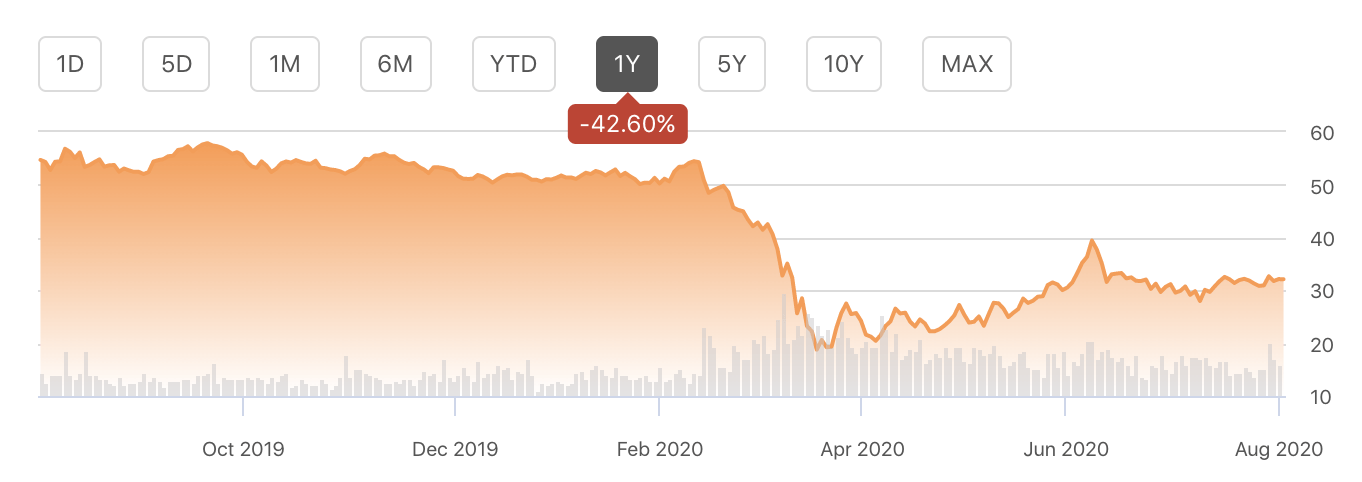

It has been a terrible year for American International Group (NYSE:AIG) shareholders with the stock losing over 40% of its value. Indeed, in the low $30s, shares are trading at levels seen in 2012. The stock offers a steady dividend, which due to the share price decline, now yields nearly 4%. It also trades at a substantial discount to book value, but earnings power continues to be poor, leaving investors with a quandary: stay and hope for a turnaround or cut losses. I recommend holding for now while using rallies to sell.

(Source: Seeking Alpha)

Q2 Results Were Mixed

In the company’s second quarter (financials available here), AIG earned $0.66, $0.13 ahead of consensus. On a GAAP basis, it was very messy, and the company lost $9.15 as it took a loss on its sale of Fortitude Re.

AIG sold its 76.6% stake in Fortitude for $2.2 billion. By disposing of this entity, AIG’s balance sheet has less risk to “long-tail runoff liabilities.” The company took a $6.7 billion after-tax loss from this sale, which led to a $4.3 billion reduction in AIG’s shareholders' equity, which excludes accumulated other comprehensive income (AOCI largely arises from when assets that are being held to maturity trade above par). Fortitude reinsures the majority of AIG’s legacy portfolio. So while AIG held onto 76% of Fortitude, it was essentially reinsuring itself. By selling out to Carlyle, AIG has reduced its exposure to its legacy insurance portfolio, though at a steep cost.

Since taking over as CEO in 2017, Brian Duperreault has focused relentlessly on trying to improve the quality of underwriting, which has plagued the general insurance unit ever since the financial crisis. This sale of Fortitude is an effort to close the chapter on that era. However, transitioning into the next era is proving to be anything but