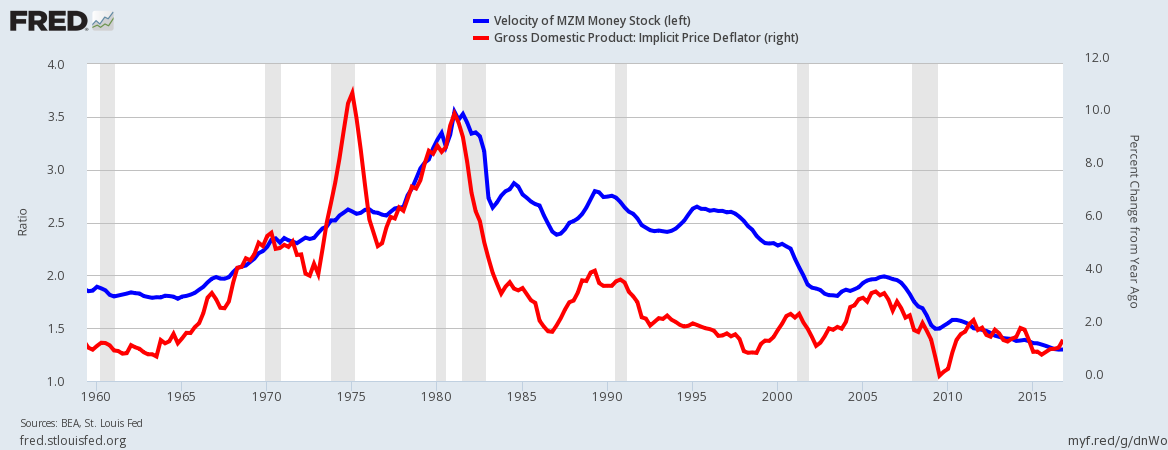

It is hard to get worked up about velocity of money. Sometimes it is rising going into a recession, sometimes it is falling. One general truth is that it has been slowing since the early 1980s.

The velocity of money has become a metric with little predictability for other economic metrics. A relevant post from the St. Louis Fed stated in part:

... during the prerecession period, for every 1 percentage point decrease in 10-year Treasury note interest rates, the velocity of the monetary base decreased 0.17 points, based on a linear regression model of the velocity onto interest rates. Since 10-year interest rates declined by about 0.5 percentage points between 2008 and 2013, the velocity of the monetary base should have decreased by about 0.085 points. But the actual velocity has gone down by 5.85 points, 69 times larger than predicted. This happened because the nominal interest rate on short-term bonds has declined essentially to zero, and, in this case, the best form of risk-free liquid asset is no longer the short-term government bonds, but money.

Of course there are general correlations - such as its relationship to inflation.

Even considering inflation, the correlations are far from perfect. But it is interesting to me that the trillions of dollars of quantitative easing had little apparent affect on the rate of decline in the velocity of money.

Is it possible that the distribution of wealth and income affect velocity of money? Logic dictates that the upper strata of wealth spends a far less percent of their income. And thus the more the inequality of wealth and income presents, the slower the velocity of money. From The Economist:

Is it just a coincidence the velocity of money slows at the same time wealth inequality is growing? And, at the same time, income inequality began