Shares of Tetraphase Pharmaceuticals (TTPH) have fallen by nearly 5% since my last update piece. However, the stock at one point doubled since I nominated it as a top comeback candidate for 2017 and is still in the green by around 50%.

TTPH data by YCharts

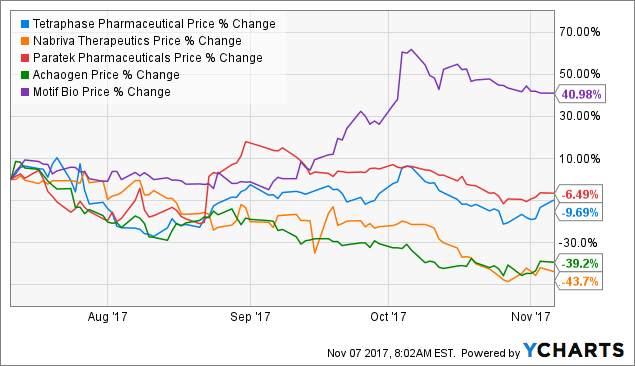

TTPH data by YChartsIn the most recent update, I noted that the stock became much more appealing now that the risk of dilution had been taken off the table. The company priced a 10 million share secondary offering at $6.50, which added to its second quarter cash balance of $118.2 million should allow for funding operations into early 2019.

In mid-August, the company reported that its Marketing Authorization Application (MAA) for IV eravacycline for the treatment of complicated intra-abdominal infections (cIAI) had been submitted to and validated by the European Medicines Agency. It was announced that enrollment had completed for the IGNITE3 study evaluating the efficacy and safety of once-daily intravenous (IV) eravacycline compared to ertapenem in complicated urinary tract infections (cUTI), with top-line data expected in the first quarter of 2018. If data is positive, management will be submitting a supplemental NDA to the FDA.

I reminded readers that if approved eravacycline could see significant adoption in treating high-risk patients, such as those with confirmed resistant pathogens, renal or hepatic impairment, or have failed first-line therapy. If readers believed that the drug candidate could do at least $500 million in annual sales at peak, then the current valuation appeared quite appealing.

The game-changer for me was the presentation of data at IDWeek 2017 from the Phase 1 study designed to optimize drug exposure of oral eravacycline in an IV-to-oral dosing regimen. Chief Medical Officer Patrick Horn stated that the timing of oral dosing in relation to meals led to lower drug exposures in the failed IGNITE2 study.

However, results from subsequent studies showed that increasing the interval between meals and dosing as well as administering a 250mg oral dose of the drug candidate is producing sufficient drug exposure to achieve the desired therapeutic effect. Drug exposure for the oral dose was 81% of that achieved with IV dosing (double that observed in the IGNITE2 study).

Now the company plans to enroll cUTI patients in a Phase 2 study in the first half of next year. Given the fact that the stock price was above $40 prior to the failure of the IGNITE2 pivotal IV-to-oral study in cUTI, I see quite a bit of upside ahead.

For the third quarter, the company reported cash and equivalents of $161.4 million, while net loss amounted to $30 million. Management has guided for an operational runway into early 2019, but I imagine further dilution is possible in the second half of 2018.

As mentioned above, key near to medium-term catalysts include the following:

- Possible approval in the EU for eravacycline in cIAI.

- Submission of their NDA to the FDA in the first quarter of 2018.

- Top line data from the pivotal IGNITE 3 study in the first quarter of 2018 (IV eravacycline in cUTI).

- Updates on the progression of the optimized IV-to-oral regimen in a mid-stage study in cUTI in the first half of the year.

I also note that well-regarded H.C. Wainwright analyst Ed Arce recently raised his price target on shares to $17. Several institutional investors I keep tabs on, including Tekla Capital Management and Ecor1 Capital, hold positions. Management will be presenting at the Stifel 2017 Healthcare Conference on November 14th and the Piper Jaffray 29th Annual Healthcare Conference on November 19th.

Tetraphase Pharmaceuticals Is A Buy.

Readers who have done their due diligence and are interested in the story should make a pilot purchase in the near term. Investors wishing to add to their positions should do so methodically over the next month or two. In the event of positive developments in the near term or a run-up into IGNITE3 data, readers are encouraged to take partial profits to take risk off the table while retaining additional upside exposure to this promising antibiotic play.

I will be adding this ticker back on the ROTY Contenders List to keep a closer eye on it.

The main risk at this point is disappointing data from the IGNITE3 study. Setbacks with regulatory submissions or failure to get eravacycline approved would be a major blow to the bull thesis as well. Delays with initiating the IV-to-oral study would not be welcome by shareholders. Risk of dilution in the near term appears off the table due to the recent secondary offering. Intense competition in the antibiotic space should be taken into consideration as well, because even if eravacycline is approved, commercial success is not a given.

Another con I want to point out is that several antibiotic plays continue to show depressing price action and downward trends in their respective stock prices despite positive data. Stocks I was expecting bigger moves from, such as Motif Bio (NASDAQ:MTFB), also disappointed me with muted moves to the upside relative to my expectations.

TTPH data by YCharts

TTPH data by YChartsAuthor's note: My goal is to bring to readers' attention to undervalued stocks with catalysts that could propel shares higher, as well as provide a fresh perspective on stocks you may already be aware of. I also touch on planning trades and risk management, as those are two areas I feel are often neglected. If you found value in the above article, consider clicking the orange "Follow" button and getting email alerts to receive my latest content. My sincere appreciation for readers who add value and join the discussion in the comments section, as well as those who share my work with others who could benefit from it.

Disclaimer: Commentary presented is not individualized investment advice. Opinions offered here are not personalized recommendations. Readers are expected to do their own due diligence or consult an investment professional if needed prior to making trades. Strategies discussed should not be mistaken for recommendations, and past performance may not be indicative of future results. Although I do my best to present factual research, I do not in any way guarantee the accuracy of the information I post. Investing in common stock can result in partial or total loss of capital. In other words, readers are expected to (and encouraged) form their own trading plan, do their own research and take responsibility for their own actions. If they are not able or willing to do so, better to buy index funds or find a thoroughly vetted fee-only financial advisor to handle your account. Additionally, I'm in collaborative relationship with The Biotech Forum/Bret Jensen.