The selling of calls is a difficult matter,

It isn't just one of your holiday games;

You may think at first I'm as mad as a hatter

When I say, shorting stock can hedge more of your gains.

Okay, so I totally butchered T.S. Eliot's poem, The Naming of Cats, but it's true - the selling of calls is a difficult matter. What do you do when implied volatility is really low? Is it worth selling calls in that kind of environment? Probably not.

But you could hedge your gains in a different manner, get a lot more downside protection, and have more control over the rate at which your position rises and falls. And that's by shorting stock, not calls, against a long call option.

***

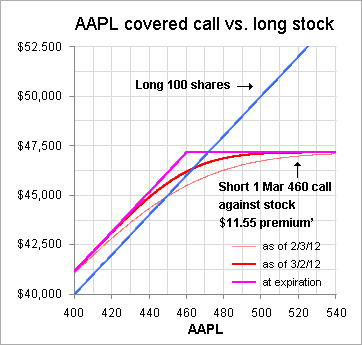

Let's use Apple (NASDAQ:AAPL) as an example. Roll the tape back to February 3. The stock opened at $457.30, peaked at $460, then closed at $459.68.

You're tempted to sell a covered call against your stock, perhaps a March 460 call? You'd only get $11.55. You sell a call partly for its so-called "downside protection," but what kind of protection is that? If volatility spikes and the stock falls $15, that short call might still actually go up!

Besides, on Friday, February 10, your stock is up $33.74. Unfortunately, buying back the call you sold for $11.55 would set you back $38.80. So you've given up a lot of upside as things stand. At least, so far.

Just to review, here's a chart showing how a covered call position works - selling one call against 100 shares of stock - assuming volatility at around 27%.

You get to keep the $11.55 premium for the call, which helps a little on the downside, but your upside gains are capped.

Selling calls is complicated…

When you sell one