mcsilvey

According to Fidelity back in December 2023, the outlook for real estate in 2024 is likely to rebound from 2023 levels due to more stable and potentially lower interest rates. The real estate market in 2024 should be calmer if nothing else. One stock that I believe offers good value before the market rebounds is the REIT from Invesco Mortgage Capital (NYSE:IVR) offering income investors an 18+% yield.

Fidelity

While the real estate market started to show signs of recovery in the first quarter of 2024, recent economic news has stymied those green shoots of growth that were sprouting on hopes of reduced interest rates. Last month, after President Biden announced a plan to lower housing costs, many REITs and other real estate stocks drifted higher, but now in April, those stocks in the real estate sector have dropped again. The sector as represented by XLRE is down about -9% YTD.

Seeking Alpha

However, even though prices are down for many REITs, quite a few of them announced dividend increases in Q1. In fact, according to S&P Global Market Intelligence, at least 35 REITs announced dividend increases in Q1, as shown in the table below.

S&P Global Market Intelligence

Those dividend increases indicate that a rebound is indeed occurring and that prospects for improved shareholder returns from dividend paying REITs are improving.

One REIT that has not increased the dividend yet this year, but has not decreased it either, is Invesco Mortgage Capital. Invesco was incorporated in 2008 and is based in Atlanta, Georgia. From the IVR company profile on Seeking Alpha:

Invesco Mortgage Capital Inc. operates as a real estate investment trust that invests, finances, and manages mortgage-backed securities and other mortgage-related assets in the United States. It invests in residential mortgage-backed securities and commercial mortgage-backed securities that are guaranteed by a U.S. government agency or federally chartered corporation; RMBS and CMBS that are not issued or guaranteed by the United States government agency or federally chartered corporation; the United States treasury securities; real estate-related financing arrangements; to-be-announced securities forward contracts to purchase RMBS; and commercial mortgage loans.

As a REIT the company is required to distribute at least 90% of its taxable income to shareholders and in the case of IVR that dividend amount is $0.40 per quarter, most recently declared on March 26, 2024. At the current market price of $8.53 that results in an annual yield of 18.5%. Despite the high yield, many investors would not touch IVR with a ten-foot pole due in part to its five-year price history. The Covid crash in 2020 significantly impacted IVR stock performance.

Seeking Alpha

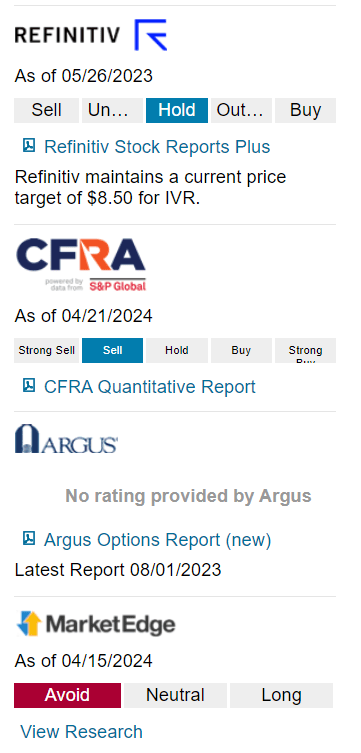

Most analysts have been bearish on IVR stock ever since the Covid crash. More recently, some analysts have begun to upgrade their ratings.

- On April 12, 2024 - EVA upgraded Invesco Mortgage Capital REIT Ord Shares from UNDERWEIGHT to HOLD.

While other analysts continue to rate IVR a Hold or Sell as shown on the Schwab website, some analysts like me see an opportunity as interest rates appear to be stabilizing, if not yet decreasing.

Schwab

The most recent SA analyst coverage of IVR from January of this year suggested that the REIT is a Buy with interest rates expected to come down. At least, that is what investors were expecting back in January due to the “Fed Pivot”. Now, however, it seems that interest rates may not be coming down any time soon. Regardless of whether interest rates remain the same or move lower later this year, I rate IVR a Buy at the current price and given the high yield income that appears to be adequately covered based on Q4 23 earnings results.

IVR Q4 2023 Earnings Summary

When examining the IVR earnings results from Q4 2023, the first thing to note is that net income per common share increased to $0.46 (more than covering the $0.40 dividend) compared to a net loss of $1.62 in Q3 2023. Earnings available for distribution per common share (a GAAP accounting measure) was $0.95, down from $1.51 in Q3'23. Book value increased to $10.00 in the quarter from $9.93 as of September 30.

