As part of Mexico's privatization efforts, the country sold off most of its airports to the public. It put these into four airport groups, three of which are now publicly-traded.

For PRO and/or Ian's Insider Corner members, you can see my coverage of Aeroportuario del Sureste (ASR), notable for its Cancun airport, and Aeroportuario del Centro Norte (OMAB), whose most important holding is the Monterrey Airport.

In the time-honored tradition of saving the best for last, we'll now discuss Grupo Aeroportuario del Pacifico (NYSE:PAC), which has the most compelling mix of Mexican airports. Top holdings include Guadalajara, Tijuana, and tourism-focused Cabos and Puerto Vallarta.

As a reminder, I'm generally very bullish on airports, since they are natural monopoly businesses, and benefit from favorable long-term demographic trends. Barring unexpected events (huge jump in oil prices, major upswing in terrorism, global health pandemic), the global aviation industry should continue to grow at rates far faster than global population or GDP. Notably, between 2004 and 2014 - a time when oil prices hit airlines hard, global aviation revenues doubled.

And Mexico is a particularly inviting market. The domestic air industry is booming as low-cost carriers have pounced into the market since the financial crisis, offering fares competitive to long-distance buses. Combine with a growing Mexican middle-class and a demographic dividend that is now playing out, and Mexico's economy should support robust growth in travel volumes.

PAC: Why It's The Best Of The Three

The bull case for PAC starts simply. It is by far the most diversified of the three Mexican airport operators. Consider the top 10 busiest Mexican airports, and who owns them:

- #1 Mexico City (not publicly-traded)

- #2 Cancun - ASR

- #3 Guadalajara

- #4 Monterrey - OMAB

- #5 Tijuana

- #6 Los Cabos

- #7 Puerto Vallarta

- #8 Merida - ASR

- #9 Leon/Guanajuato

- #10 Culiacan - OMAB

As you can see, PAC operates five out of Mexico's top 10 airports. The other companies each only control two of the top 10 airports. And traffic has a long-tail; once you get out of the top 10, the remaining airports provide only marginal additions to your overall revenue base.

ASR would seem like the clear post-Trump pick. It runs Cancun, which is (by a wide margin) Mexico's #2 airport after the capital. Cancun surpassed 20 million passengers this year versus #3 Guadalajara, which crossed 10 million for the first time in 2016.

ASR's next biggest source of revenue isn't even from Mexico, but rather its JV stake in San Juan, Puerto Rico's airport. Thus, you're getting a highly concentrated tourism play with a Puerto Rican turnaround/recovery kicker.

That may work out fine, but as I commented previously, I'm wary of making a huge bet on Cancun. Look at what happened to former leading Mexican tourist spot Acapulco, for example. Things get overbuilt, crime rises, the cool crowd moves on to something still pristine, etc. Plus, the government would like for there to be another Mayan Riviera international airport built near Cancun that might divert significant traffic flows sooner or later.

Meanwhile, over at OMAB, you're getting a concentrated bet on Monterrey, which you could also call the city that NAFTA built. The metro area has doubled in size since 1990 as US manufacturers sent jobs south in search of cheap labor. Should that trend continue (I suspect it will, Trump huffing and puffing aside), OMAB is a great value at today's price. But there's not a lot of diversity to the company's airports beyond that. Its other properties tend to be US trade-reliant as well (Torreon, Reynosa, Ciudad Juarez, etc.) or be dangerous fading tourist destinations (Acapulco).

That leaves us with PAC, which offers a most intriguing mix of airports not heavily reliant on any one factor. The crown jewel is Guadalajara, Mexico's second largest city - comparably important to Mexico as Chicago is to the US.

Guadalajara is large enough to attract significant tourism flows merely due to its status as a large city (along with some specific attractions such as tequila tours). Guadalajara's metro area ranks it just behind Atlanta, but ahead of Boston and San Francisco to give some size perspective. The city places in the top 10 within Latin America in both size and GDP.

And Guadalajara sports a large modern economy with much more than just low-level industrial activities. It's a base for the IT industry, among other more educated and well-paid fields of labor.

After Guadalajara, we have Tijuana. While the city is on the US border, it's not all downside. The city has built deep links to San Diego. Speaking of San Diego, Tijuana is ideally positioned to take air traffic, as San Diego's airport is capacity-constrained (only has one runway) and Tijuana just built a direct entry to the US border-crossing bridge.![]()

Next up, PAC comes with not one but two tourism-heavy airports, both in safe and growing areas, Puerto Vallarta and Cabos. These are the premiere Mexican Pacific tourism spots, and could pick up additional traffic if Cancun ever loses a step.

