Just a few weeks ago I wrote a Seeking Alpha article on Medical Properties Trust (NYSE:MPW), the only "pure play" Hospital REIT with a Total Capitalization of around $3.5 billion. In that article I summarized the company's latest (Q4-13) results and I suggested that MPW "does not have to do any new acquisitions to achieve the $1.10 FFO per share for 2014".

I added that "the $1.10 FFO run rate that MPW announced is not guidance for 2014. This $1.10 is what the company said it had in place as the FFO run rate. This does not include any acquisition activity for 2014, which the company guided (earnings call) to be $500 million for 2014".

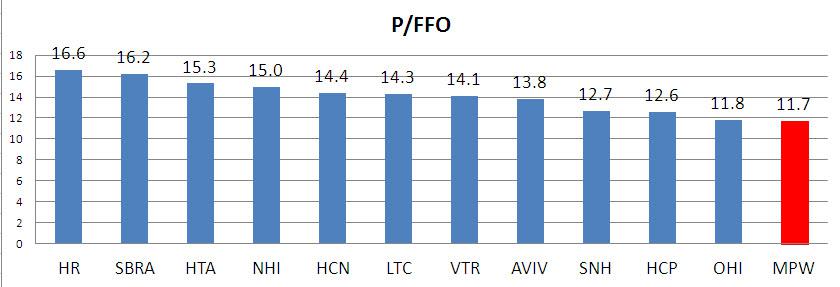

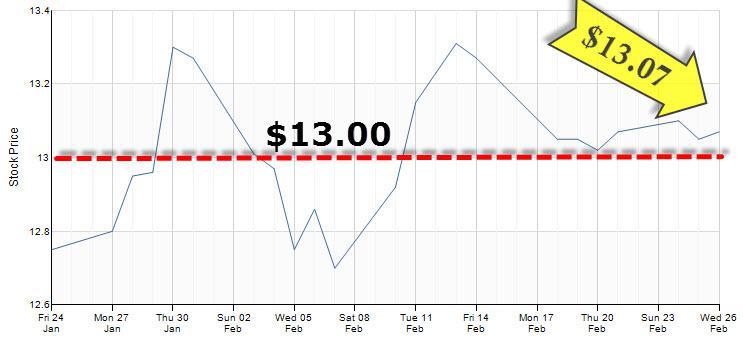

Simply said, MPW appears to be doing a great job with managing its capital allocations prudently. I summed up my latest article with a bullish recommendation and BUY price of $13.00 or less. It's my view that MPW shares could hit $17 over the next 12 months and my premise for the increase is because I believe that MPW's Price to Funds from Operations (P/FFO) multiple could move more in-line with other Health Care REIT multiples.

MPW is currently trading at $13.07 a share, moving closer to my $13 BUY Target. With a dividend yield of 6.43% it's possible that I may soon accumulate additional shares and take advantage of stock that's trading at "soundly valued margin-of-safety".

As a shareholder, or even as a prospective shareholder, it's critical to evaluate the management team of a REIT security. Over the previous few weeks I have been providing exclusive interviews with several REIT CEOs. More recently I have provided articles (with Q&A interviews) with Ben Butcher, CEO of STAG Industrial (STAG), Scott Peters, CEO of Healthcare Trust of America (HTA), and Debra Cafaro, CEO of Ventas, Inc. (VTR).

In this article I wanted to provide you with relevant insight into the management team and CEO of Medical Properties Trust.

Edward K. Aldag, Jr. is Chairman, President, and CEO and he has served in the capacity since the company was founded in 2003. Aldag was instrumental in creating MPW where he assembled the management team that exists today. Aldag has deep roots in medical property finance and he has built a circle of competence around structured finance and the monetization of hospital-related assets.

As I referenced in a previous article, investors deserve to understand "the business behind the business". That's why I asked Edward Aldag, the CEO of Medical Properties Trust, to answer a few questions exclusively for Seeking Alpha.

