Most investors salivate when their stock gets an acquisition offer because it generally means the prospective buyer is willing to pay more than the current market price of the equity of the targeted firm. However, current valuations in the utility segment implies the majority of stocks are trading at a premium to the usual premium in a merger dance. It could be said buying at a premium to a merger premium is not much of a safe haven.

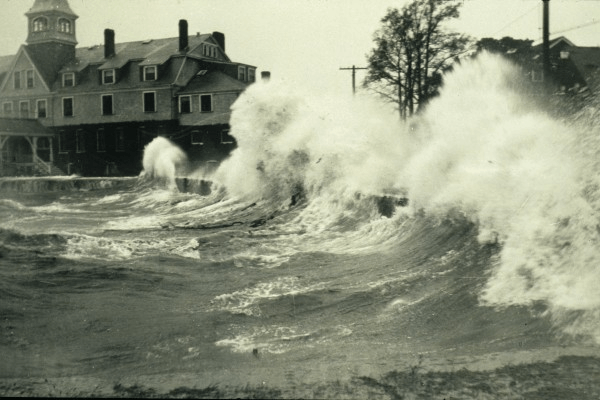

In the No-Name hurricane of Sept 1938, there were no safe havens as the storm crossed Cape Cod, Massachusetts, leaving 250 dead in its wake

Historically, utility stocks have been considered a “safe” sector during times of market upheaval. Their steady, regulated earnings and higher dividend income can provide less volatility than the overall market, especially when compared to higher valued stocks, such as technology. Usually, utilities offer lower beta values, such as the 0.35 5-yr monthly beta of the S&P Utility ETF (XLU). However, much like the Sept 1938 No-Name hurricane that devastated Cape Cod and New England, sometimes it is difficult to find safe sanctuaries in the middle of a powerful storm, and with the current volatility of 1,000 point swings on the Dow, we certainly are in the middle of a financial cyclone.

The utility sector has been in consolidation mode for over 25 years. Since 1995, the electric utility sector has experienced over 145 acquisition announcements among Edison Electric Institute EEI members and roughly 120 have completed deals. The electric and gas utility industries remain fragmented, and the financial force driving utility consolidation continues, including rising capital needs, stagnant demand growth, and economies of scale. There is the added recent incentive to acquire “green” assets. The regulated relationship between the companies and regulators assures investment in prudent utility infrastructure is recognized and allows for a fair return. As a result, utility