Rounding out the top holdings, #9 Leon/Guanajuato is a dual-play airport, offering service to touristic Guanajuato, with its unique mining-themed attractions/geography, along with serving a booming nearby industrial area.

Guanajuato's passenger figure has doubled since 2011, and was the fastest-growing of any meaningful size in Mexico in 2015, making it an attractive upside option.

2016: A Banner Year

Guanajuato isn't the only airport growing quickly. Out of PAC's top-tier airports, all of them had great 2016s. Excluding PAC's Montego Bay, Jamaica airport, all its top 8 airports were up at least 13% on the year:

And, looking at the November data specifically, things remain strong. Admittedly, the tourism airports were off a bit (Cabos, in particular, got hit by a nasty hurricane earlier this year). But the twin pistons driving PAC remain firm, with Guadalajara up 17% on the month, and Tijuana still around 30%. Those two airports alone account for nearly half the group's traffic.

December traffic actually accelerated compared to November, despite being the first fully-post Trump month of data that we have. International tourism jumped several points, while domestic travel continued its slight slowdown of late. In total, it was sufficient for an overall traffic gain.

The tourism-centered airports should pick up further heading into 2017 due to the Trump-centered decline in the Mexican Peso. Current forecasts are bullish on Mexican tourism for 2017.

There are some headwinds, such as the Mexican government cutting tourism advertising as part of broader austerity. However, the weaker Peso fixes many ills, particularly relating to tourism. In addition, while the headline murder rate is up a bit as of late, there's been a sharp drop in kidnappings (-25% in 2015) and extortions. The government isn't winning the drug war decisively, but it appears to be holding its ground at least.

Trump Risk

Of course, no article on Mexico is complete without mentioning the elephant in the room. Some of PAC's airports are quite exposed to Trump (thankfully, not most of them).

Hermosillo, the company's #7 busiest airport, is near the border and relies on the automotive industry. Ford (F) helped kick off the outsourcing boom by building there prior to NAFTA in fact. Guanajuato could also face troubles in a Trump world. While the city itself relies on tourism and silver mining, the surrounding region is booming manufacturing center, and is advertising heavily (including in China) to attract more investors/plants.

Crown jewel Guadalajara is unlikely to be severely affected. It has a diverse and robust economy. It also garners significant tourism/international traffic. If Mexico's economy experiences a sharp contraction, Guadalajara would take a hit in line with the broader country. My current forecast (in line with Wells Fargo's (WFC) outlook) sees a modest 1% recession in 2017 with recovery coming in 2018.

Tijuana also could be effected. The city is heavily integrated into the San Diego economy, it'd be hard for many firms to pull out, even if Trump did his worst. That said, Tijuana has plenty of low-end manufacturing, a trade war would impact the city. It also serves as a jumping off point for many Mexican migrants who then proceed to travel overland into the US for job opportunities. This flow of traffic could be interrupted in the Trump future.

Why Tijuana Is Booming

On the plus side, Tijuana may develop more as a tourist airport. The newly opened Cross-Border Xpress bridge is a game-changer. If you were wondering why Tijuana grew so sharply in 2016, look no further. Tijuana's airport sits on land adjacent to the US border. A private firm built a bridge directly to US territory in San Diego; ticketed passengers can now land in Tijuana, walk within contained airport facilities to the US, and exit customs there. As it's marketed, the Tijuana terminal - in San Diego (website):

That already sounds good, once you consider that often hour+ lines at the traditional Tijuana/San Diego border, this becomes a massive opportunity. Adding cream on top, San Diego is one of the world's busiest one-runway airports, and as such, is badly capacity constrained.

The city has long needed a bigger airport, but local figures have dragged their feet. The tech industry there is begging for a new airport. In lieu of getting one, more and more traffic will start to utilize Tijuana now that it's easily accessible from San Diego proper. In 2016, Tijuana picked up international direct service from Asia on Aeroméxico, the first offering of its kind in the San Diego metro area. Direct US access from the airport greatly expands Tijuana's catchment area.

With the massively successful Volaris (VLRS) low-cost airline operating extensively out of Tijuana, look for it to try some innovative routes of the city now that it can also tap San Diego's market and that US-Mexican routing restrictions have just been relaxed.

Finally, again given capacity constraints at San Diego, there's a decent chance one or more airlines will start flying Tijuana-Los Angeles and Tijuana-San Francisco. Given the short distance and flight time involved, this could bulk-up Tijuana's passenger volumes greatly, and offer real possibilities toward making the city a hub with more connecting passengers (great for retail at the airport's shops).

