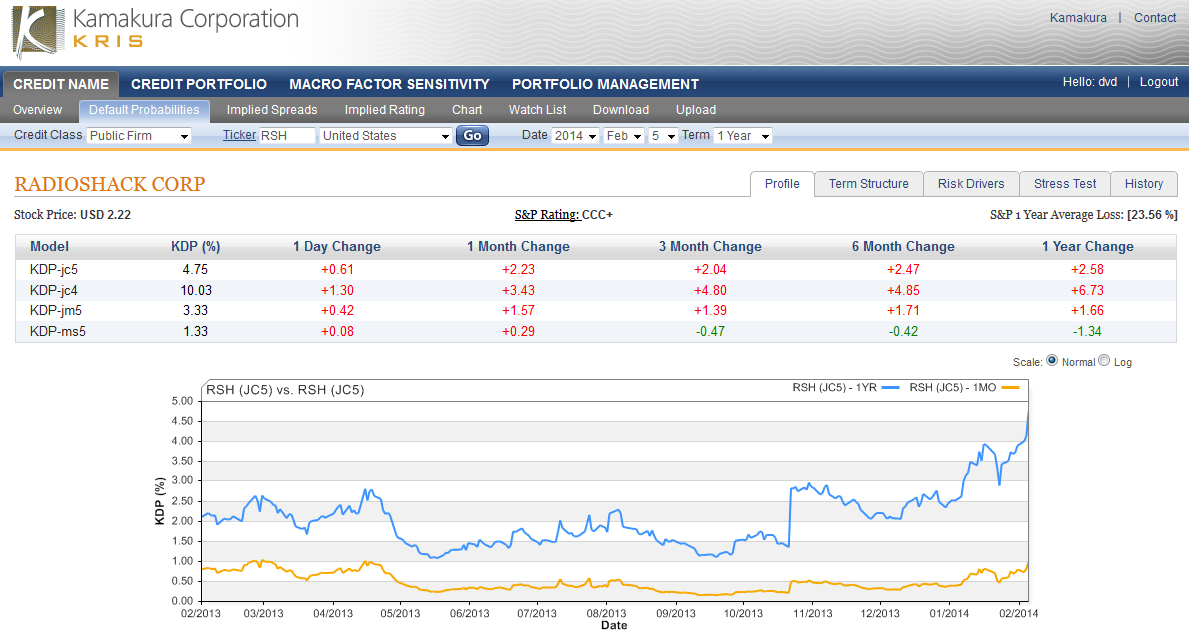

The blue line is the firm's one year default probability. The yellow line is the annualized one month default probability.

Background on the Default Probability Models Used

The Kamakura Risk Information Services version 5.0 Jarrow-Chava reduced form default probability model ( abbreviated KDP-jc5) makes default predictions using a sophisticated combination of financial ratios, stock price history, and macro-economic factors. The version 5.0 model was estimated over the period from 1990 to 2008, and includes the insights of the worst part of the recent credit crisis. Kamakura default probabilities are based on 1.76 million observations and more than 2000 defaults. The term structure of default is constructed by using a related series of econometric relationships estimated on this data base. KRIS covers 35,000 firms in 56 countries, updated daily. Free trials are available at Info@Kamakuraco.com. An overview of the full suite of Kamakura default probability models is available here.

General Background on Reduced Form Models

For a general introduction to reduced form credit models, Hilscher, Jarrow and van Deventer (2008) is a good place to begin.

Hilscher and Wilson (2013) have shown that reduced form default probabilities are more accurate than legacy credit ratings by a substantial amount. Van Deventer (2012) explains the benefits and the process for replacing legacy credit ratings with reduced form default probabilities in the credit risk management process. The theoretical basis for reduced form credit models was established by Jarrow and Turnbull (1995) and extended by Jarrow (2001). Shumway (2001) was one of the first researchers to employ logistic regression to estimate reduced form default probabilities. Chava and Jarrow (2004) applied logistic regression to a monthly database of public firms. Campbell, Hilscher and Szilagyi (2008) demonstrated that the reduced form approach to default modeling was substantially more accurate than the Merton model of risky debt. Bharath and Shumway (2008), working completely independently, reached the same conclusions. A follow-on paper by Campbell, Hilscher and Szilagyi (2011) confirmed their earlier conclusions in a paper that was awarded the Markowitz Prize for best paper in the Journal of Investment Management by a judging panel that included Prof. Robert Merton.Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.