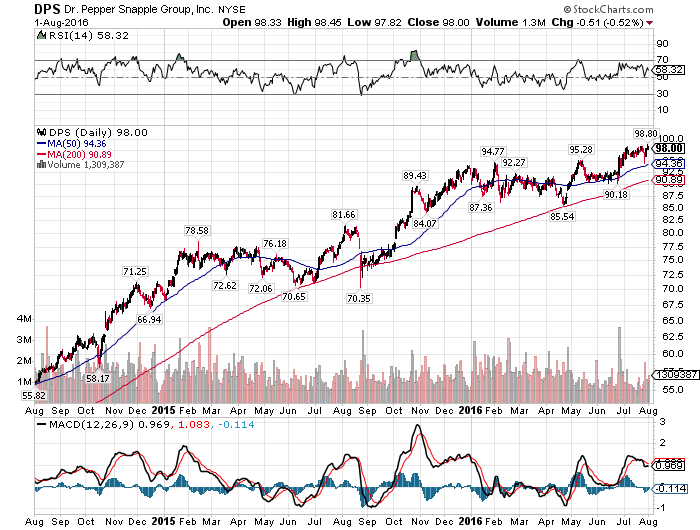

Dr. Pepper Snapple (DPS) has been one of the best performing stocks in the entire market for the past couple of years. The chart is beautiful as shares have moved from bottom left to upper right with very little downward action. And while DPS has shown more growth potential than KO, for instance, is it enough? DPS' Q2 report was fine but didn't exactly provide torrid growth so what is going to make this stock continue to go up?

DPS saw total sales up 2% during the quarter as price and mix contributed as well as a 1% gain in volume. This has been a problem for DPS for some time as it and others in the carbonated beverages space face declining demand over time for traditional soft drinks. DPS has the Snapple business that provides some much needed diversification but still, volume is always going to be an issue. And a 1% gain in volume is nothing to get excited about and it certainly changes the valuation picture because you know there will always be a lid on sales growth.

In addition, the global nature of DPS' business saw two percent of sales removed by forex translation. This is a problem for virtually any multinational as the dollar has been mostly holding up against some rapidly depreciating major currencies around the globe. The dollar is always going to be a problem for DPS and with the Fed being the only major central bank in the world that is even talking about tightening, I suspect this will get worse before it gets better. DPS' dollar exposure is by no means unmanageable but every little bit counts when you're talking about volume being up 1%.

To its credit, DPS continues to find ways to boost margins as its segment operating profit rose