As a reminder/note, if you like Tijuana in particular, make sure to consider Volaris stock as well, since it dominates that airport, and will certainly make hay if the growth story there continues. My most recent Volaris coverage can be found here.

New Routes

One of the big growth stories to PAC, over the longer-haul, will be the further integration of Mexico into North America. The two countries made a big jump toward that goal earlier this year. Here's the AP's take:

The United States and Mexico agreed in December [2015] to open their aviation markets to each other's carriers. Rules that had generally limited two or three airlines from each country to a particular route will go away.

Airlines on both sides of the border will be able to fly whatever routes they want as often as they want and set their own prices, said Thomas Engle, the State Department's deputy assistant secretary for transportation.

"This will help reduce airfares for sure," said George Hobica, founder of the travel site airfarewatchdog.com [...]

The agreement between the U.S. and Mexico does not relax limits on takeoffs and landings at Mexico City's busy main international airport. So the first new flights from U.S. carriers will focus on resort towns in Mexico.

These changes went into effect earlier this year. And their arrival spurred the launch of various new US-Mexico routes.

Even prior to this, Volaris had some pretty interesting international routes, flying to Oakland, Fresno, Reno, and San Antonio, among others. These aren't the sorts of top-tier international gateways travelers typically use when entering the US. Instead, Volaris is finding markets where it can make a low-frequency service aimed at tourists and family travelers in smaller markets.

On that note, Volaris recently announced new service to Milwaukee, which has a decent-sized Hispanic population, from Guadalajara. Previously, Milwaukee only had direct service to Cancun. PAC can see substantial upside if airlines such as Volaris start offering direct flights to Mexico from various mid-tier cities abroad. Previously, Mexico City dominated international arrivals, PAC stands to benefit greatly the more that passenger traffic diffuses rather than remaining concentrated in the capacity-constrained hub airport at the capital.

Mexican Aviation: A Huge Secular Growth Story

I could comment at length, but let me just show a few graphs instead. They make my point clearly. Anna.Aero has the data. Here's Mexican domestic travel:

As you can see, the Mexican domestic market generally grows at least 10%/annual clip during decent economic times. Yes, 2008 was a rough year, but it came after a sustained 20%+ growth period in 2007. Given the increasing prominence of multiple dirt cheap discount airlines, look for airlines to keep stealing traffic from buses (or expanding the travel market entirely) for a long time to come.

And internationally, the growth generally hasn't been as dramatic, but the trend is similar:

2015 was an exceedingly good year, particularly toward the back half. 2016 hasn't been quite as strong, but PAC's airports (more than the country as a whole) are performing well, and 2017 should maintain steady trend line growth as the fall in the Peso makes up for issues elsewhere.

To put a picture to PAC's tremendous growth, let's consider how passenger traffic has developed at its top two airports. Here's Guadalajara (2016 estimate is mine, assuming same 16% YTD growth rate):

That's the sort of nice exponential growth a long-term stockholder wants to see. Tijuana looks even nicer:

If you can buy a business with this sort of growth trajectory at a half-way decent starting valuation, good things are likely to happen. Particularly given PAC's structure, where the big costs are upfront, and each incremental passenger produces massive margins.

Valuation: How Much Upside?

PAC is currently trading around a 21 reported PE. So, if you just look at that, you might say it's not that cheap and move along. That'd be the wrong play. PAC is a very REIT-like structure. It owns real estate, collects rent, and pays the vast majority of profits out as dividends.

Valuing PAC on an EV/EBITDA basis provides a fairer picture. Unfortunately, there aren't all that many public comparisons, particularly in North America, where airport privatization hasn't taken off.

In Europe (see PWC's report here), large airports with slow traffic growth generally sell at 10-14x EBITDA, while regional airports with faster growth sell at 14x-18x EBITDA. In recent years, however, these ratios have spiked, with many transactions occurring above 20x EBITDA lately.

Until recently, PAC had been trading around 13-14x EV/EBITDA over the past couple years. With the Trump dump, PAC now sits at 8.7x EV/EBITDA.

Put another way, PAC is selling cheaper than even the lowest of growth overseas airports, despite having tremendous growth and a unique catalyst working in its favor at Tijuana. PAC's pristine balance sheet is also a plus. All that, of course, is weighted against Trump risk. The weak Peso has also held down the value of PAC stock for US owners, though it benefits the company by supporting tourism.

And, if I may be so bold, I'd suggest the market has badly undervalued PAC all along. Consider the stock traded at $30/share as recently as 2010, proceeding to run as much as 250% in six years. Given the company's massive growth rate, it seems silly that the stock was on average available at just 11x median EBITDA in recent years, and the market is now throwing away its shares at an even cheaper level today.

