Focus of Article:

The focus of PART 1 of this article is to analyze Annaly Capital Management Inc.’s (NYSE:NLY) recent results and compare several of the company’s metrics to twenty mortgage real estate investment trust (mREIT) peers. This analysis will show past and current data with supporting documentation within three tables. Table 1 will compare NLY’s mortgage-backed securities (“MBS”)/investment composition, recent leverage, hedging coverage ratio, BV, and economic return (loss) to the twenty mREIT peers. Table 1 will also provide a premium (discount) to estimated CURRENT BV analysis using stock prices as of 9/11/2020. Table 2 will show a quarterly compositional analysis of NLY’s agency MBS portfolio while Table 3 will show the company’s recent hedging coverage ratio over the past two quarters (only contributor/team to provide detailed hedging metrics).

I am writing this two-part article due to the continued requests that such an analysis be specifically performed on NLY versus its mREIT peers at periodic intervals. This article also discusses the importance of understanding the composition of NLY’s MBS/investment and derivatives portfolios when it comes to projecting the company’s future quarterly results as interest rates/yields fluctuate. Understanding the characteristics of a company’s MBS/investment and derivatives portfolios can shed some light on which companies are overvalued or undervalued strictly per a “numbers” analysis. This is not the only data that should be examined to initiate a position within a particular stock/sector. However, I believe this analysis is a good “starting-point” to begin a discussion on the topic.

At the end of this article, there will be a conclusion regarding the following comparisons between NLY and the twenty mREIT peers: 1) leverage as of 6/30/2020; 2) hedging coverage ratio as of 6/30/2020; 3) trailing twelve-month economic return (loss); and 4) premium (discount) to my estimated CURRENT BV (BV as of 9/11/2020). My BUY, SELL, or HOLD recommendation and updated price target for NLY will be in the “Conclusions Drawn” section of this article. This includes providing a list of the mREIT stocks I currently believe are undervalued (a buy recommendation), overvalued (a sell recommendation), or appropriately valued (a hold recommendation).

Overview of Several Classifications within the mREIT Sector:

I believe there are several different classifications when it comes to mREIT companies. For purposes of this article, I am focusing on four. It should be noted in light of several prior acquisitions and certain changes in overall investment strategies, some mREIT companies have minor portfolios outside each entity’s main concentration. However, I have continued to group certain mREIT companies in each entity’s main classification for purposes of this article. Some market participants (and even some mREIT companies) have different classifications when compared to Table 1. Some market participants/companies base classifications on the percentage of capital deployed in each entity’s investment portfolio. However, my preference is to base a company’s classification on the monetary “fair market value” (“FMV”) of each underlying portfolio (which, for a fact, is what drives valuation fluctuations). In my professional opinion, there is no “uniform” methodology when it comes to classifying mREIT companies but more of an underlying preference. Readers should understand this as the analysis is presented below.

First, there are mREIT companies who earn a majority of income from investing in fixed-rate agency MBS holdings. These investments consist of commercial/residential MBS, collateralized mortgage obligations (“CMO”), and agency debentures for which the principal and interest payments are guaranteed by government-sponsored enterprises/entities (“GSE”). In this current environment, this is extremely important to understand (especially when markets recently incorrectly priced in this notion). Since these investments typically have higher durations versus most other investments within the broader mREIT sector, companies within this classification typically utilize higher hedging coverage ratios in times of rising mortgage interest rates/U.S. Treasury yields (or a projected rise over the foreseeable future). NLY, AGNC Investment Corp. (AGNC), Arlington Asset Investment Corp. (AI), ARMOUR Residential REIT Inc. (ARR), Cherry Hill Mortgage Investment Corp. (CHMI), Dynex Capital Inc. (DX), Orchid Island Capital Inc. (ORC), and Two Harbors Investment Corp. (TWO) are currently classified as a fixed-rate agency mREIT.

Second, there are mREIT companies who earn a majority of income from investing in variable-rate agency MBS holdings. These investments generally are commercial/residential MBS for which the principal and interest payments are also guaranteed by a GSE. More specifically, variable-rate MBS generally consist of adjustable-rate mortgages(“ARM”) that have varying interest rate reset periods. ARM holdings are usually classified together based on each security’s average number of months to coupon reset. This is also known as the security’s “months-to-roll”. This is a typical indicator of asset duration which helps identify each security’s price sensitivity to interest rate movements. If a security’s months-to-roll is high, then this type of investment can also be described as a hybrid ARM holding. Capstead Mortgage Corp. (CMO) is currently classified as a variable-rate agency mREIT.

Third, there are mREIT companies who earn varying portions of income from investing in agency MBS holdings, non-agency MBS holdings, other securitizations, and non-securitized mortgage-related debt investments. This type of company is known as a “hybrid” mREIT. In regards to non-agency MBS, this includes (but is not limited to) Alt-A, prime, subprime, and re/non-performing loans where the principle and interest are not guaranteed by a GSE. Since there is no “government guarantee” on the principle or interest payments of non-agency MBS, coupons are generally higher when compared to agency MBS of a similar maturity. However, borrowing costs (including repurchase agreements) for these specific investments are also higher (no government guarantee; credit risk). Due to the subtle yet identifiable differences between agency and non-agency MBS, I like to differentiate between an agency and a hybrid mREIT company. Since there is credit risk when it comes to non-agency MBS, leverage ratios are typically lower when investing in these securitizations when compared to agency MBS (even when credit risk remains low). That said, the recent historical volatility within this specific sector has temporarily caused most mREIT peers to deleverage which has caused some temporary “disruptions” when it comes to leverage ratios. Over time, this should return to more historical averages (will take time though). Anworth Mortgage Asset Corp. (ANH), Chimera Investment Corp. (CIM), Ellington Financial Inc. (EFC) (converted to a REIT in 2019); Invesco Mortgage Capital Inc. (IVR), MFA Financial Inc. (MFA), AG Mortgage Investment Trust Inc. (MITT), and Western Asset Mortgage Capital Corp. (WMC) are currently classified as a hybrid mREIT.

Finally, there are mREIT companies that invest in (but are not limited to) a combination of agency MBS, non-agency MBS, other mortgage-related investments, non-securitized debt investments (including multifamily and commercial loans), and mortgage servicing rights (“MSR”). I believe Blackstone Mortgage Trust, Inc. (BXMT), Granite Point Mortgage Trust Inc. (GPMT), New Residential Investment Corp. (NRZ), New York Mortgage Trust Inc. (NYMT), and PennyMac Mortgage Investment Trust (PMT) should currently be classified as a “multipurpose” mREIT. Since BXMT and GPMT had 99% and 98.5% of its investment portfolio in variable-rate debt as of 6/30/2020, respectively, these companies currently do not need to utilize a high hedging coverage ratio (some could even argue to not have derivative instruments in place; if anything perhaps “contra” hedges to counter a drop in rates/yields). The same can be said about NRZ (to a lesser degree) who currently has a majority of the company’s investment portfolio in MSR and MSR-related investments which act as an “indirect” hedge (the same can be said regarding interest only [IO] securities). Indirect hedges are not calculated within each company’s hedging coverage ratio (not the main purpose of these investments). As I have pointed out in the past, these investments actually benefit, from a valuation standpoint, in a rising interest rate environment as prepayment risk (and in a majority of scenarios credit risk) decreases while there is an increase in projected future discounted cash flows (and vice versa). Now let us start the comparative analysis between NLY and the twenty mREIT peers.

