Freeport-McMoRan (NYSE:FCX) is a stock that investors need to be cautious on, especially with the Q1 earnings report next Tuesday. While the company is now more focused on strengthening their balance sheet, which is a positive development, shareholders need to recognize how highly negative the operating environment was in Q1 and the effect it has on the upcoming earnings report, which will likely lead to a miss.

Source: Freeport-McMoRan

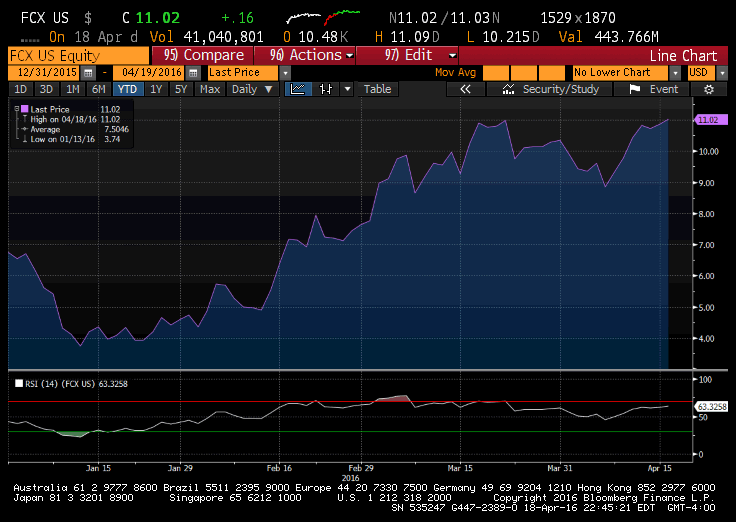

Backing Up

Commodities, including copper, have significantly rallied out of their February lows and really finished Q1 strong. On top of that, Freeport was the beneficiary of a new position by David Tepper of 3.6 million shares and was the beneficiary of an increased stake by none other than Carl Icahn. Additionally, short covering has significantly helped fuel the rally. On January 29, 222 million shares were short and now just 144 million remain short. That's a 35.14% decrease in the amount of shorts. Below you can see the positive reaction in FCX's stock.

Source: Bloomberg

Capex Cut Will Lead To A Delayed Recovery

As I've stated numerous times on Seeking Alpha, I look for companies with significant potential to grow. If possible, I look for these types of companies to have growing, but sustainable dividends.

Freeport's capex is down 29% from mid-2015 and will retract 47% in 2017. These cuts were necessary, in my opinion, otherwise cash flow would have seen significantly worse adverse effects. Interestingly enough, although the company started cutting capex last year, free cash flow has only grown to be more negative. From Q2 to Q4, it decreased from -$592 million to now -$686 million. This trend even occurred as the dividend was cut to $0.05. That dividend was fully cut back in Q4 because of their trouble managing cash flows in light of their $19.8 billion in LT debt.