The advent of COVID-19 may have changed the way we work and the way we play forever. Investing now requires us to imagine what a post-pandemic world would look like. I have long believed that the most likely outcome is the gradual and slow re-opening of the economy with social distancing to persist for months on end. Given this situation, certain business models may not survive or would need to be altered in order to operate post-pandemic. Planet Fitness (NYSE:PLNT) is one such company whose entire business model may need to be re-evaluated for a post-COVID-19 world.

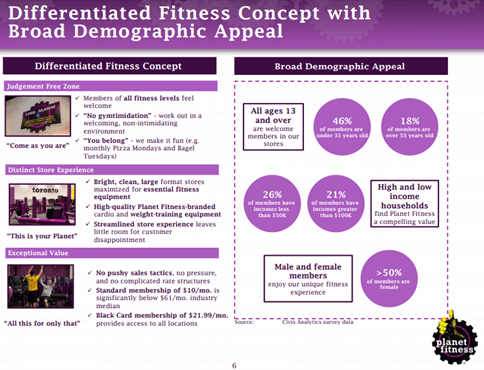

Just a brief background on the company; Planet Fitness is a franchisor and operator of a chain of gyms predominantly in the US. Planet Fitness rose to prominence by being more inclusive and offering a non-intimidating/judgment-free environment at a much cheaper price. Planet Fitness memberships are about $10-20 while the industry median according to the company's 10-K is about $71.

The company targets the casual gym users and no fitness buff as these people may find traditional gyms intimidating and expensive. The equipment in Planet Fitness' gyms is of high quality and the company has limited the number of staff available on site. The square space tends to be smaller than its competitors' and is lacking non-essential amenities like pools, daycare or juice bars, etc. In other words, it is a low-cost and high-volume business model.

COVID-19 is a disruption to the business model

As I’ve discussed in my article on Peloton (PTON), social distancing is a large hindrance to the traditional gym model. This is because large groups of people who are all sweating bodily fluids in a confined space is a potential hotbed for viruses. In order to reopen, gyms may have to change