Leverage, Hedging Coverage Ratio, BV, Economic Return (Loss), and Premium (Discount) to Estimated Current BV Analysis - Overview:

Let us start this analysis by first getting accustomed to the information provided in Table 1 below. This will be beneficial when explaining how NLY compares to the twenty mREIT peers in regards to the metrics stated earlier.

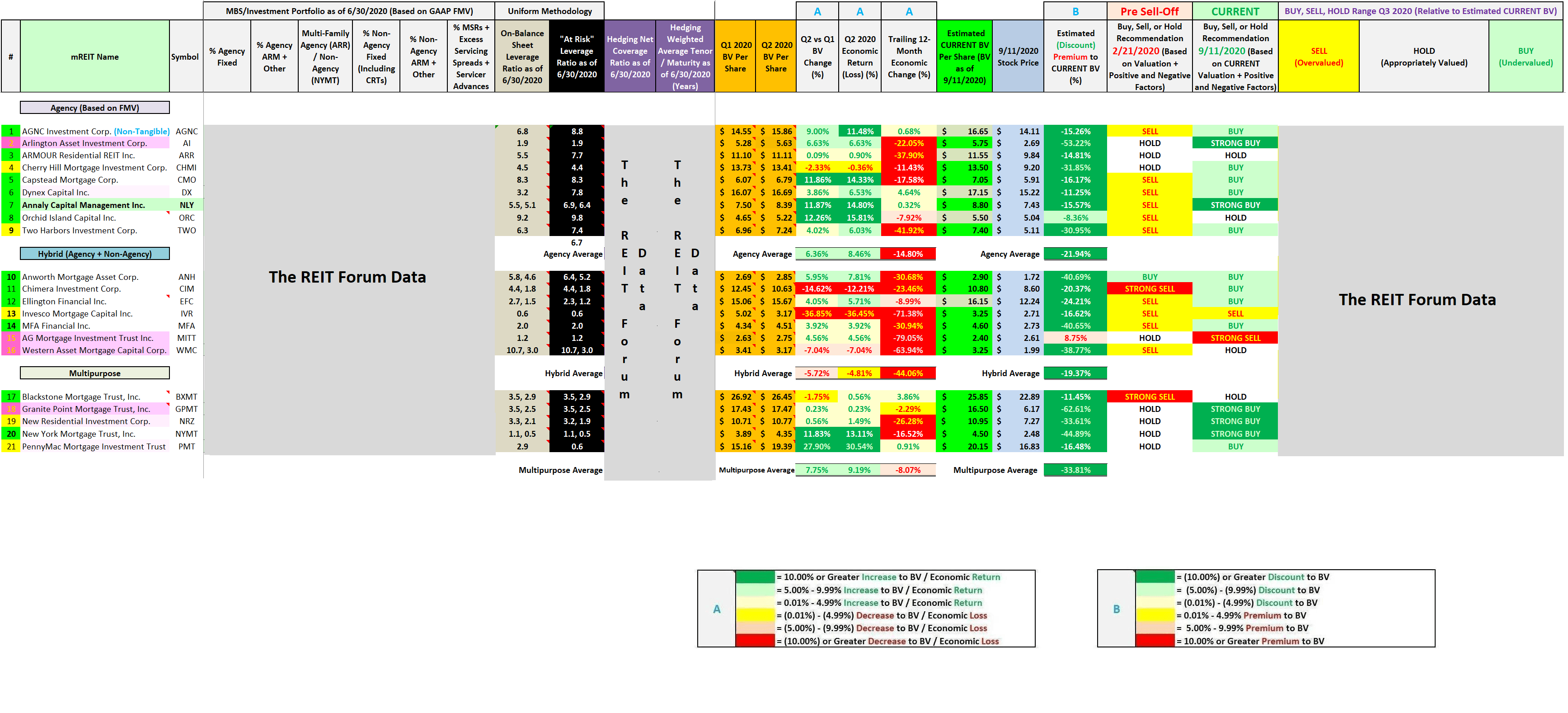

Table 1 – Leverage, Hedging Coverage Ratio, BV, Economic Return (Loss), and Premium (Discount) to Estimated Current BV Analysis

(Source: Table created by me, obtaining historical stock prices from NASDAQ and each company’s 3/31/2020 and 6/30/2020 BV per share figures from the SEC’s EDGAR Database)

(Source: Table created by me, obtaining historical stock prices from NASDAQ and each company’s 3/31/2020 and 6/30/2020 BV per share figures from the SEC’s EDGAR Database)

Table 1 above provides the following information on NLY and the twenty mREIT peers (see each corresponding column): 1) generalized MBS/investment portfolio composition as of 6/30/2020 (metric solely for the REIT Forum subscribers); 2) on-balance sheet leverage ratio as of 6/30/2020; 3) at-risk (total) leverage ratio as of 6/30/2020; 4) hedging coverage ratio as of 6/30/2020 (metric solely for the REIT Forum subscribers); 5) hedging weighted average tenor/maturity (metric solely for the REIT Forum subscribers); 6) BV per share at the end of the first quarter of 2020; 7) BV per share at the end of the second quarter of 2020; 8) BV per share change during the second quarter of 2020 (percentage); 9) economic return (loss) (change in BV and dividends accrued for/paid) during the second quarter of 2020 (percentage); 10) economic return (loss) during the trailing twelve-months (percentage); 11) my estimated CURRENT BV per share (BV as of 9/11/2020); 12) stock price as of 9/11/2020; 13) 9/11/2020 premium (discount) to my estimated CURRENT BV (percentage); 14) 2/21/2020 BUY, SELL, or HOLD recommendation (pre market sell-off due to coronavirus [COVID-19]); 15) 9/11/2020 BUY, SELL, or HOLD recommendation; and 16) BUY, SELL, and HOLD recommendation range, relative to my estimated CURRENT BV (metric solely for the REIT Forum subscribers).

Analysis of NLY:

As of 6/30/2020 NLY’s investment portfolio consisted of 83% and 1% fixed- and variable-rate agency MBS holdings, respectively (based on FMV). When compared to 3/31/2020, NLY’s percentage of fixed- and variable-rate agency MBS remained unchanged. NLY also maintained a 1% multifamily agency MBS sub-portfolio. NLY continued to invest in non-agency MBS and non-MBS holdings which accounted for 15% of the company’s investment portfolio balance as of 6/30/2020. This included NLY’s investments in commercial debt/real estate, preferred equity, corporate debt, middle market (“MM”) lending, seniors housing, and MSRs. This percentage was also unchanged when compared to the end of the prior quarter.

Using Table 1 above as a reference, when excluding borrowings collateralized by assets held in “securitization trusts” (non-recourse debt), NLY had an on-balance sheet leverage ratio of 5.1x while the company’s at-risk (total) leverage ratio, when including its off-balance sheet net long “to-be-announced” (“TBA”) MBS position, was 6.4x as of 6/30/2020. NLY had an on-balance sheet and at-risk (total) leverage ratio of 5.8x and 6.8x as of 3/31/2020, respectively. As such, NLY modestly lowered the company’s on-balance sheet leverage while slightly lowering its at-risk (total) leverage during the second quarter of 2020.

