As of this moment, I'm looking at hefty unrealized losses on an outsize position in International Business Machines (NYSE:IBM). In reviewing the situation, I evaluated the company by comparing it to the competitors listed on its most recent 10-K. This article presents the analysis and invites comment and criticism from readers.

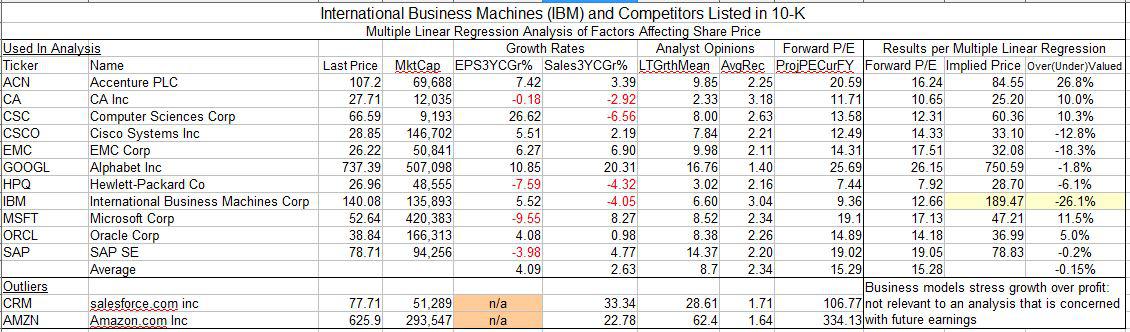

There is no data available for Dell, which is privately owned, and the data I used didn't contain information on Fujitsu. Aside from that, all major competitors are considered. I used Portfolio123 to develop the information, consisting of 3 year historical growth rates for EPS and Sales, together with average analyst estimates of long-term growth, average recommendations on a scale of 1 (strong buy) to 5 (sell) and forward P/E.

Feeding the information into online multiple linear regression (abbreviated MLR) software, I received a formula for forward P/E, derived from the other variables, and calculated values for that metric, based on the formula developed.

If IBM were valued on the same basis as its peers, forward P/E would be 12.7, rather than 9.4, resulting in a share price of $190. If it takes two years to reach that level, capital appreciation would be 16% per year, to which one can add the dividend, currently yielding 3.7%. The patient investor has a reasonable expectation of capital appreciation, and he will be paid to wait.

Transition

When reporting 3Q 2015 earnings, IBM saw revenues decrease 1% when adjusting for currency and divestitures. More importantly, year-to-date growth in strategic initiatives was 20% as reported, or 30% adjusted.

Management's stated goals for the strategic initiatives amount to a 12.5% annual increase, when going from $25 billion in 2014 to $40 billion in 2018. The transition is developing far more rapidly than projected.

I'm uncertain what to make of the speed at which the