Source: Investor presentation, page 7

Here we go again

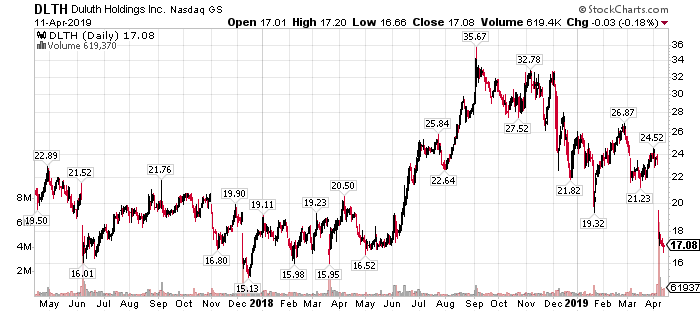

Shares of Duluth Holdings (NASDAQ:DLTH) have been on a wild ride in the past couple of years. After spending a lot of time bouncing between the high-teens and low-20s, Duluth rocketed to nearly $36 very briefly last summer. However, things haven’t been so rosy since then.

I’ve been a Duluth bull and bear at different times, depending upon the valuation at any given point. The way the stock has moved has created situations of great overvaluation and strong buying opportunities alike. Today, after the selloff from the Q4 earnings report, Duluth looks like it is a buy once more.

An imperfect Q4

Duluth’s Q4 report certainly wasn’t perfect, but investors that have sold the stock, in my view, are missing the point on long-term growth potential. That potential has been there all along, but the stock has, at times, built in some of that growth well in front of when it would actually occur. However, with the stock very near the lowest levels it has seen in the past two years, I think there is some value in Duluth despite relatively weak guidance for this year.

Total sales in 2018 rose 20.5% to $568 million, including a $7.7 million increase from an additional operating week. Duluth continues to not only grow its core direct-to-consumer, or DTC, channel, but open new stores as well. The company boosted its physical retail footprint by 50% in 2018, adding 15 stores. Duluth reckons it will open another 15 stores this year, and in fact, just opened its 50th store in support of that goal. Duluth continues to see mid-single-digit gains in the DTC channel, while retail sales grow at ~40% rates, thanks to new store openings. Importantly, Duluth is seeing growth from both its men’s and women’s lines, the latter of which is