As of 6/30/2020, NLY had the third lowest at-risk (total) leverage ratio when compared to the eight other agency mREIT peers within this analysis. Due to the notable impacts from the COVID-19 pandemic to the mREIT sector when it comes to the quick “spike” in leverage and liquidity risk (rising credit risk more of a longer-term impact regarding all non-agency investments), outside a couple multipurpose mREIT peers who mainly invest in commercial whole loans (BXMT and GPMT), all sector peers I currently cover had various strategies at play when it comes to investment portfolio composition and risk management strategies. Even when several mREIT peers had very similar MBS/mortgage-related investments, recent strategies notably differed from company-to-company. Directly dependent on the amount/percentage of margins calls on certain outstanding borrowings (and the underlying investments pledged as collateral) and derivative instruments, most mREIT peers had a notable change in recent leverage ratios. Due to NLY’s overall size and asset composition, this company was not “forced” to de-lever to the same extent as some of the smaller-capitalized agency mREIT peers (more “cushion” when it came to its existing capital base).

Previously, management implied NLY had a fairly “defensive posture” in regards to leverage during 2017-2018 due to the risk of widening spreads/lower MBS prices as the Federal Open Market Committee (“FOMC”) dictated future monetary policy (in particular, the Federal [“Fed”] Funds Rate and the Fed Reserve’s non-reinvestment of U.S. Treasuries and agency MBS). However, with the FOMC’s more “dovish” rhetoric in 2019 regarding U.S. monetary policy over the foreseeable future, I previously correctly anticipated NLY would begin to increase leverage which has been consistent with recent agency mREIT sector trends as net spreads have narrowed. This benefited most mREIT peers during the fourth quarter of 2019.However, this led to more severe BV declines during the first quarter of 2020 (especially March).This was partially offset during the second quarter of 2020 as MBS pricing/valuations (and most other mortgage-related investments outside some CMBS and commercial whole loans) rebounded.

NLY had a BV of $7.50 per common share at the end of the first quarter of 2020. NLY had a BV of $8.39 per common share at the end of the second quarter of 2020. This calculates to a quarterly BV increase of $0.89 per common share or 11.87%. When including NLY’s quarterly dividend of $0.22 per common share, the company had an economic return of $1.11 per common share or 14.80% for the second quarter of 2020. Similar to most agency mREIT peers, this was a very strong quarterly performance and helped erase a notable portion of the extremely severe decrease in BV during the first quarter of 2020.

As disclosed to readers in prior mREIT articles (as it was occurring during the quarter), a notably more positive relationship between agency MBS/mortgage-related investment pricing and derivative instrument valuations quickly developed during April 2020 when compared to the first quarter of 2020. This ultimately led to nearly all agency mREIT peers to report an increase in BV as of 6/30/2020 when compared to 3/31/2020. In other words, basically most agency/non-agency/mortgage-related investment MBS net valuation gains slightly-notably “trumped” derivative/MSR net valuation losses. I correctly projected most agency mREIT companies would experience a modest-notable BV increase within the following AGNC BV projection article:

Within that article, I projected NLY would report (prior to any other sector peer reporting) a BV as of 6/30/2020 of $8.05 per share with a range of $7.70-$8.40 per share. In comparison, NLY reported a BV as of 6/30/2020 of $8.39 per share which was basically at the top end of my projected range. I classify this as a modest (at or greater than 2.5 % but less than 5% outperformance).

