![]()

Wabash National (NYSE:WNC) is a manufacturer of trailers, vans, flatbeds, refrigerated trucks, and even pharmaceutical equipment. The company has been seen as a cyclical play on the economy due to the nature of what it produces. Generally, when companies are selling less the need for transportation mechanisms declines. However, the economy is doing well and the shares trade as if there is a risk to the business model and earnings. The stock offers an attractive valuation and perhaps have more upside potential than downside risk. For the investor who can wait for consistent performance to result in a higher valuation, Wabash National is worth a look.

Performance

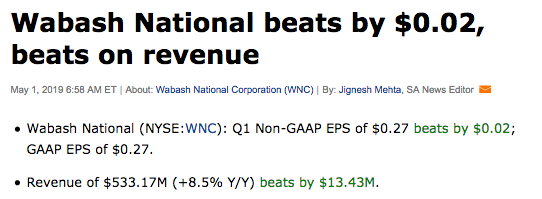

Wabash National reported first quarter earnings recently that beat on both the top and bottom lines.

Source: Seeking Alpha

Revenues continued to grow despite belief that the economy might have been slowing.

In the company's commercial trailer products segment, revenue increase just over 4%.

Source: Earnings Slides

The company did, however, see margins decline due to higher material costs and some supplier disruptions. Hopefully going forward the company can pass along higher costs through higher prices. This can happen easily during a strong economy, especially when offering a premium product.

The company's diversified products group saw revenue rise at a similar rate, but also saw margin expansion.

Source: Earnings Slides

The company was helped by the mix of sales and pricing initiatives taken the year before.

Lastly, the strongest growth came in final mile products.

Source: Earnings Slides

This is probably due to the strong demand for delivery of products from purchases made online. Due to the increased demand for package volume and shipments, companies are in need of additions to their fleet. Wabash produces an excellent product that can help transporters increase efficiency and at a reasonable cost.

The company had