Thomas: For 2013, MPW's normalized Funds From Operations (or FFO) increased by 35% over a two-year period. What's driving that growth and are the acquisitions sustainable?

Aldag: As a hospital-focused, net lease REIT with long-term leases, immediate and strongly accretive acquisitions have driven our dramatic growth during the last couple of years, and we expect these types of transactions to continue to be the primary driver of FFO growth in the future. By the way, on a run rate basis without any provision for this continued growth, our in-place FFO as of years' end should add up to an additional $0.10 per share in FFO.

Hospital operators need to lock in long-term financing and this dynamic has supported tremendous opportunities for MPW resulting in our completion of $1.5 billion of acquisitions in 2012 and 2013. We believe that the continued consolidation in the hospital market will also fuel this growth.

To complement this rapid external growth, we structure our long-term leases to include pre-determined, inflation indexed annual rental escalators, which not only provide inflation protection but also provide internal growth even in times of low inflation.

Given the size of the hospital real estate market, which we estimate at almost $500 billion, and the strength of our acquisition pipeline, we are confident that we can continue to drive solid FFO growth moving forward.

Thomas: In 2012, MPW made $800 million in investments and in 2013 approximately $700 million in investments. What is your guidance for 2014 and how much do you expect to buy in Europe?

Aldag: We recently raised our acquisition guidance for 2014 to $500M from $400M in 2013 based upon our very strong pipeline. We expect the great majority of our acquisitions will be in the U.S.

Since the inception of our company we have always looked at cross border investments as a way for MPW to diversify. We love the hospital market in the U.S. We understand the hospital market in the U.S., but we also believe that it is very prudent for us to diversify our portfolio into other stable areas outside of the U.S. We expect our investments will grow in Europe this year and we continue to look at other opportunities inside and outside of Europe. We have not put an exact percentage on our goal of investments outside of the U.S., but the U.S. hospital market will continue to be the largest part of our portfolio by far.

Currently, the U.S. market represents approximately 93 percent of our portfolio, and we expect the U.S. will remain our dominant market for the foreseeable future.

Thomas: How will the ACA impact MPW now and in the future?

Aldag: As we have predicted since the legislation was enacted, we believe the Affordable Care Act's impact on MPW will be limited.

Some have argued that it will be a positive for hospitals, as more individuals become insured and gain access to health care, and that is a logical argument, but we do not anticipate material changes to our operators' performance. We believe the tradeoffs from the insured to the previously uninsured will be essentially neutral. Regardless, we believe the overall pool for health care funding will continue to increase at a modest rate in the years ahead, which provides a stable environment for MPW.

Hospital operators have had plenty of time to adjust to changing expectations and, if there is continued shift from fee-for-service to outcome-based reimbursements, operators will be able to make that adjustment. The fundamental premise remains: hospitals are critical pieces of communities' infrastructure and experienced operators will successfully adapt as our healthcare delivery system continues to experience change.

Thomas: Do you see MPW becoming investment grade rated this year or next?

Aldag: It is certainly a logical progression to assume that at some point in the near future the rating agencies will move us up the one or two notches needed to get there. We have always managed this company using a prudent balance sheet with an investment thesis that has created a strong stable diversified portfolio. As we have grown from zero assets to more than $3.0 billion in 10 years the rating agencies have duly noted our success, including our strong and liquid balance sheet, operator and geographical diversification, and disciplined investment philosophy.

Moody's upgraded our senior unsecured debt rating to Ba1 from Ba2 in March 2012, and we are currently on a positive outlook from Standard & Poor's. We will maintain our selected leverage targets of 40-45% debt to gross assets and debt to EBITDA of 5.0 to 5.5x while continuing tremendous growth.

Thomas: Is there more risk in owning assets in Germany? What returns are you getting in Germany?

