In our opinion, Gregory Garrabrants displayed a rather distasteful sense of humor during the BOFI 2Q15 earnings call. When a KBW analyst inquired as to whether regulators had asked BofI Holding (BOFI) to tweak anything in its business model as part of the H&R Block (HRB) approval process, he had a rather odd response:

I have to say, Julianna, I'm going to give you like the award for that. I think my dad had a good sense of humor and he used to say - when you get a question like have you stopped beating your wife, you always have to stop and say, wait a minute, what was that question?

We find nothing humorous about domestic violence.

We are glad that sell-side analysts are beginning to ask the same questions we have been asking.

We did have one question for management coming out of the earnings call that we were unable to ask.

Why is BOFI not disclosing a lawsuit from 2012 that is going to jury trial in October of this year?

Given this case pertains to an acquisition of deposits and breach of contract, we think H&R Block shareholders would be particularly interested in the details of the lawsuit.

Two current and active lawsuits (links provided below) have been brought to our attention since our first article on BOFI. We encourage readers to digest the contents of the lawsuits on their own and form their own conclusions. We provide short summaries below.

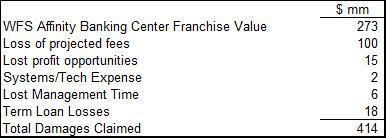

Undisclosed Lawsuit #1 - Breach of Contract Claim

BOFI is accused of breaching a contract with Waterfield Financial Services in connection with an acquisition of deposits.

We summarized the damages claimed in this case below:

Undisclosed Lawsuit #2 - Class Action Wiretapping Lawsuit

BOFI is accused of recording phone calls without the plaintiff's permission.

In its most recent 10-Q, under legal proceedings, BOFI states the following:

Item 1. Legal Proceedings:

"We are not involved in any material legal proceedings. From time to time we may be a party to a claim or litigation that arises in the ordinary course of business, such as claims to enforce liens, claims involving the origination and servicing of loans, and other issues related to the business of the Bank."

We reviewed BOFI's financial statements dating back to 2012 and found no mention of any active legal proceedings.

We have no view on the merits of the lawsuits. Given the nature of the lawsuits, we do not believe that they fall under the category of "ordinary course of business" lawsuits. We also note that the damages claimed in the breach of contract lawsuit appear to make up a significant proportion of BOFI's book value.

BOFI has also countersued, and the case appears to have been actively litigated for several years now. We therefore found it highly irregular that BOFI has never disclosed the existence of these lawsuits in its public filings, particularly given that the July 2012 case is set to go to jury trial in October 2015.

Most public companies that we follow provide ample disclosures regarding lawsuits of this magnitude. Details provided generally include the name of the case, the venue, a brief description of the case, and some commentary on the merits of the case. Therefore, the lack of any mention of these court cases surprised us.

Just look at H&R Block's filings to get a sense for what standard litigation disclosures look like.

We already covered the numerous questions we have about BOFI's disclosures in our last article:

BofI Holding: Will Regulators Strike?

