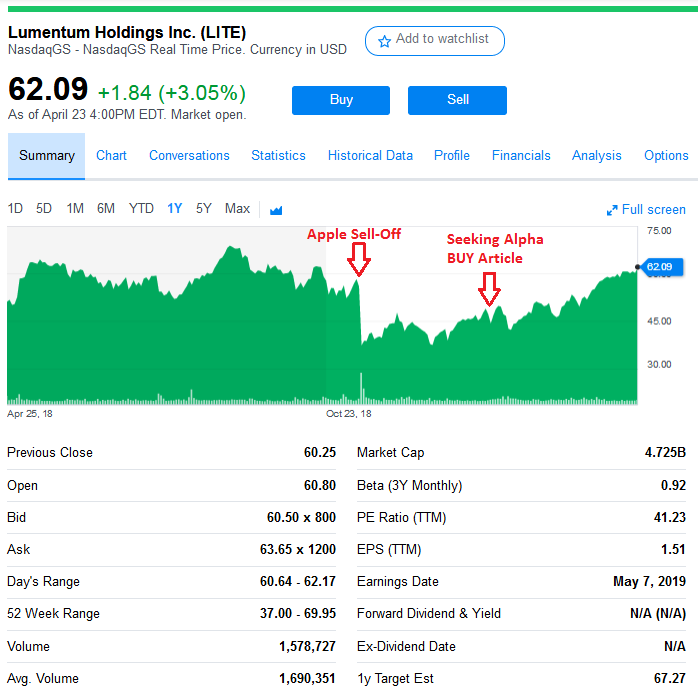

Back in January, I wrote a Seeking Alpha article recommending Lumentum (NASDAQ:LITE) after the stock had sold-off as a result of concerns that orders from its #1 customer - Apple (AAPL) - would be drastically lower. I suggested the loss in Apple-related revenue might easily be recovered by 3D sensing applications in the larger Android market as well as emerging opportunities in 5G infrastructure. The stock was $44 and change at the time and my prediction was that LITE could trade back up to $60 over the next 12 months. The stock closed at $62.09 yesterday, for a less than three-month return of ~40%:

Source: Yahoo Finance

The stock's move just seemed "too far, too fast", so I sold half my shares.

But it could be a big mistake. I still like the company because the future looks bright. LITE recently closed its sale of datacom transceiver product lines to Cambridge Industries Group ("CIG") in order to focus on photonic chips. The transceiver product lines acquired by CIG were previously developed and manufactured by Oclaro Japan, which LITE acquired in December of last year. In connection with the deal, Lumentum and CIG entered into a long-term supply agreement for Lumentum's photonic chips. Basically, LITE sold some non-core assets and added another customer to its core photonic products.

Those who view LITE as an Apple-centric company may be missing the mark. While the impact of slower 3D sensing orders from Apple was certainly tangible (Apple was 30% of revenue in FY18), investors may have underestimated Lumentum's ability to sell its 3D sensing products into the much larger Android market. The transition to mid-range phones (i.e. Android) is actually great for LITE as it is a much bigger global market space than iOS, so volumes are sure to go up (it will be an estimated $2 billion consumer mobile market by 2020/2021). And for