Invesco Q423 presentation

In the earnings update from CEO John Anzalone, he summarized the positive Q4 results:

During the quarter, we reduced risk within the portfolio as volatility initially increased, and subsequently returned leverage to our target range as volatility subsided. Our debt-to-equity ratio ended the fourth quarter at 5.7x, down from 6.4x as of September 30th. As of the end of the quarter, substantially all our $5.1 billion investment portfolio was invested in Agency RMBS, and we maintained a sizeable balance of unrestricted cash and unencumbered investments totaling $422 million.

Earnings available for distribution for the period benefited from attractive interest income on our target assets, favorable funding and low-cost, pay-fixed swaps. For the quarter, EAD per common share was $0.95 compared to $1.51 for the third quarter, reflecting declines in interest income on investments and interest rate swaps in connection with our reduction in leverage and adjustments to our swap portfolio.

Regarding the outlook for the agency MBS asset class, the company remains cautious yet optimistic with potentially stabilizing interest rates. The long-term outlook for the RMBS business remains intact:

“We believe Agency RMBS investors stand to benefit from attractive valuations, favorable funding and a steeper yield curve as the macro environment stabilizes."

As of the IVR Q4 23 earnings call on February 23, 2024, the CEO was noting that challenges remain in the MBS sector.

Over the first six weeks of 2024, mortgage valuations have been challenged with lower coupons underperforming higher coupons. As of February 16th, our book value per common share is down moderately, estimated to be between $9.50 and $9.88. While evolving expectations around the timing of changes in monetary policy may bring challenges in the coming months, we believe that a potential reduction in interest rate volatility combined with compelling valuations and favorable funding conditions will support an attractive investment environment for agency mortgages in 2024.

Indeed, since that time, the impacts of uncertainty around monetary policy have led to additional challenges for the sector.

Comparison to Other High Yield mREITs

Compared to DX, NLY, and AGNC, the six-month total return from IVR is substantially higher at 35% compared to 24-25% returns from the other three mREITs.

Seeking Alpha

For income investors, the distribution yield from IVR is also the highest of the four. It is also the smallest of the four mREITs based on market cap.

Ticker | Market Cap | Yield |

AGNC | 6.4B | 15.37% |

DX | 677M | 13.20% |

IVR | 407M | 18.5% |

NLY | 9.17B | 14% |

Q1 2024 mREIT Earnings Results

While Q1 results are just now being announced, AGNC was one of the first to report results on April 22 and the report was mixed but with a generally positive outlook for the remainder of 2024.

Favorable dynamics for fixed income investors continued through Q1, the company said. ""Particularly beneficial for agency mortgage-backed securities investors in the first quarter, interest rate volatility declined meaningfully, agency MBS spreads remained relatively stable, and the Federal Reserve indicated that short term rates had likely reached their pinnacle for this monetary policy cycle," said President and CEO Peter Federico.

Dynex Capital also announced Q1 results on April 22 and those results were not as good as investors had hoped, although gains from hedging offset some of the losses that the company experienced.

Q1 earnings available for distribution were -$17.7M, or -$0.30 per share, missing the average analyst estimate of -$0.16 per share. That declined from -$13.9M, or -$0.24 per share, in Q4 2023. Net gains on Dynex's hedging portfolio exceeded net losses on its investment portfolio by $37.3M. "Though the 10-year U.S. Treasury rate increased over 30 basis points during the first quarter, which negatively impacted the fair value of the company's investment portfolio, losses were offset by modest spread tightening on some of the company's investments and gains on U.S. Treasury futures used as interest rate hedging instruments," the company said.

After the market close on 4/24/24, NLY reported Q1 results that were also mixed with good and bad news including GAAP net income of $0.85 per share but EAD of only $0.64 while declaring a quarterly common stock dividend of $0.65 per share.

"We were pleased to generate a 4.8% economic return in the first quarter as each of our three investment strategies contributed to our book value appreciation, as well as generated stable earnings," commented David Finkelstein, Annaly's Chief Executive Officer and Chief Investment Officer. "Our core Agency MBS portfolio performed well as spreads were supported during the first quarter by lower volatility and an improved supply and demand picture.

