One of the challenges and pleasures of being a (lower case) macro man is the intellectual challenge of finding tradeable themes. Sometimes they fall into your lap, such as last year's "implosion of the world financial system" theme. In other environments, things can become a bit trickier, not least because timing is just as important as direction in implementing a trade.

One of Macro Man's core views for the past several months has been that following the gradual waning of the financial crisis, there remains a bone-crushing recession to cope with in 2009. One of the direct outcomes of the hit to global domestic demand is, unsurprisingly, sharply falling trade volumes.

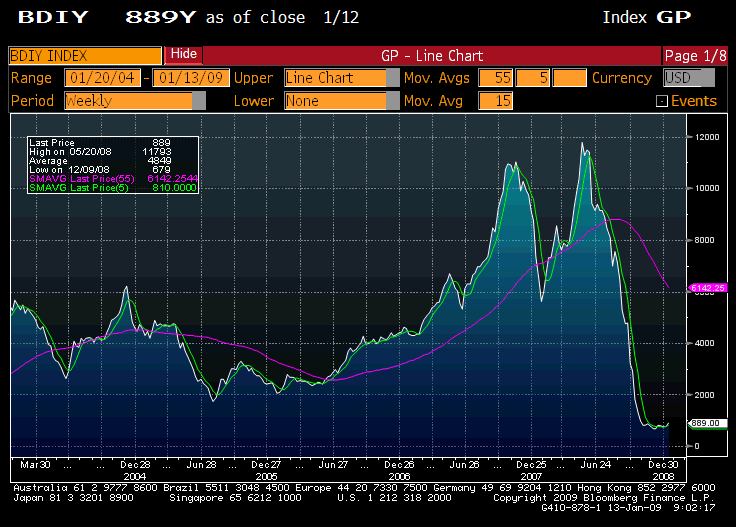

Last summer, the Baltic Dry Freight Index collapsed, a move which at the time was characterized as somewhat overdone. Since making a low late last autumn, the index has essentially flat-lined, implying that there is little to no fresh marginal demand for shipping.

Trade data around the world has subsequently confirmed the message from the BDIY. Taiwanese exports fell 41% (!!!!) y/y in December, while trade figures throughout the rest of Asia have shown similar weakness (if not quite of the same magnitude).

Now, there is a popular view that while current data is poor, the stimulus packages in China will bail out the Asian region if not the world. Macro Man is sceptical. Indeed, the greatest risk to asset prices is that the Chinese stimulus is a damp squib. And if you need any reminders of what that means for the world, check out the chart below, which shows China's trade balance with the rest of Asia. China usually runs a tasty deficit with Asia, as they import components for onshore assembly and re-export. Observe how China has managed to shift demand abruptly lower with Wal-Mart style ruthlessness.