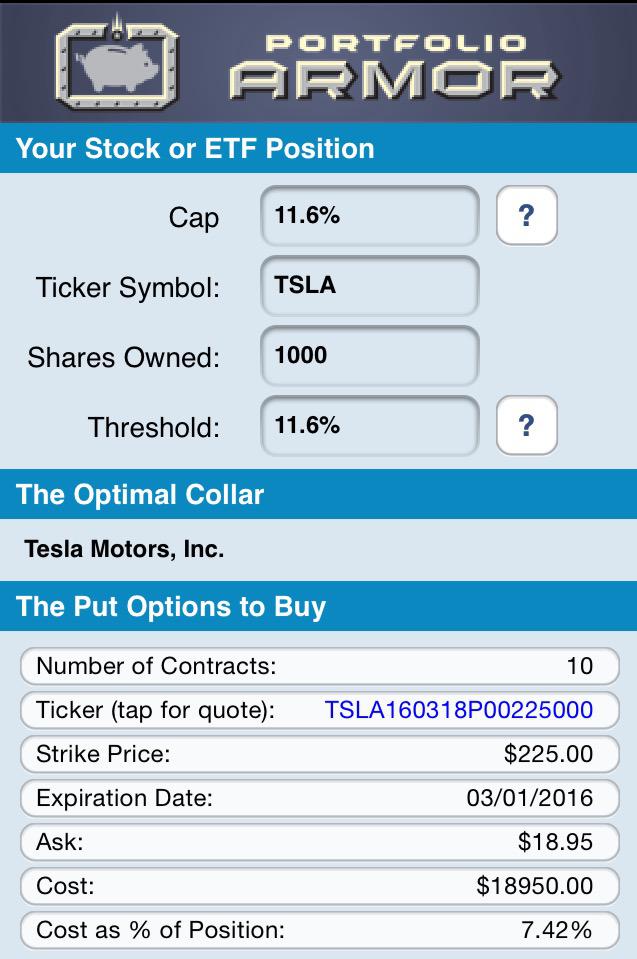

Shares of Tesla (TSLA) dropped 5.16% Monday, as the market as a whole sold off. In an article published on Friday ("Adding Downside Protection To Tesla"), we discussed headwinds facing the company and presented this Tesla hedge created as of last Wednesday's close:

The Optimal Collar To Hedge Tesla

This was the optimal collar, as of Wednesday's close, to hedge 1000 shares of TSLA against a greater-than-11.6% drop before March, while capping an investor's potential upside at 11.6% over the same time frame.

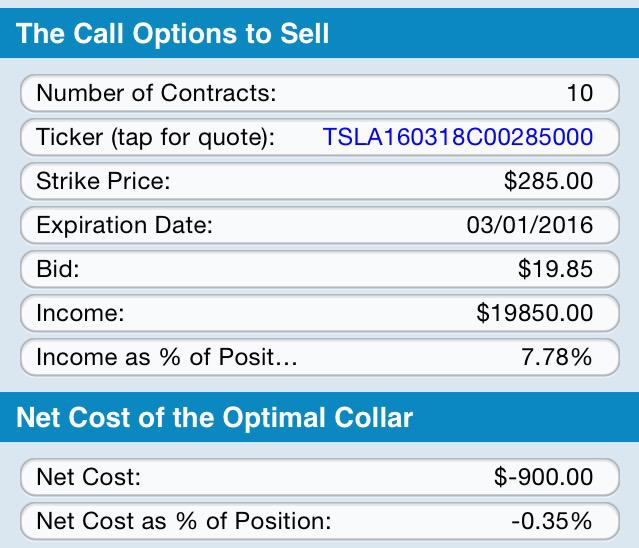

As you can see at the bottom of the screen capture above, the cost of the put leg of this collar was $18,950, or 7.42% of position value. However, as you can see below, the income generated from selling the call leg of the collar was $19,850, or 7.78% of position value.

So, the net cost of this collar is actually negative, meaning a Tesla investor would have collected more from selling the calls than he would have paid for buying the puts. In a sense, he would have been getting paid to hedge.

How That August 19th Hedge Responded To Today's Drop

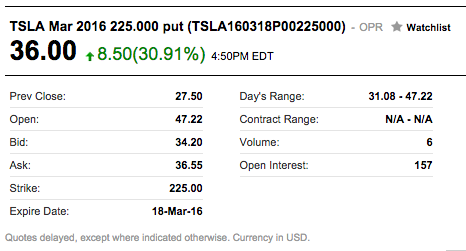

Here is an updated quote on the put leg as of Monday:

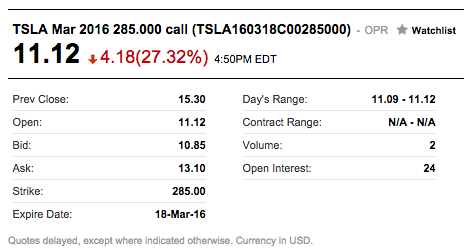

And here is an updated quote on the call leg:

How That Hedge Protected Against Today's Drop

TSLA closed at $255.25 on Wednesday, August 19th. A shareholder who owned 1000 shares of it and opened the collar above then had $255,250 in TSLA stock plus $18,950 in puts, and if he wanted to buy-to-close his short call position, he would have needed to pay $19,850 to do that. So, his net position value for TSLA on August 19th was ($255,250 + $18,950) - $19,850 = $254,350.

TSLA closed at $218.87 on Monday, August 24th, down 14.3% from its closing price on August 19th. The investor's shares were worth $218,870 as of 8/24, his put options were worth $36,000 and if he wanted to close out the short call leg of his collar, it would have cost him $11,120. So: ($218,870 + $36,000) - $11,120 = $243,750. $243,750 represents a 4.2% drop from $254,350.

More Protection Than Promised

So, although TSLA had dropped by 14.3% at the time of the calculations above, and the investor's hedge was designed to limit him to a loss of no more than 11.6%, he was actually down only 4.2% on his combined hedge + underlying stock position by this point.

Options Give You Options

Being hedged gives an investor breathing room to decide what his best course of action is. An TSLA investor hedged with this collar could exit his position with an 4.2% loss now (instead of a 14.3% loss), he could wait to see what happens, or if he remains a long term bull, he could buy-to-close the call leg of this collar, to eliminate his upside cap. If he's even more bullish, he could sell his appreciated puts, and use those proceeds to buy more TSLA. He has those options because he's hedged.