On the NLY earnings call transcript, CEO Finkelstein also noted that the economy continued to improve and the Fed’s mandate changed in the first quarter with regards to selling off Treasury assets:

First quarter of 2024 was characterized by surprisingly resilient economic data, a healthy labor market, and an uptick in inflation. Consequently, interest rates sold off modestly on the quarter as the market priced out roughly half of the rate cuts that were expected at the beginning of the year. Now despite rising rates, risk assets performed well over the quarter as volatility declined and money flowed into both equity and fixed income markets.

Banks also reemerged as modest buyers of Treasuries and Agency MBS in the first quarter, a welcome development given their absence over the past couple of years. In addition, the Federal Reserve made it clear that it considers policy rates and balance sheet management to be separate tools as they have begun discussing slowing the pace the Fed's Treasury securities run off.

IVR Q1 2024 Earnings Estimates

This is all relatively good news for mortgage REITs in general, and thus IVR should also benefit from these improving conditions when they report Q1 earnings. That announcement is currently scheduled for May 6 (or May 9 according to Schwab). The consensus earnings estimate for Q1 24 is $1.15 (according to Schwab, $1.10 according to SA) compared to $0.95 in Q4 23. IVR beat estimates in 3 of the past 4 quarters and I expect that they will beat estimates again in Q1. There has been 1 upward and 1 downward EPS revision in the past 90 days.

IVR Earnings Summary (Seeking Alpha)

In a March 2024 update from Invesco portfolio managers Clint Dudley and Brian Norris, the company observes that Agency MBS represents an attractive opportunity for long-term investors.

Comparing current valuations of both investment grade corporates and Agency MBS relative to long-term historical averages reveals the former is trading rich while the latter is more attractive. We find the most relevant valuation metric for comparison of the two asset classes in the current environment is the zero-volatility spread. ZV spread is the yield difference relative to US Treasuries with similar duration, in basis points, unadjusted for both default and prepayment risk.

The chart on the left illustrates the ZV spread differential between the Bloomberg Agency MBS Index vs. the Bloomberg US Investment Grade Index, while the chart on the right displays higher coupon Agency MBS relative to the same investment grade corporate index. Currently, the ZV spread of the Bloomberg US Investment Grade Corporate Index is in the 7th percentile vs. the last 10 years, while the ZV spread of the Bloomberg US Agency MBS Index is in the 55th percentile over the same period. Furthermore, recently issued, higher coupon Agency MBS are even more attractive, with a ZV spread currently in the 90th percentile over the past 10 years.

Invesco

What’s the Rate Outlook for H2 2024?

Of course, if the Fed eventually reduces interest rates that will further improve the outlook for Agency MBS as others have noted, and the portfolio managers at Invesco see the medium-term opportunity to be unique and highly attractive based on the premise that rates will eventually come down.

Our medium-term outlook calls for a modest slowdown in economic growth in the US and gradual cuts in the Federal Funds target rate, resulting in a steeper yield curve and lower interest rate volatility. While cuts in the Fed Funds rate and a steeper yield curve create a favorable backdrop for most risk assets, Agency MBS stands to benefit the most from a decline in interest rate volatility as option costs normalize.

The latest GDP report for Q1 confirms that the economy is indeed slowing down. However, inflation remains sticky leading to concerns of stagflation, which would not be positive for risk assets.

“Stagflation is a growing risk after GDP missed and the price index surprised to the upside. If inflation isn’t getting better with such a weak growth, you have to wonder if the trend toward lower prices will continue. The bump in yields after the report suggests rate cuts are increasingly in doubt," said David Russell, global head of Market Strategy at TradeStation.

Additional reports coming out this week should provide more clarity on the inflation fight, but the market is reacting to the GDP news as if rate cuts are now off the table for even longer. If rates stay “higher for longer” then the recovery in the REIT sector could take even longer to unfold.

Risks to Consider Before Buying IVR

The biggest risk to consider with IVR due to its concentrated holdings of Agency MBS assets is that of continued interest rate uncertainty and volatility. As explained in the March update from the portfolio managers, the rapid increase in interest rates that occurred beginning March 2022 caused the Agency MBS sector to underperform both US Treasuries and investment grade bonds due to the uncertainty in their cash flows. While interest rates have stabilized for now, any potential additional increases to the base rate could cause the Agency MBS sector to significantly underperform in the short term, which would likely negatively impact the IVR stock price and could potentially also result in a dividend reduction.

Summary: Buy IVR Now While It's Still on Sale

Despite the terrible long-term history of IVR, especially since the Covid crash of 2020 from which the stock price has never recovered, there is hope for the future for IVR investors. The best time to buy a stock, whether for income or capital gains, is when it is priced artificially low. The IVR stock has reached a price that is about 33% above its 52-week low reached in October, as seen on the 6-month price chart.

