The last week has been a fright fest for the gold "community". But these are the financial markets, not a community. There is a world outside of whatever is going on in gold and silver. A macro economic backdrop filled with entwined and correlated assets and markets all trying to form a message when taken as a whole.

Sure, gold - as a monetary metal - is a big one when it comes to macro indications, but what is really important is the great question that has been ping-ponged about for many years now between intellectuals on either side of the debate; inflation or deflation?

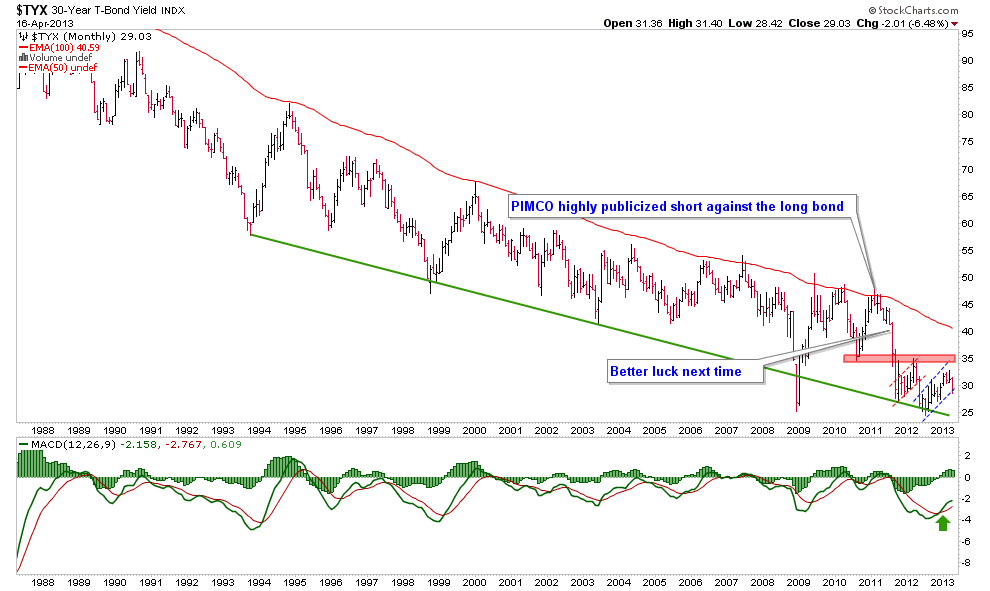

This post dials things out from the hysteria of the gold bear market (it is a savage cyclical bear, and we will certainly deal with it in a constructive way on the market's terms) to the big picture and the eternal debate between 'inflationists' and 'deflationists'. Really, as I have felt all along, we have inflation and we have deflation… all along the continuum, as illustrated by the monthly chart of the 30-year T bond yield.

30 year yield, monthly

The continuum of gently declining interest rates on long-term T bonds implies a deflationary backbone spanning decades. Against this firm disinflationary signal, policy makers have had license to print money at various times and with varying intensity. The MACD trigger on the chart above implies that a new inflation phase is trying to get started, but this is restrained by what looks like the second of two bear flags that have formed just below resistance at a 3.5% yield.

As long as rates remain below that resistance level, the deflation argument is alive and well. The last time the 'continuum' hit the red line (100 month exponential moving average), which has been the limiter of inflation expectations for decades, the second phase