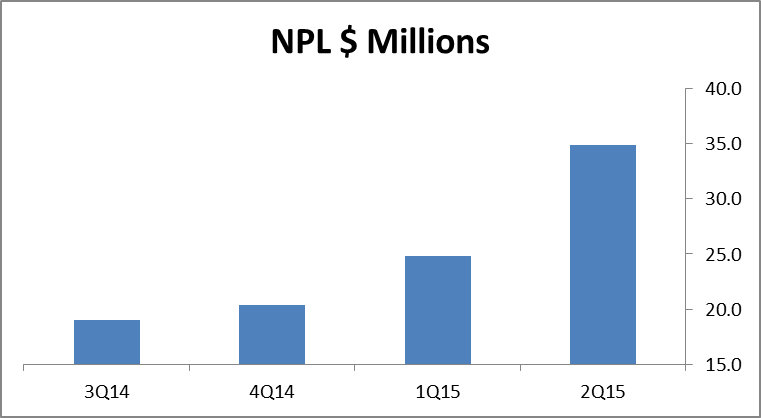

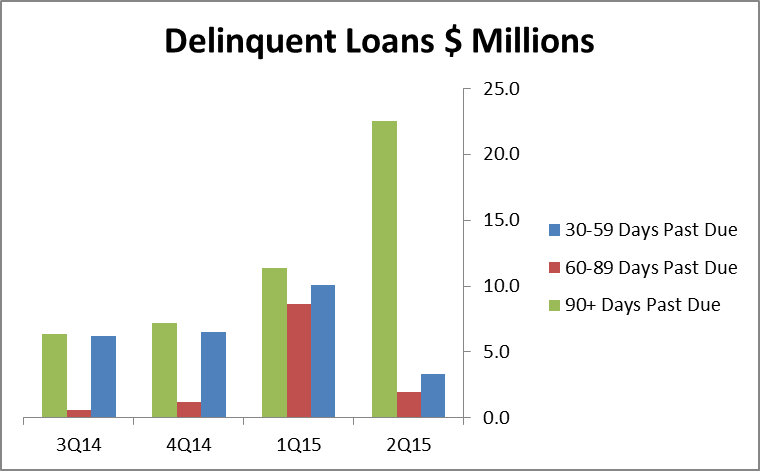

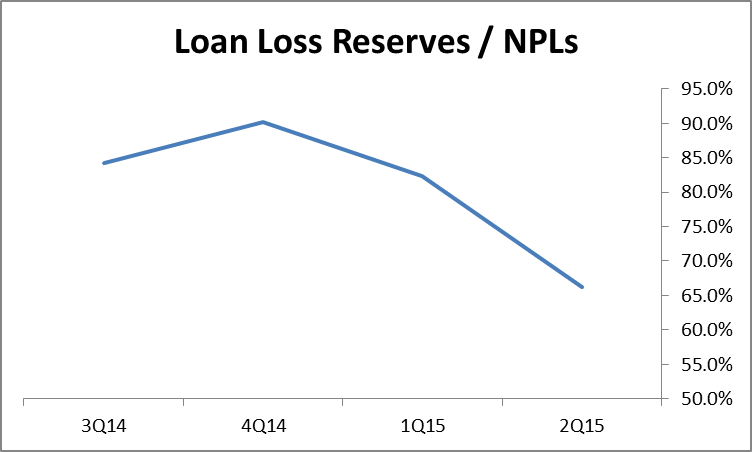

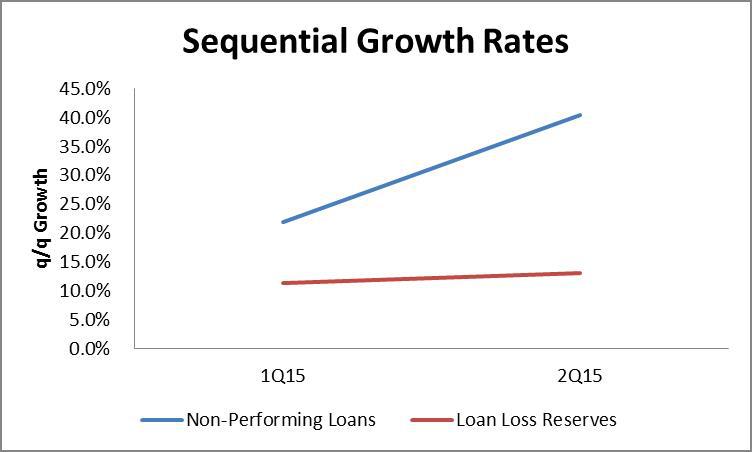

We were also surprised BOFI received no questions about its loan book performance on the earnings call. We note that non-performing and delinquent loan issues appear to be to manifesting themselves at BOFI, with NPLs / 90 day past due delinquent loans picking up rapidly sequentially. Despite these trends, BOFI yet again recorded an incredibly small allowance for loan loss provisions:

Given the uptick in NPLs, one would expect to see loan loss provisions grow commensurately with the NPL growth. We plotted out BOFI's allowance for loan losses against its NPL balance. For those less familiar with bank analysis, we looked at the size of BOFI's loan loss reserves in comparison to its non-performing loan balance. For a bank growing loans at a 50%+ pace, one would expect the allowance for loan losses to run at >100% of current NPLs in even the healthiest of banks in order to capture loan growth. We also plotted out the sequential growth in BOFI's allowance for loan losses against its NPL growth in the past two quarters. In our opinion, both metrics point to management under-reserving against future loan losses.