Seeking Alpha

Depending on what happens over the next few months regarding inflation, the future of interest rate cuts, and other Fed actions including the reduction of Treasury sales, the REIT sector may see a continued recovery in the second half of 2024. If that scenario plays out, IVR stock will appear relatively inexpensive now while offering a distribution yield of 18.5%.

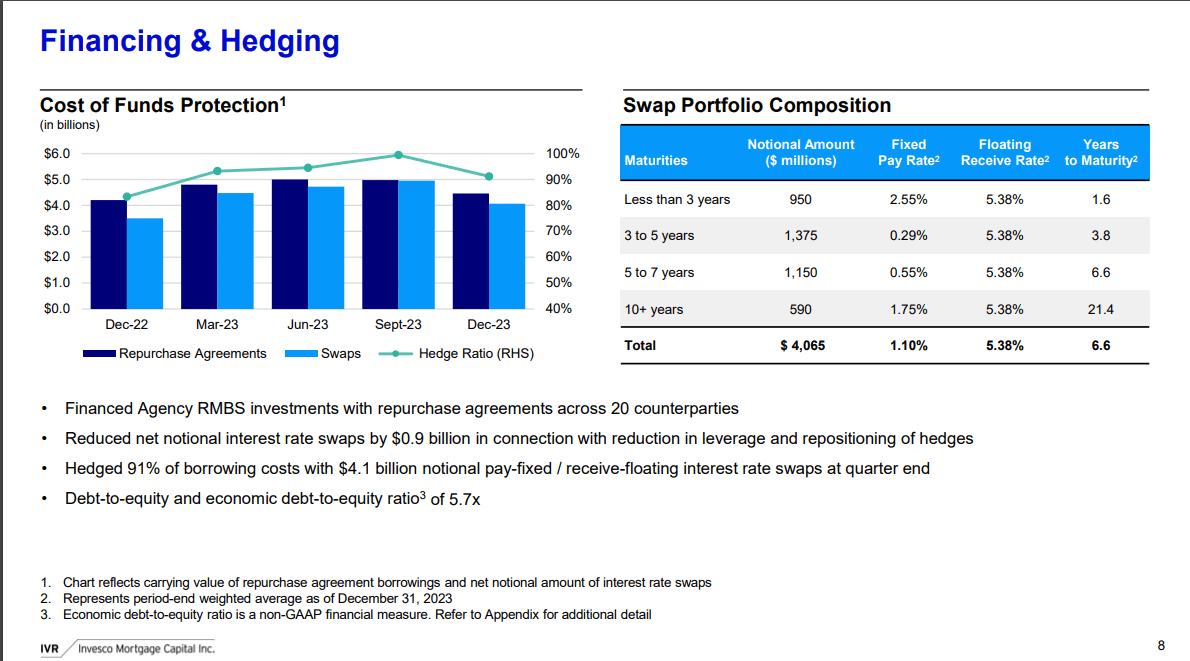

Invesco has been reducing the cost of capital and adjusting hedging positions over the past few quarters, as illustrated in this slide from the Q423 investor presentation.

Invesco Q423 presentation

As summed up by CIO Brian Norris on the Q4 earnings call, 2024 is shaping up to be an attractive opportunity for long-term investors in the MBS space and IVR is well positioned to take advantage:

Despite significant tightening of spreads in the asset class in the fourth quarter, we believe the Agency RMBS valuations remain attractive for long-term investors, given our expectations for the potential reduction in interest rate volatility over the course of 2024 as easing monetary policy likely results and a steeper yield curve.

Our preference for higher coupon specified pool should perform well in that environment. Further, our liquidity position remains robust. As a result, we believe IVR is well-positioned to navigate future mortgage market volatility and selectively capitalize on historically wide Agency RMBS spreads, which provides the supportive back drop for long term investment.

I agree with his assessment that IVR offers income investors especially an excellent opportunity to invest now at a low price to realize long-term income at attractive levels for patient investors. In the short term, there could be more price volatility, but the dividend is well covered, and the momentum appears to have shifted in the REIT sector based on Q1 results reported thus far. I expect that IVR will also deliver a positive Q1 earnings report in early May. I rate IVR a Buy ahead of earnings at a price below $9. I currently own shares of IVR in my Income Compounder portfolio.