularly promising. The first one should see the IND application in 1H2024, while the latter is still undergoing Phase ½ trials, with initial clinical data expected by 2H2024. Successful updates regarding these two would surely support the stock as investors gain confidence in R&D progress. However, revenue-wise, I think investors should be cautious. 2023 was an exceptional year for BEAM, mostly fueled by the agreement with Lilly. This deal accounted for a significant portion of 2023's revenue, suggesting that future revenue streams might not be as substantial without similar large-scale deals, which adds a considerable risk layer.

Wait for a Better Price

Therefore, getting a reasonable valuation multiple for BEAM is difficult, since 2023 should be considered an outlier year rather than the norm. We could take the average of the 2023 revenues, with the forecasted revenues for 2024 and 2025, to get a better P/S multiple. This approach would give us an average revenue of $168.5 million. Thus, this figure would imply a forward P/S multiple of 11.2, which is relatively high, especially for a biotech company without any Phase 3 drug candidates in its pipeline. Moreover, the sector’s median forward P/S multiple is just 3.4, further corroborating the notion that BEAM trades at a significant premium relative to peers.

Source: TradingView.

So, when we take it altogether, I see that BEAM is an incredibly promising biotech company with potentially disruptive technology. However, the market seems fully aware of such potential, so it trades at a significant premium today. Moreover, the potential for stock dilution stemming from the recent shelf registration adds a risk layer that investors can't ignore. Revenue sources are highly unpredictable as they come from partnerships rather than product sales at this stage, increasing the uncertainty related to the underlying business.

Also, there don’t seem to be substantial catalysts that can significantly improve BEAM’s valuation in the near term other than updates on Beam-301 and Beam-201 development progress. Plus, FDA approval processes are fraught with uncertainty. Hence, I think being bearish is impossible, but leaning bullish might not be appropriate due to valuation concerns and a lack of major catalysts in the near term. Thus, I rate BEAM a “hold” for now, but I think the stock would be a fantastic investment at lower valuation multiples.

Caution is Advised: Risk Assessment

I believe BEAM’s investment profile undoubtedly has upside potential in the long run. Yet, it’s impossible to ignore the risks embedded in the equation at this juncture. In particular, I identified its relatively high valuation multiple as the prime reason that tempers my optimism in the stock. However, the underlying business itself is also packed with uncertainties regarding the dependence on unpredictable partnership revenue streams and the glaring lack of Phase 3 drug candidates. This, coupled with the previously mentioned stock dilution risk and a lack of major catalysts, is concerning, especially when new investors today have to ostensibly hold for the long term to get to a potential FDA approval that would unlock shareholder value.

Additionally, BEAM’s trailing twelve-month CFI turned positive for the first time in Q1 2023, primarily due to a strategic shift from investing in short-term securities to selling them for liquidity. Note that BEAM's net income for Q4 2023 was also positive for the first time, which I consider an outlier due to the substantial increase in quarterly revenue. The ongoing drawdown of investment securities could suggest that BEAM's liquidity might appear better due to asset sales despite having a record revenue quarter in Q4 2023. It’s also undeniable that BEAM's positive cash flow for Q4 2023 was also influenced by its quarterly net income of $142.8 million. Still, $99.5 million came from changes in unearned revenues, indicating that much of that was non-cash. Moreover, my estimated cash runway of about 2.1 years suggests caution regarding BEAM’s liquidity. Given this overall context, I think it's prudent to monitor BEAM's financial position closely, especially considering that the record revenue in Q4 2023 seems an outlier and not the norm for BEAM when assessing its true liquidity situation.

This is why the stock has historically been a highly volatile security, even by biotech standards. For instance, BEAM traded as high as $49.50 per share in February of this year, only to be at $24.10 just a couple of months later. This is a 51.3% drawdown in a very short timeframe and testifies to how volatile BEAM can be. Given that the stock is likely still trading at a significant premium, there could be even further downside before BEAM trades more in line with its peers. Thus, the price risk in BEAM is also significant as well. All of these factors combined led to me taking a cautious stance on the stock.

Lean Neutral: Conclusion

Overall, BEAM is a promising biotech stock trading at a high premium relative to peers. This is somewhat justified due to its innovative approach to precision genetic treatments, yet such a premium detracts from its investment appeal. Additionally, I don’t see major catalysts for BEAM’s product pipeline, further corroborating the notion of leaning neutral on the stock. Financially, BEAM is well positioned to see through its research programs, which is a green flag. However, the waiting time will be at least a few years since its IP portfolio remains relatively early with no Phase 3 drug candidates. Thus, I think there’s a good chance that investors will eventually be able to pick up BEAM shares at better prices, which is why I rate the stock a “hold” for now.