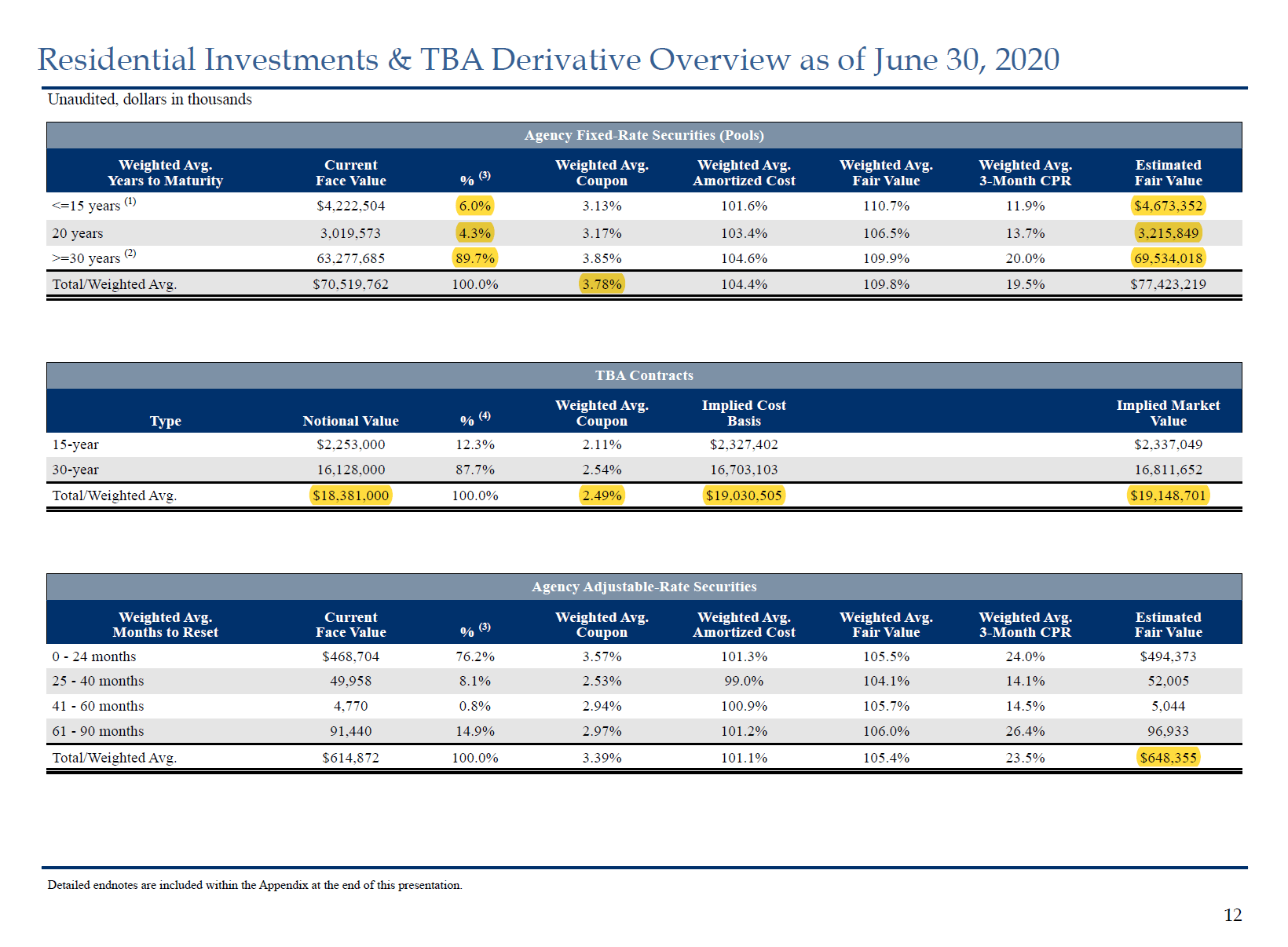

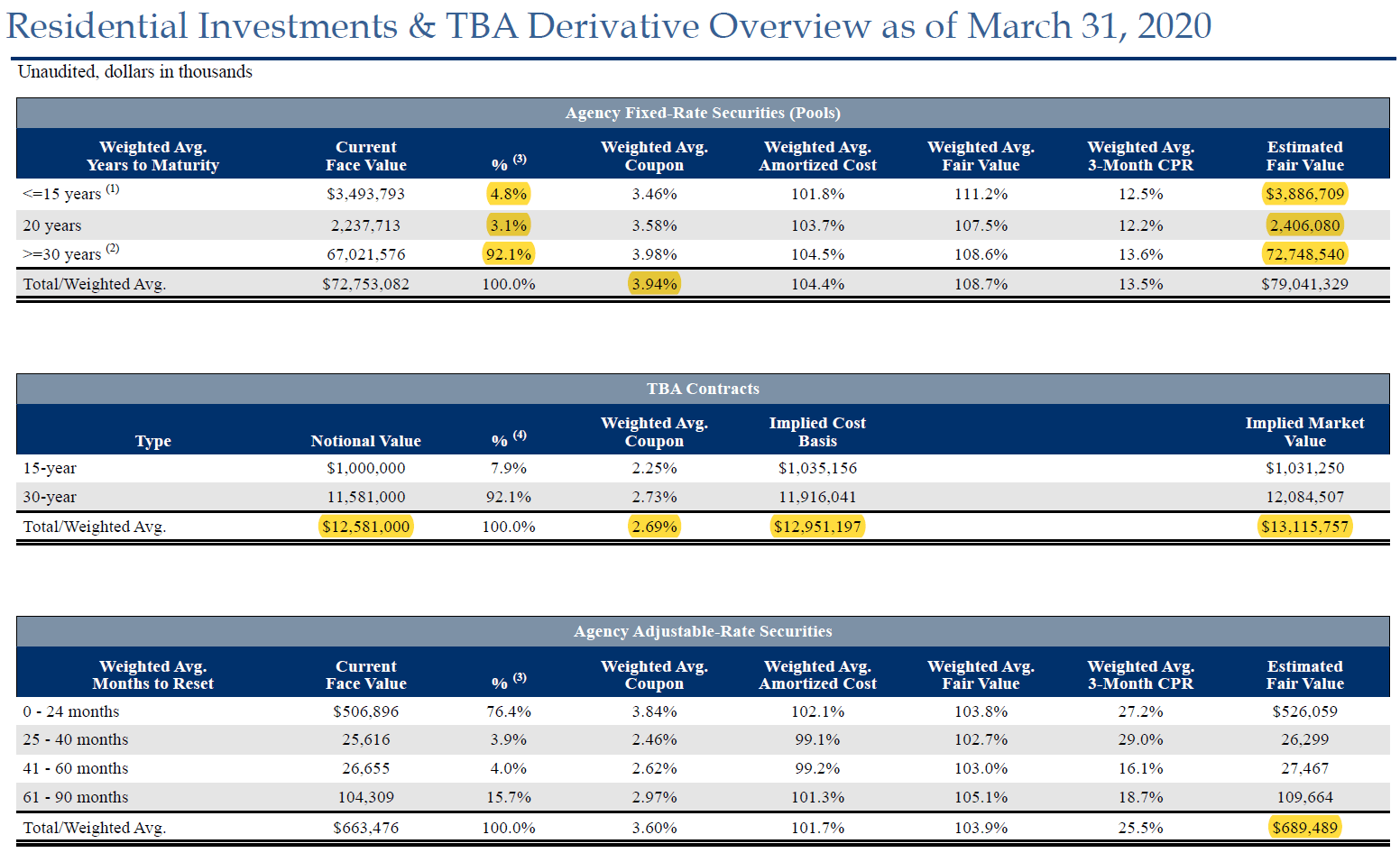

Let us now discuss NLY’s MBS and derivatives portfolios to spot certain characteristics which will impact future results. Table 2 below provides NLY’s proportion of fixed- and variable-rate agency MBS holdings as of 6/30/2020 versus 3/31/2020 (the vast majority of the company’s investment portfolio).

Table 2 – NLY Agency MBS Portfolio Composition (6/30/2020 Versus 3/31/2020)

(Source: Table obtained [with added highlights] from NLY’s quarterly shareholder presentation for first and second quarters of 2020)

Using Table 2 above as a reference, NLY continued to maintain a portfolio heavily invested in 30-year fixed-rate agency MBS holdings during the second quarter of 2020. NLY’s proportion of 15-year fixed-rate agency MBS holdings slightly increased from 4.8% to 6.0% during the quarter (based on par/face value). NLY’s proportion of 20-year fixed-rate agency MBS holdings slightly increased from 3.1% to 4.3%. As such, NLY’s proportion of 30-year fixed-rate agency MBS slightly decreased from 92.1% to 89.7%. When compared to fixed-rate agency mREIT peers like AGNC and ARR, NLY continued to have a higher proportion of 30-year fixed-rate agency MBS holdings during the second quarter of 2020.

NLY’s on-balance sheet fixed-rate agency MBS holdings had a weighted average coupon (“WAC”) of 3.78% as of 6/30/2020 which was a (16) basis points (“bps”) decrease when compared to 3/31/2020. This provides direct evidence NLY sold-off some higher coupon fixed-rate agency MBS during the quarter. Continuing a trend from the past two quarters, NLY’s TBA MBS position had a notably lower WAC of just 2.49% which was consistent with a few other fixed-rate agency mREIT peers regarding forward/generic MBS strategies (lower coupons generally equate to less prepayment risk). In addition, NLY’s weighted average three-month conditional prepayment rate (“CPR”) increased from 13.5% to 19.5% which was also a fairly consistent trend across the sector as mortgage interest rates/long-term U.S. Treasury yields decreased during the first and second quarters of 2020 (a bit of a “delayed” impact to this metric; including seasonal trends). Let us now move on to NLY’s derivatives portfolio.

