Recent moves by Baytex Energy (NYSE:BTE) may have shored up the balance sheet and sufficiently increased cash flow. Baytex Energy began as a heavy oil producer. Up until 2014 that was a decent proposition. But just before the big price decline, management acquired the Eagle Ford properties and debt ballooned. The recent acquisition of Raging River (RRENF) should have increased cash flow enough to ensure a comfortable survival.

Source: Baytex Energy March 2020 Investor Presentation

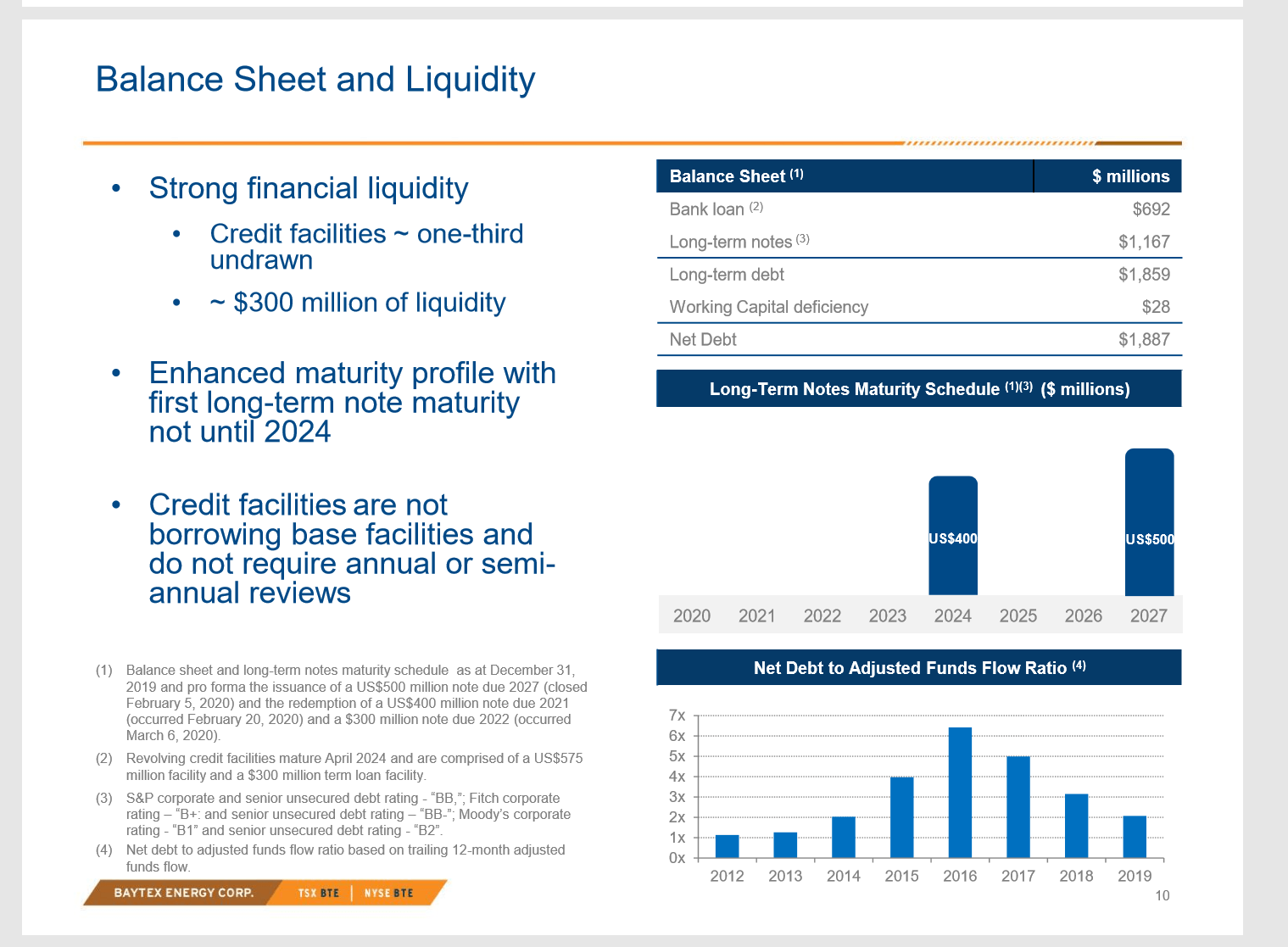

As shown above, once oil prices declined, the key net debt ratio climbed to unacceptable levels by 2016. In fact, even after oil prices recovered somewhat, the ratio remained too high for most lending guidelines. That "forced" a merger with low debt Raging River. That merger lowered the debt ratios while adding considerable light oil production.

Current oil prices are unlikely to be sustained for more than a few months. However, while the current challenges remain, much of the industry will not make much cash flow if any from current oil prices. Most lenders do not value income from hedges much.

Therefore, the second quarter is likely to have the low point of the current industry cycle. Depending on production and supply conditions, the recovery should begin by the third quarter. If that is the case, this company could be in a good position to take advantage of the current situation.

Before the latest crisis began, the debt ratios were in decent shape in fiscal year 2019. The banks stood behind this company back in 2015 when things got really bad from the soaring debt ratio. This time around, cash flow will begin at lower price levels than it did back then.

Management noted that this company does not undergo periodic reviews for the bank line as many do in the industry. There is one covenant. The

I analyze oil and gas companies like Baytex Energy and related companies in my service, Oil & Gas Value Research, where I look for undervalued names in the oil and gas space. I break down everything you need to know about these companies - the balance sheet, competitive position, and development prospects. This article is an example of what I do. But for Oil & Gas Value Research members, they get it first and they get analysis on some companies that is not published on the free site. Interested? Sign up here for a free two-week trial.