Investment Thesis

We are bullish Edwards Lifesciences (NYSE:EW) shares and believe the name is worth visiting for those seeking exposure to valve therapies and cardiovascular interventions. EW hosts a robust portfolio that is well insulated, via diversified offerings within the valve surgery space, and this widens the company's economic bastion over the longer-term. Specifically, key segment offerings in aortic, mitral and tricuspid valve products attest to EW's market positioning and the capacity to capture additional market share into the future.

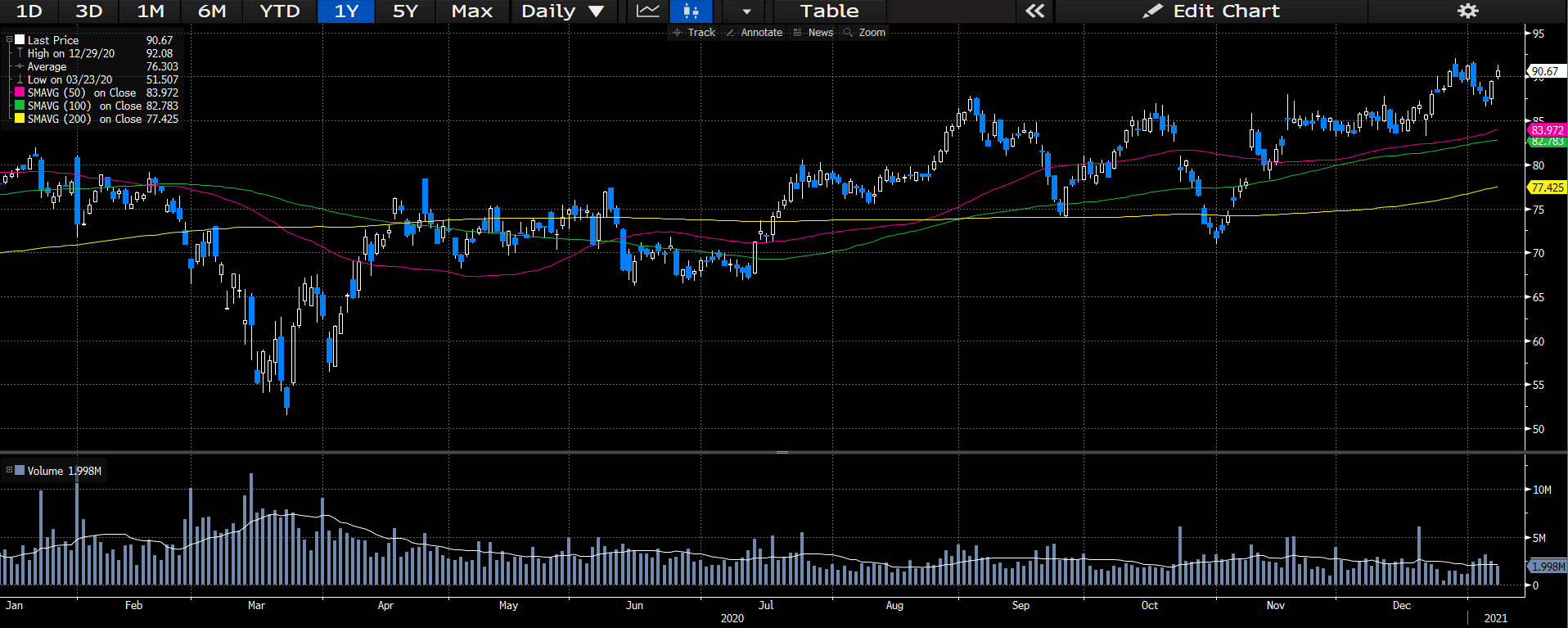

Exhibit 1. Single-year price performance

Data Source: Author's Bloomberg Terminal

Balancing this view is the fact that the market may have already priced in much of the future growth at current valuations, which may present as a challenge to those seeking value-type propositions. Additionally, given the apparent sector and factor rotation away from growth-type names into more value orientated themes, this may present as challenges to EW's story on the charts over the coming periods. We would point investors to the company's success in generating return over the invested capital outlay since 2011, that helps justify the premium attached to the valuation, and feeds into our own thesis for shares over the coming periods. Here, we cover all of the necessary moving parts in the investment debate, for the benefit of investors in their own investment reasoning.

Robust Revenue Outlook

We have covered EW several times in the past, and consider the name a key holding for our long-term portfolio outlook that mirrors a market-neutral approach with exposure to equity factors such as momentum and high ROIC. On a fundamental basis, it seems that EW is able to constantly illustrate the evolution of the TAVR platform, and remain optimistic of the long-term TAVR outlook, as management look to expand the TAM for this segment over the coming years. To