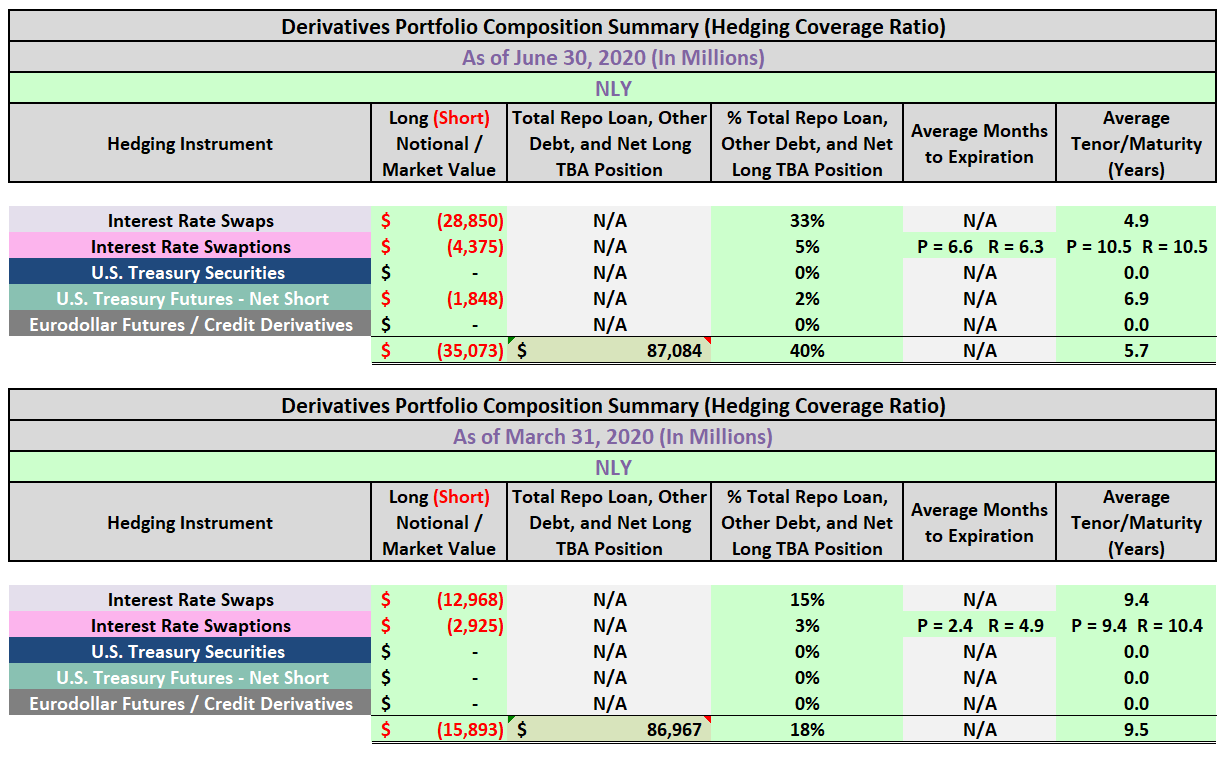

While management has continued to diversify the company’s investment portfolio into less interest rate sensitive holdings (lower durations), a majority of the company’s investment portfolio (from a valuation standpoint) was still in fixed-rate agency MBS. Along with the “plummet” in the Fed Funds Rate to near 0% in March 2020 (which also caused a proportionately large decrease to the London Interbank Offered Rate (“LIBOR”) across all tenors/maturities and all other applicable short-term funding/interest rates) and the subsequent margin call in certain derivative instruments, NLY notably reduced the company’s hedging coverage ratio during the first quarter of 2020. As NLY entered into new interest rate swap contracts during the second quarter of 2020 (at notably more attractive terms), management “rebuilt” the company’s derivatives portfolio. To highlight the recent activity within NLY’s derivatives portfolio, Table 3 is presented below.

Table 3 – NLY Hedging Coverage Ratio (6/30/2020 Versus 3/31/2020)

(Source: Table created by me, partially using NLY data obtained from the SEC’s EDGAR Database [link provided below Table 1])

Using Table 3 above as a reference, NLY had a net (short) interest rate swaps and swaptions position of ($13.0) and ($2.9) billion as of 3/31/2020, respectively (based on notional value). However, NLY completely sold/exited the company’s net long U.S. Treasury, net (short) U.S. Treasury futures, and net (short) credit derivatives positions during the quarter. When calculated, NLY had a hedging coverage ratio of only 18% as of 3/31/2020. When compared to the seven other fixed-rate agency mREIT peers within this analysis, this was notably below the average hedging coverage ratio of 50% as of 3/31/2020.

NLY had a net (short) interest rate swaps and swaptions position of ($28.9) and ($4.4) billion as of 6/30/2020, respectively. NLY also had a net (short) U.S. Treasury futures position of ($1.8) billion. When calculated, NLY’s hedging coverage ratio increased to 40% as of 6/30/2020. This now matched the agency mREIT average hedging coverage ratio of 40% as of 6/30/2020.

Once again using Table 1 above as a reference, as of 9/11/2020 NLY’s stock price traded at $7.43 per share. When calculated, NLY’s stock price was trading at a (15.57%) discount to my estimated CURRENT BV (BV as of 9/11/2020). Simply put, NLY’s stock price traded at a notable (at or greater than a 10%) discount to my estimated CURRENT BV and at a slightly smaller discount when compared to the average of other agency mREIT peers within Table 1. When tracking historical trends, NLY typically trades at a higher valuation (less of a discount/more of a premium) to the company’s agency mREIT peers. I continue to believe NLY “deserves” to trade at modestly higher valuation (which has been explained in various mREIT sector articles and through the REIT Forum discussions). As such, as stated later in the article, I currently believe NLY is very attractively valued from a stock price perspective.

Comparison of NLY’s Recent Leverage, Hedging Coverage Ratio, BV, Economic Return (Loss), and Valuation to Twenty mREIT Peers:

Many readers have continued to request that I provide various metrics for the mREIT stocks I currently cover in ranking order. As such, without showing four additional tables, once again using Table 1 above as a reference, the following were the on-balance sheet and at-risk (total) leverage ratios of NLY and the twenty mREIT peers as of 6/30/2020 (in order of lowest to highest at-risk (total) leverage ratio; excluding borrowings collateralized by assets held in “securitization trusts” and/or “variable interest entities” [VIE]; non-recourse):

1) NYMT: 0.5x on-balance sheet leverage; 0.5x at-risk (total) leverage

2) IVR: 0.6x on-balance sheet leverage; 0.6x at-risk (total) leverage

2) PMT: 2.9x on-balance sheet leverage; 0.6x at-risk (total) leverage

4) EFC: 1.5x on-balance sheet leverage; 1.2x at-risk (total) leverage

4) MITT: 1.2x on-balance sheet leverage; 1.2x at-risk (total) leverage

6) CIM: 1.8x on-balance sheet leverage; 1.8x at-risk (total) leverage

7) AI: 1.9x on-balance sheet leverage; 1.9x at-risk (total) leverage

7) NRZ: 2.1x on-balance sheet leverage; 1.9x at-risk (total) leverage

9) MFA: 2.0x on-balance sheet leverage; 2.0x at-risk (total) leverage

10) GPMT: 2.5x on-balance sheet leverage; 2.5x at-risk (total) leverage

11) BXMT: 2.9x on-balance sheet leverage; 2.9x at-risk (total) leverage

12) WMC: 3.0x on-balance sheet leverage; 3.0x at-risk (total) leverage

13) CHMI: 4.5x on-balance sheet leverage; 4.4x at-risk (total) leverage

14) ANH: 4.6x on-balance sheet leverage; 5.2x at-risk (total) leverage

15) NLY: 5.1x on-balance sheet leverage; 6.4x at-risk (total) leverage

16) TWO: 6.3x on-balance sheet leverage; 7.4x at-risk (total) leverage

17) ARR: 5.5x on-balance sheet leverage; 7.7x at-risk (total) leverage

18) DX: 3.2x on-balance sheet leverage; 7.8x at-risk (total) leverage

19) CMO: 8.3x on-balance sheet leverage; 8.3x at-risk (total) leverage

20) AGNC: 6.8x on-balance sheet leverage; 8.8x at-risk (total) non-tangible leverage

21) ORC: 9.2x on-balance sheet leverage; 9.8x at-risk (total) leverage

Regarding several mREITs’ leverage ratios within Table 1, some figures may not “exactly” match to what was reported by each company. This is due to the fact not all companies within the mREIT sector have a singular, “uniform” methodology for computing its leverage ratio. To provide a consistent sector-wide metric, I have calculated each company’s leverage ratios based on one uniform methodology. There are no notable differences between each company’s internally reported leverage ratios and the uniform leverage ratios I have calculated.