Consider how many businesses you know that trade at a single-digit EBITDA today, have a realistic chance of doubling that within 5-6 years, and whose core assets can grow revenues 13-18%/year with minimal capital expenditures. And with very low leverage, the business doesn't have creditors to worry about even if the Trump-induced downturn is worse than expected.

The Dividend

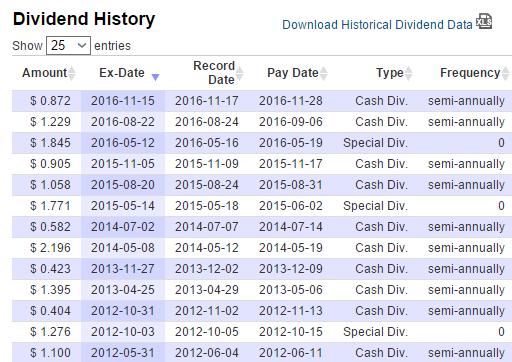

If that weren't nice enough, we must remember that PAC is a cash machine to shareholders. And the yield is misunderstood by many foreign investors, allowing it to stay under the radar and thus not get caught up in the chase for yield.

This is because PAC pays the majority of its profits out as dividends semi-annually. The dividend fluctuates, generally rising, and isn't fixed from year to year, as US companies are apt to do.

Seeking Alpha and other such financial sites now show PAC as yielding just 2.3%, since they count these two dividend payments, but miss the special dividend.

Remember that PAC is REIT-like. Earnings are understated, since the company has to expense things such as depreciation that don't matter to it on a cash basis. Thus PAC produces more cash flow than earnings would suggest. PAC has commitments related to the terms of its airport concessions, and is required to keep cash on hand in relation to those. The amount in excess of that can and is generally paid out as a special dividend annually. Here's PAC's dividend history since 2012 - note the meaty recurring special dividends:

In 2016, for example, PAC appeared to only pay $2 in dividends, if you add the normal semi-annual cash dividends together. Throw in the special dividend, and now you've got $4 of dividends, or a greater than 5% yield.

Given PAC's structure, it has a dividend that can grow explosively. Consider its history since going public (annual dividend per share data from here):

With the company regularly spitting out around $4/share in dividends, the company's yield has already more than doubled from what it was regularly producing less than a decade ago. And once the Mexican Peso starts to recover, the dividend grows even fatter for US holders.

At minimum, I'd argue that PAC should trade at 15x EV/EBITDA, and even that's probably low. Most airport transactions are going off above 20x EBITDA nowadays, and PAC has faster-growing airports than the comparable sales. Sure, discount Mexico to the degree you feel you need to, but PAC shouldn't be selling at less than half price to global airports just due to location and Trump risk.

Mexican airports are undervalued as a group, and PAC has the best assets of the bunch. 2017 could be choppy as Mexico probably hits a small recession, and Trump rhetoric rattles the market from time to time. But at the rate PAC is growing, and its starting single-digit EV/EBITDA ratio and 5% yield, you're getting a wide margin of safety.

This stock was cruising in the months leading up to the election; had Hillary won, I have no doubt it'd be trading at fresh all-time highs today. Give it 6-12 months for Trump fears to blow over, notch a few more quarters of 15% growth, and you'll see PAC stock top $120.

2017 Guidance & Outlook

Finally, it's worth considering PAC's 2017 guidance released earlier this week.

The company projects 9% traffic growth for the year. That'd be a significant decline from 2016's rate, but still plenty good given economic and political realities. Given the magnitude of the decline in PAC's stock, you'd need a far harsher slowdown to justify the market's reaction.

As it is, we'll see international traffic at least maintain 2016's growth rate, if not accelerate even further. Against that, the domestic market will slow down somewhat, though it should keep growing. The Mexican government's recent move to hike the price of gasoline sharply is another plus for the low-cost airlines in the price war against the bus lines, since airlines tend to pay for fuel in dollars and were suffering on competitiveness there.

PAC projects 2017 revenues to rise 14%. While traffic will be up just 9%, the company can pass through inflation to end users while also benefitting from growth in non-aeronautical services. There are near-term opportunities for the company to pick up more advertising revenues, for example.

Additionally, PAC projects 11% EBITDA growth for the year. Remember, the company is already in the single digits on an EV/EBITDA basis - which is extremely cheap for an airport holding company. And that EBITDA figure is still likely to rise double digits during an off year. It's hard to overstate the power of PAC's growth engine.

Come for the 5% dividend yield, stay for the huge growth. Trump fears have put this excellent airport operator on deep discount. Once Trump fears start to simmer down and investors get back to looking at the company's blistering growth figures, shares will rebound sharply.