Aldag: Investors and respected economists view Germany as a very stable country, both politically and economically, and its healthcare system is very stable as well. The German rehabilitation market (which includes our facilities) serves a broad scope of treatment with more rehabilitation facilities and beds than the U.S. The reimbursement comes from a well-established system of public and private funds.

Since economic cycles in Europe don't always sync with the U.S., we believe some exposure in Germany creates additional geographical diversification for our portfolio and further reduces the overall risk of our already highly derisked portfolio.

We are very pleased with our recent acquisition, and have found that returns on investment in Europe are generally similar to those in the U.S.

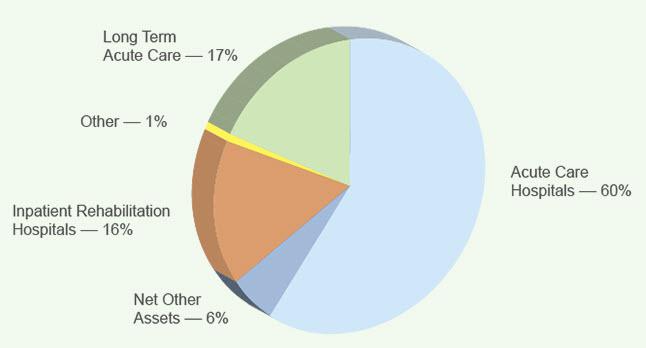

Thomas: MPW has around 57% in Acute Care. Do you expect that to change? Why?

Aldag: The recent RHM and Ernest transactions have driven the percentage of our portfolio invested in Acute Care hospitals to below 60%.

These transactions have created tremendous opportunities for MPW and our shareholders. Eventually we envision our portfolio returning to approximately 70% in the Acute Care sector over time where we have the highest lease coverage at approximately 5.4x. This sector remains the foundation of our portfolio.

Thomas: Why doesn't MPW issue preferred stock?

Aldag: With our current capital structure, we have achieved an attractive blended cost of capital that has dramatically improved in recent years.

That said, we will continue to be opportunistic in the capital markets and evaluate the relative merits of common stock, preferred stock, limited asset sales, joint ventures, and other strategies. In the last six months, we have had two very successful long-term bond financings and we are also experienced issuers in the bank and convertible bond market.

Moving forward, we are open to all options that maximize accretion while allowing MPW to maintain a strong balance sheet.

Thomas: MPW recently announced a 5% dividend increase, the first increase in five years. Do you believe there is room for future increases?

Aldag: Our management has always focused on total return to shareholders, and our dividend is a big overall contributor to this.

Our goal for our dividend payout has been approximately 75-80% of our normalized FFO, which is right where we are today.

As normalized FFO increases in the years ahead through both internal and external growth, our Board will consider dividend increases as appropriate.

Thomas: How well has MPW prepared for rising interest rates?

Aldag: MPW has followed the practice of matching our portfolio with fixed-rate debt and/or newly issued common equity, thereby mitigating the concern that rising interest rates will negatively affect our cash flow in the near term.

As of December 31, 2013, approximately 85% of our debt is fixed, so we have limited exposure to variable interest rates. Additionally, our leases provide for annual rental increases with most lease payments rising with increases in CPI.

Thomas: Ed, thank you for taking the time to answer these questions. Good luck and see you again soon.

People Behind the Property: My next "people behind the property" interview will be with Taylor Picket, CEO of Omega Healthcare Investors (OHI).

Other REITs mentioned: (SNH), (HCN), (SBRA), (AVIV), (NHI), (HCP), (HR), and (LTC).

REIT Newsletter: For more information on REITs, check out my monthly newsletter HERE.

Disclaimer: This article is intended to provide information to interested parties. As I have no knowledge of individual investor circumstances, goals, and/or portfolio concentration or diversification, readers are expected to complete their own due diligence before purchasing any stocks mentioned or recommended.

Disclosure: I am long O, DLR, VTR, HTA, STAG, UMH, CSG, GPT, ARCP, ROIC, MPW, HCN, OHI, LXP, KIM. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.