Second, the following was the hedging coverage ratio for NLY and the twenty mREIT peers as of 6/30/2020 (in order of lowest to highest ratio):

The REIT Forum Data

Next, the following were the economic return (loss) percentages for NLY and the twenty mREIT peers during the trailing twelve-months ended 6/30/2020 (combination of annual change in BV and dividends accrued for/paid; in order of highest to lowest economic return/lowest to highest economic loss):

1) DX: 4.64% trailing twelve-month economic return

2) BXMT: 3.86% trailing twelve-month economic return (different general methodology for valuing commercial whole loans versus most other mortgage-related investments)

3) PMT: 0.91% trailing twelve-month economic return

4) AGNC: 0.68% trailing twelve-month economic non-tangible return

5) NLY: 0.32% trailing twelve-month economic return

6) GPMT: (2.29%) trailing twelve-month economic loss (different general methodology for valuing commercial whole loans versus most other mortgage-related investments)

7) ORC: (7.92%) trailing twelve-month economic loss

8) EFC: (8.99%) trailing twelve-month economic loss

9) CHMI: (11.43%) trailing twelve-month economic loss

10) NYMT: (16.52%) trailing twelve-month economic loss

11) CMO: (17.58%) trailing twelve-month economic loss

12) AI: (22.05%) trailing twelve-month economic loss

13) CIM: (23.46%) trailing twelve-month economic loss

14) NRZ: (26.28%) trailing twelve-month economic loss

15) ANH: (30.68%) trailing twelve-month economic loss

16) MFA: (30.94%) trailing twelve-month economic loss

17) ARR: (37.90%) trailing twelve-month economic loss

18) TWO: (41.92%) trailing twelve-month economic loss

19) WMC: (63.94%) trailing twelve-month economic loss

20) IVR: (71.38%) trailing twelve-month economic loss

21) MITT: (79.05%) trailing twelve-month economic loss

Finally, the following were the 9/11/2020 premium (discount) to my estimated CURRENT BV (BV as of 9/11/2020) percentages for NLY and the twenty mREIT peers (in order of largest to smallest discount/smallest to largest premium):

1) GPMT: (62.61%) discount to my estimated BV as of 9/11/2020 (different general methodology for valuing commercial whole loans versus most other mortgage-related investments)

2) AI: (53.22%) discount to my estimated BV as of 9/11/2020

3) NYMT: (44.89%) discount to my estimated BV as of 9/11/2020

4) ANH: (40.69%) discount to my estimated BV as of 9/11/2020

5) MFA: (40.65%) discount to my estimated BV as of 9/11/2020

6) WMC: (38.77%) discount to my estimated BV as of 9/11/2020

7) NRZ: (33.61%) discount to my estimated BV as of 9/11/2020

8) CHMI: (31.85%) discount to my estimated BV as of 9/11/2020

9) TWO: (30.95%) discount to my estimated BV as of 9/11/2020*

* = My estimated BV as of 9/11/2020 takes into consideration the following: 1) reverses out the previously accrued termination fee payable to the prior external manager. TWO’s independent board of directors (“BoD”) has previously stated the company terminated the management agreement WITH CAUSE which equates to no termination fee being owed (currently in legal proceedings; an event I will continue to monitor)

10) EFC: (24.21%) discount to my estimated BV as of 9/11/2020

11) CIM: (20.37%) discount to my estimated BV as of 9/11/2020

12) IVR: (16.62%) discount to my estimated BV as of 9/11/2020

13) PMT: (16.48%) discount to my estimated BV as of 9/11/2020

14) CMO: (16.17%) discount to my estimated BV as of 9/11/2020

15) NLY: (15.57%) discount to my estimated BV as of 9/11/2020

16) AGNC: (15.26%) discount to my estimated non-tangible BV as of 9/11/2020**

** = Estimated tangible BV of $15.70 per share as of 9/11/2020 (when excluding goodwill and other intangible assets); a (10.13%) discount

17) ARR: (14.81%) discount to my estimated BV as of 9/11/2020

18) BXMT: (11.45%) discount to my estimated BV as of 9/11/2020 (different general methodology for valuing commercial whole loans versus most other mortgage-related investments)

19) DX: (11.25%) discount to my estimated BV as of 9/11/2020

20) ORC: (8.36%) discount to my estimated BV as of 9/11/2020

21) MITT: 8.75% premium to my estimated BV as of 9/11/2020***

*** = My estimated BV as of 9/11/2020 takes into consideration the following: 1) accounts for the preferred dividends owed to preferred shareholders (cumulative impact); and 2) accounts for the liquidation preference of the company’s preferred stock versus net proceeds (consistent sector-wide methodology)

Conclusions Drawn (PART 1):

PART 1 of this article has analyzed NLY and twenty mREIT peers in regards to the following metrics: 1) leverage as of 6/30/2020; 2) hedging coverage ratio as of 6/30/2020; 3) trailing twelve-month economic return (loss); and 4) premium (discount) to my estimated CURRENT BV.

First, NLY’s at-risk (total) leverage as of 6/30/2020 was modestly above the mREIT sector average. However, when compared to the company’s fixed-rate agency mREIT peers within this analysis, NLY’s at-risk leverage ratio was now slightly below average. Over the prior several years, NLY typically ran below average leverage versus the company’s fixed-rate agency mREIT peers.

Second, NLY’s hedging coverage ratio was now exactly at the fixed-rate agency mREIT average as of 6/30/2020. As a whole, most mREIT peers have notably decreased their hedging coverage ratios over the past two quarters. While this is would certainly “ring the alarm bells” if markets experienced a rapid rise in mortgage interest rates/U.S. Treasury yields, this scenario has not played out during the third quarter of 2020 (through 9/11/2020). As such, thus far NLY has “gotten away” with utilizing a lower number of derivative instruments when compared to 2018-2019. Last quarter, I correctly anticipated NLY’s hedging coverage ratio would “gravitate” toward the agency mREIT average as 2020 progressed.

Third, NLY’s trailing twelve-month economic return was more attractive versus the mREIT sector average. NLY outperformed most of the company’s agency mREIT peers regarding this metric and nearly matched the performance of one of its closest sector peers, AGNC. This was mainly due to the recent composition of NLY’s MBS/investment and derivatives portfolio and the net movement of mortgage interest rates/U.S. Treasury yields during this timeframe. Due to NLY’s overall size and agency MBS liquidity, this company fared better versus most mREIT sector peers during the COVID-19 pandemic.

Finally, NLY’s current valuation, when compared to my estimate of each mREIT’s CURRENT BV (BV as of 9/11/2020), was now at a slightly higher valuation versus the mREIT peer average within this analysis. Still, through the metrics provided within this two-part sector comparison article (including factors/metrics not discussed), I believe NLY “deserves” to trade at a premium valuation to most mREIT peers. As such, this is one of the reasons why I continue to believe NLY remains very attractively valued. I would strongly suggest readers consider CURRENT BVs (as opposed to prior period BVs) when assessing whether a stock is attractively valued or not.

When taking a look at the events/trends that have occurred during the third quarter of 2020, MBS pricing has remained strong while there have been relatively unchanged valuation fluctuations within most derivative instruments.As such, a minor-modest positive relationship between MBS pricing and derivative instrument valuations has occurred. Generally speaking, option adjusted spreads (“OAS”) have slightly-modestly tightened during the quarter (through 9/11/2020).

The relationship between MBS/investment pricing and derivative instrument valuations needs to be constantly monitored (which I continually perform throughout the quarter). If I start to see a more notable positive/negative relationship unfold, I will inform readers through several avenues within Seeking Alpha (through articles, the live chat feature of The REIT Forum, and/or comments).

My BUY, SELL, or HOLD Recommendation:

From the analysis provided above (using Table 1 as a reference), including additional catalysts/factors not discussed within this article, I currently rate NLY as a SELL when I believe the company’s stock price is trading at or greater than a 5% premium to my projected CURRENT BV (BV as of 9/11/2020; $8.80 per share), a HOLD when trading at less than a 5% premium through less than a (5%) discount to my projected CURRENT BV, and a BUY when trading at or greater than a (5%) discount to my projected CURRENT BV. These percentage ranges are a 2.5% increase when compared to my last public NLY article (approximately 3 months ago; subscribers of the REIT Forum get weekly updates on recommendation range changes).

Therefore, I currently rate NLY as a STRONG BUY.