Other questions that we think should have been asked on the earnings call:

- What proportion of your loans are to foreign nationals? Given the recent appreciation of the USD, do you see any risk of an uptick in defaults in your foreign national loan portfolio given mortgage affordability has stepped down meaningfully for non-USD denominated home buyers?

- Based on your recent loan to Vapor Hub International (OTCPK:VHUB) (see loan agreement here), is BOFI now entering the penny stock lending business? How do you think about loss rates when you lend to these types of companies?

- How are the January 2014 changes to prepayment penalty rules impacting your business? Your refi/prepayments appear to be accelerating - is this a potential headwind to loan growth going forward?

Summary Thoughts

During the conference call, Garrabrants also took the unusual step of calling out short-sellers of his stock. He said that "short-sellers are trying to stem the pain they're going to feel by choosing poorly which shares they short".

Ultimately, short-sellers and long investors are looking for the same thing - transparency in order to conduct fundamental stock analysis. On the 2Q15 conference call, Mr. Garrabrants expressed clear frustration with the "short-sellers" of his stock.

Attacking the short-sellers will not alleviate these frustrations.

A simple solution to Mr. Garrabrants' frustrations would be for BOFI to provide investors with more color on: the contents of its loan book, its lending standards, why it finds its current loan loss provisions appropriate, and what regulatory risks it is taking in the process of underwriting its wide spread loans.

Garrabrants on the call also stated that "people have been able to write things that are untrue about us, and, really, I don't know how much effect they've had…I think mostly they've been disregarded for the drivel that they are".

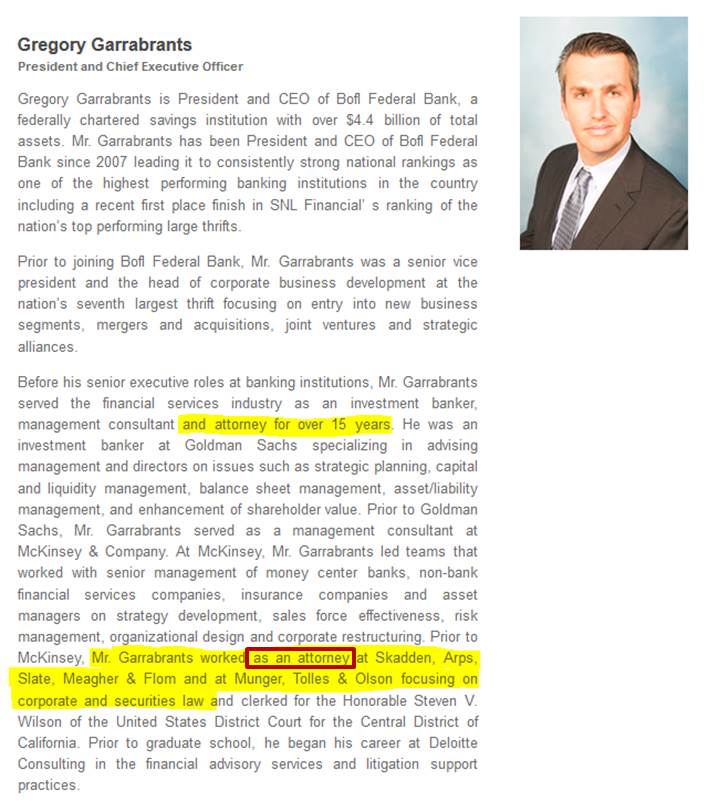

We see signs that Garrabrants himself has not disregarded our previous write-up as "drivel". We note that since our article was published, both he and the CFO have modified their official biographies.

One closing example:

Before:

After: