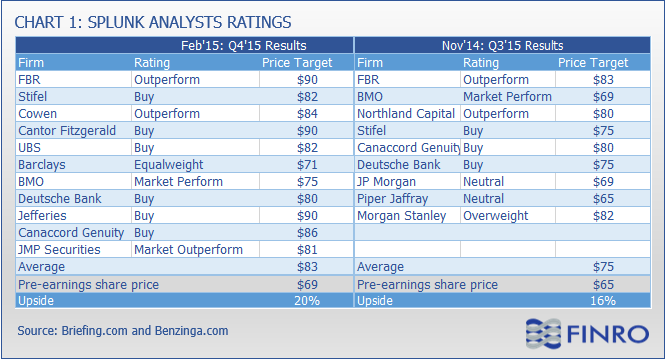

The big data analytics company Splunk (SPLK) reported its fourth quarter and full 2015 year (ended Jan 31, 2015) results last week with higher than expected revenues and EPS figures, and increased its full-year guidance for 2016 from $575M to $600. Shortly after the earnings release, Splunk's stock price soared more than 7% to $74.65 and completed a 40% rally in February alone. The next day, 11 research firms published their updated Splunk reports, providing an $83 average price target, and it seemed like Splunk was on the road to the $80s. However, as many Splunk investors feared, the stock dropped sharply to 15% from the $74 price peak, reminding them of the Q3 post-earnings sell-off.

The similarity is amazing between the market reaction to Splunk's Q4 and Q3 earnings. In November 2014, Splunk reported better than expected revenues and EPS for the third quarter, increased its full-year guidance, and received an analyst average price target of $75, which was 16% higher than the pre-earnings share price. From that point, Splunk's stock dropped 27% to $51 at the end of January 2015.

Right after the earnings, I sold some of my position at $75, realizing a 20% gain. I immediately thought of the article I published after the Q3 earnings, where I set a $75 share price as my next checkpoint and provided a $145M estimate for Q4 revenues. After the "I told you so" feeling faded, I started to think about my action plan for the Splunk position and how to benefit from the market reaction.

Once again, I want to mention something I pointed out in my earlier articles. I believe that the big data analytics market is headed upward as the flood of data increases, and I think Splunk, which is the biggest pure-play in big data analytics, is the right pick