As such, I currently believe NLY is notably undervalued from a stock price perspective. My current price target for NLY is approximately $9.25 per share. This is currently the price where my recommendation would change to a SELL. The current price where my recommendation would change to a HOLD is approximately $8.35 per share.

Along with the data presented within this article, this recommendation considers the following mREIT catalysts/factors: 1) projected future MBS/investment price movements; 2) projected future derivative valuations; and 3) projected near-term dividend per share rates. This recommendation also considers the eight Fed Funds Rate increases by the FOMC during December 2016-2018 (a more hawkish tone/rhetoric when compared to 2014-2016), the three Fed Funds Rate decreases during 2019 due to the more dovish tone/rhetoric regarding overall monetary policy as a result of recent macroeconomic trends/events, and the recent very quick “plunge” in the Fed Funds Rate to near 0%. This also considers the previous wind-down/decrease of the Fed’s balance sheet through gradual runoff/partial non-reinvestment (which began in October 2017 which increased spread/basis risk) and the prior “easing” of this wind-down that started in May 2019 regarding U.S. Treasuries and August 2019 regarding agency MBS (which partially reduced spread/basis risk when volatility remains subdued). This also considers the recent early Spring 2020 announcement of the start of another round of “quantitative easing” that includes the Fed specifically purchasing agency MBS (and “rolling over” all principal and interest payments into new agency MBS) which should bolster prices while keeping long-term rates low.

mREIT Sector Recommendations as of 2/21/2020 and 9/11/2020:

Finally, once again using Table 1 above as a reference, I want to highlight to readers what we (myself along with Colorado Wealth Management and his team) conveyed to readers when it came to sector recommendations as of 2/21/2020 (pre sell-off).

As of 2/21/2020, we had a BUY recommendation on the following mREIT stocks analyzed above (in no particular order):1) ANH.

As of 2/21/2020, we had a HOLD recommendation on the following mREIT stocks analyzed above (in no particular order):1) AI; 2) ARR; 3) CHMI; 4) MITT; 5) GPMT; 6) NRZ; 7) NYMT; and 8) PMT.

As of 2/21/2020, we had a SELL recommendation on the following mREIT stocks analyzed above (in no particular order):1) AGNC; 2) CMO; 3) NLY; 4) ORC; 5) DX; 6) EFC; 7) MFA; 8) IVR; 9) TWO; and 10) WMC.

As of 2/21/2020, we had a STRONG SELL recommendation on the following mREIT stocks analyzed above (in no particular order):1) CIM; and 2) BXMT.

So, prior to the COVID-19 sell-off, as of 2/21/2020 I/we had 0 mREITs rated as a STRONG BUY, only 1 rated as a BUY, 8 rated as a HOLD, 10 rated as a SELL (including NLY), and 2 rated as a STRONG SELL. Simply put, out of my seven years of covering this particular sector on Seeking Alpha, this was one of the most “bearish” overall weekly recommendation range classifications I have provided. Investors who “heeded” this advice were, at least, able to “lock-in” some notable gains (as sector valuations “ran up” after positive Q4 2019 earnings) which helped offset subsequent sector/market losses. At this general point in time, this was in direct contradiction to most contributors that continually cover the mREIT sector.

Our outlook notably reversed course during late March-April 2020 as the market “pummeled” both strong and weak mREIT peers (notable price dislocations; in particular most agency mREIT peers). Our service quickly moved most recommendations to BUYS or STRONG BUYS immediately when this notable price dislocation was occurring. In addition, we quickly added proportionately large positions across several sector peers and “never looked backed” (subscribers to our service can attest to these positions as we disclose our trades in “real time” (the same day we place a place).

Still using Table 1 above as a reference, I want to highlight to readers what we are conveying to subscribers when it comes to sector recommendations as of 9/11/2020 (last week’s close).

As of 9/11/2020, we have a STRONG BUY recommendation on the following mREIT stocks analyzed above:1) AI; 2) NLY; 3) GPMT; 4) NRZ; and 5) NYMT.

As of 9/11/2020, we currently have a BUY recommendation on the following mREIT stocks analyzed above (in no particular order):1) AGNC; 2) CHMI; 3) CMO; 4) DX; 5) TWO; 6) ANH; 7) CIM; 8) EFC; 9) MFA; and 10) PMT.

As of 9/11/2020, we currently have a HOLD recommendation on the following mREIT stock analyzed above (in no particular order):1) ARR; 2) ORC; 3) WMC; and 4) BXMT.

As of 9/11/2020, we currently have a SELL recommendation on the following mREIT stocks analyzed above (in no particular order):1) IVR.

As of 9/11/2020, we currently have a STRONG SELL recommendation on the following mREIT stocks analyzed above (in no particular order): 1) MITT.

So, as of 9/11/2020 we now have 5 mREITs rated as a STRONG BUY, 10 rated as a BUY, 4 rated as a HOLD, only 1 rated as a SELL, and only 1 rated as a STRONG SELL. Simply put, a notable difference in value/outlook when compared to February 2020.

Each investor's BUY, SELL, or HOLD decision is based on one's risk tolerance, time horizon, and dividend income goals. My personal recommendation will not fit each reader’s current investing strategy.The factual information provided within this article is intended to help assist readers when it comes to investing strategies/decisions.

Current/Recent mREIT Sector Stock Disclosures:

On 3/18/2020, I initiated a position in NLY at a weighted average purchase price of $5.05 per share. This weighted average per share price excludes all dividends received/reinvested.

On 1/31/2017, I initiated a position in NRZ at a weighted average purchase price of $15.10 per share. On 6/29/2017, 7/7/2017, and 12/21/2018, I increased my position in NRZ at a weighted average purchase price of $15.775, $15.18, and $14.475 per share, respectively. When combined, my NRZ position had a weighted average purchase price of $14.912 per share. This weighted average per share price excluded all dividends received/reinvested. On 2/6/2020, I sold my entire NRZ position at a weighted average sales price of $17.555 per share as my price target, at the time, of $17.50 per share was surpassed. This calculates to a weighted average realized gain and total return of 17.7% and 41.2%, respectively. I held this position, on a weighted average basis, for approximately 20 months.

On 6/29/2017, I initiated a position in CHMI at a weighted average purchase price of $18.425 per share. On 10/6/2017, 10/26/2017, 11/6/2017, 1/29/2018, 10/12/2018, 6/6/2019, 7/23/2019, 9/5/2019, 3/16/2020, and 4/6/2020 I increased my position in CHMI at a weighted average purchase price of $18.015, $18.245, $17.71, $17.145, $17.235, $16.315, $15.325, $12.435, $8.55, and $3.645 per share, respectively. When combined, my CHMI position has a weighted average purchase price of $7.735 per share (yes, my last 3 purchases were proportionately large). This weighted average per share price excludes all dividends received/reinvested.

On 8/31/2017, I initiated a position in CHMI’s Series A preferred stock, (CHMI.PA). On 9/12/2017 and 4/6/2020, I increased my position in CHMI-A at a weighted average purchase price of $25.145 and $10.945 per share, respectively. When combined, my CHMI-A position had a weighted average purchase price of $18.071 per share. This weighted average per share price excluded all dividends received/reinvested. On 6/8/2020, I sold my entire CHMI-A position at a weighted average sales price of $24.273 per share. This calculates to a weighted average realized gain and total return of 34.3% and 49.4%, respectively. I held this position, on a weighted average basis, for approximately 1.7 years. This calculates to a weighted average annualized total return of 29.7%.

