Its been a dismal episode riding this slide the past year or so.

However I would not write off New Zealand Energy, just yet.

In the category it falls into, junior E&P, it has just started producing oil in Q1, and although at a slower pace, than its followers may wish - more patience is needed to follow this play through 2014.

We could be near a bottom, and for the risk tolerant investor, this could be the entry point that can make you some $ if you weigh the odds of what might yet be in the ground on both sides of the island.

Photo above was the Waihapa Acquisition that occured in 2013

Click Links: April Presentation

More Links below: (click headlines)

I know the charts show a clear selling trend. I just don`t think the charts do anything but explain the markets adversity to risk right now. The charts tell what happened, not what is going to happen. I cannot predict what is GOING to happen any more than you can, however I have reason to suspect the market is over punishing NZERF, V.NZ and that can translate to a trading opportunity in the next couple of weeks.

I am sticking my neck out and going to suggest that the chart trend will be proven wrong by May 9th, and that the numbers coming out on May 5th or shortly after will be slightly better than guidance suggested.

There are a number of near term wells that are not part of the Q1,Q2 production updates. Its not going to be the boost that gets people really really excited just yet, but it will likely be moderately better than march and help put positive investor sentiment back into believing NZEC is capable of improving production Quarter to Quarter.

The real catalyst, may not come from NZEC at all, and instead may be the reporting of two things by NZEC`s competitive neighbor (Tag Oil). The first being what was learned from drilling their first onshore Kapuni well, and second and perhaps more relevant, what the results were on the East Coast well drilled by Tag Oil last year.

In a short time frame both events above should be material to how an investor views the massive acreage position that New Zealand Energy sits on (both in Taranaki, and East Coast).

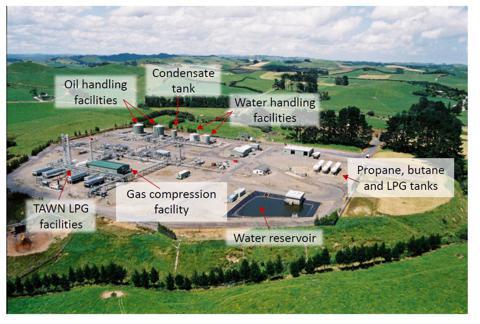

Last year $33.5 MM was spent to acquire this facility below.

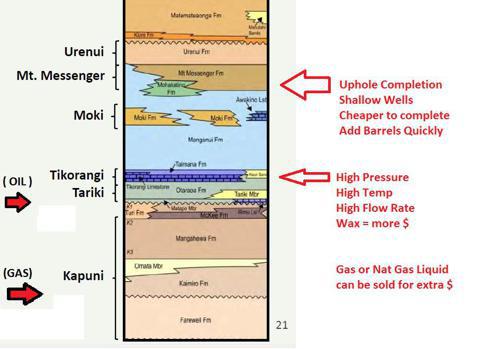

Right now most of the production is shallow, from Moki.

The bigger future for this production station is likely from deeper, the Tikorangi, which is challenging to drill and complete but produces under great pressure and flow rates before declining due to a variety of geological and reservoir engineering reasons.

Deeper than Tikorangi, lies the Kapuni, a proven offshore basin, which tag oil (next door) recently attempted a deep exploration well chasing natural gas. In the event that well proves commercial, then New Zealand Energy sits on top of the same geology with their Waihapa Acquisition.

The drilling permits acquired with the production facility offer large future farm-in opportunities on exisiting permits. This is not to be underestimated, as we are still early in delineating how large Taranaki is and what its resource quantity is.

Now to the real kicker, which is longer term, still speculative, but the real reason you should read everything you can on all players in New Zealand (and soon).

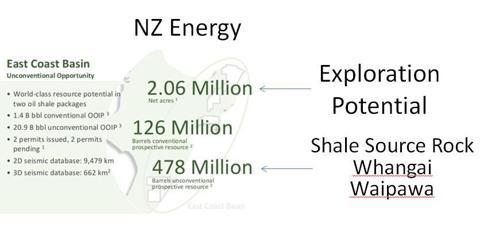

New Zealand might have its own Bakken. An upto 600m thick shale play on the east side of the island. In case you aren`t aware, 600m is very, very thick for a payzone and this could translates to economic quantities of oil (enough to shift geopolitical equations).

NZEC has a very large acreage position of over 2 million net acres (exploration permits) in the fairway of the Whangai and Waipawa source rocks (shale) and geoscientists believe it could hold a substantial size of oil, comparable to North Dakota, or even larger.

The east coast is highly attractive for its exploration potential, and by this summer 2014 we should have much more information on just how the initial east coast exploration went last year.

Disclaimer: Oil Exploration is extremely risky and you should not take this blog as investment advice. You should read all the cautionary statements and investor disclosures of all companies mentioned and hire or consult with a competent advisor before jumping into any risky investment decision.