On 1/29/2018, I initiated a position in TWO at a weighted average purchase price of $15.155 per share. On 4/17/2019, I increased my position in TWO at a weighted average purchase price of $13.165 per share. When combined, my TWO position had a weighted average purchase price of $13.825 per share. This weighted average per share price excluded all dividends received/reinvested. On 2/3/2020, I sold my entire TWO position at a weighted average sales price of $15.355 per share as my price target, at the time, of $15.25 per share was surpassed. This calculates to a weighted average realized gain and total return of 11.0% and 25.2%, respectively. I held this position, on a weighted average basis, for approximately 13 months.

On 3/8/2018, I initiated a position in NYMT’s Series D preferred stock, (NYMTN). On 4/6/2018, 4/27/2018, 10/12/2018, 12/7/2018, 12/18/2018, and 3/22/2019 I increased my position in NYMTN. When combined, my NYMTN position has a weighted average purchase price of $22.379 per share. This weighted average per share price excludes all dividends received/reinvested.

On 10/12/2018, I initiated a position in GPMT at a weighted average purchase price of $18.155 per share. On 5/12/2020, 5/27/2020, 5/28/2020, 8/26/2020, 9/10/2020, and 9/11/2020, I increased my position in GPMT at a weighted average purchase price of $4.745, $5.144, $5.086, $6.70, $6.19, and $6.045 per share, respectively. My last two purchases make up approximately 50% of my total position (to put things in better perspective). When combined, my GPMT position has a weighted average purchase price of $6.234 per share. This weighted average per share price excludes all dividends received/reinvested.

On 10/12/2018, I initiated a position in MITT at a weighted average purchase price of $17.105 per share. On 4/17/2019 and 6/3/2019, I increased my position in MITT at a weighted average purchase price of $16.22 and $15.52 per share, respectively. When combined, my MITT position had a weighted average purchase price of $15.946 per share. This weighted average per share price excludes all dividends received/reinvested. On 5/11/2020, I sold my entire MITT position at a weighted average sales price of $2.115 per share as my price target, at the time, was surpassed (as MITT’s estimated BV as of 4/30/2020 was even lower versus my previously projected (75%) quarterly BV decrease [6/30/2020 versus 3/31/2020]). This was my first “realized total loss” within either the mREIT or business development company (“BDC”) sector since I began writing here on Seeking Alpha in 2013. With that said, my proportional allocation in MITT (versus the rest of the mREIT sector) was small.

On 6/3/2019, I initiated a position in ARR at a weighted average purchase price of $17.545 per share. On 9/10/2019, I increased my position in ARR at a weighted average purchase price of $16.785 per share. When combined, my ARR position had a weighted average purchase price of $16.975 per share. This weighted average per share price excluded all dividends received/reinvested. On 2/20/2020, I sold my entire ARR position at a weighted average sales price of $21.045 per share as my price target, at the time, of $20.90 per share was surpassed. This calculates to a weighted average non-annualized realized gain and total return of 24.0% and 31.0%, respectively. I held this position, on a weighted average basis, for approximately 6 months.

On 6/3/2019, I initiated a position in IVR at a weighted average purchase price of $15.49 per share. This weighted average per share price excludes all dividends received/reinvested. On 2/14/2020, I sold my entire IVR position at a weighted average sales price of $17.965 per share as my price target, at the time, of $17.95 per share was surpassed. This calculates to a weighted average non-annualized realized gain and total return of 16.0% and 25.0%, respectively. I held this position for approximately 8 months.

On 11/22/2019, I initiated a position in ANH at a weighted average purchase price of $3.475 per share. This weighted average per share price excludes all dividends received/reinvested.

On 11/22/2019, I initiated a position in AI’s Senior Notes Due 2023 (AIW) at a weighted average purchase price of $24.13 per share ($25 being par). On 3/10/2020, 3/13/2020, and 3/19/2020, I increased by position in AIW at a weighted average purchase price of $23.50, $19.75, and $9.31 per share, respectively. When combined, my AIW has a weighted average purchase price of $14.804 per share. This weighted average per share price excludes all interest received/compounded.

On 12/31/2019, I initiated a position in AI’s Senior Notes Due 2025 (AIC) at a weighted average purchase price of $24.00 per share ($25 being par). On 3/10/2020 and 3/19/2020, I increased by position in AIC at a weighted average purchase price of $23.72 and $8.71 per share, respectively. When combined, my AIC has a weighted average purchase price of $16.182 per share. This weighted average per share price excluded all interest received/compounded. On 9/2/2020-9/4/2020, I sold my entire AIC position at a weighted average sales price of $23.55 per share. This calculates to a weighted average non-annualized realized gain and total return of 45.5% and 51.1%, respectively. I held this position for approximately 6.5 months.

On 1/2/2020, I initiated a position in AI at a weighted average purchase price of $5.57 per share. On 1/9/2020 and 3/16/2020, I increased my position in AI at a weighted average purchase price of $5.59 and $3.25 per share, respectively. When combined, my AI position has a weighted average purchase price of $4.027 per share. This weighted average per share price excludes all dividends received/reinvested.

On 3/18/2020, I once again initiated a position in AGNC at a weighted average purchase price of $7.115 per share. This weighted average per share price excludes all dividends received/reinvested.

On 4/6/2020, I initiated a position in CHMI’s Series B preferred stock, (CHMI.PB) at a weighted average purchase price of $10.65 per share. This weighted average per share price excluded all dividends received/reinvested. On 6/19/2020-6/24/2020, I sold my entire CHMI-B position at a weighted average sales price of $22.045 per share. This calculates to a weighted average realized gain and total return of 107.0%. I held this position for approximately 2.5 months.

Final Note: All trades/investments I have performed over the past several years have been disclosed to readers in “real time” (that day at the latest) via either the StockTalks feature of Seeking Alpha or, more recently, the “live chat” feature of the Marketplace Service the REIT Forum (which cannot be changed/altered). Through these resources, readers can look up all my prior disclosures (buys/sells) regarding all companies I cover here at Seeking Alpha (see my profile page for a list of all stocks covered). Through StockTalk disclosures and/or the live chat feature of the REIT Forum, at the end of August 2020 I had an unrealized/realized gain “success rate” of 85.5% and a total return (includes dividends received) success rate of 92.7% out of 55 total past and present positions (updated monthly; multiple purchases/sales in one stock count as one overall position until fully closed out). I have only 1 realized “total loss” in any of my past/sold positions. Both percentages experienced a modest increase, when compared to April-May 2020, as a direct result of the recent partial market rally to counter previous fears/panic surrounding the COVID-19 pandemic. In addition, in early April 2020, I initiated several new positions and increased several existing positions at attractive-very attractive prices versus pricing as of 6/30/2020. I encourage other Seeking Alpha contributors to provide real time buy and sell updates for their readers which would ultimately lead to greater transparency/credibility. Starting in January 2020, I have transitioned all my real-time purchase and sale disclosures solely to members of the REIT Forum. All applicable public articles will still have my sector purchase and sale disclosures (just not in real time). Please disregard any minor “cosmetic” typos if/when applicable.

I am currently "teaming up" with Colorado Wealth Management to provide intra-quarter CURRENT BV and NAV per share projections on all 21 mREIT and 15 BDC stocks I currently cover. These very informative (and “premium”) projections are provided through Colorado's S.A. Marketplace service. In addition, this includes additional data/analytics, weekly sector recommendations (including ranges), and exclusive "rapid fire" mREIT and BDC articles after earnings. For a full list of benefits I provide to the REIT Forum subscribers, please see my profile page.