Lithium Mining Salt Flats

Source: Apex

The lithium triangle above encompasses much of the known world supply. It is a critically important region for supplying the growing demand part of the lithium equation by a battery-hungry world. Here, salt flats straddle three countries: Chile, Bolivia, and Argentina. This area is essential for the lithium demand component discussed in the first article in this series because it feeds the world's growing hunger for lithium that is expected to continue for years.

The Atacama Salar

Atacama Salar de Chile

Sociedad Quimica y Minera de Chile (NYSE:SQM) is a well-placed giant in the Atacama Salar de Chile, part of South America's lithium triangle. SQM is the largest lithium producer in the world and the primary focus of this third article in the series.

The Atacama de Salar region in Chile currently produces one-third of the world's supply of lithium from two mining and export producers, SQM and Albemarle (ALB). The latter producer was reviewed in the second article in the series.

Northern Chile's topography, arid climate, and rich lithium source make it one of the world's largest productive containments. The term giant is not used lightly as indicated below.

Marcelo A. Awad, Executive Director, Wealth Chile stated that, "Chile produced the second-highest amount of lithium globally in 2014." Chilean mines feature the largest confirmed lithium reserves at over 7,500,000 MT. The Atacama Salar in Chile produces the highest grade lithium brine in the world."

Additionally, SQM maintains other current lithium mining projects in Argentina and Australia.

Can Supply Meet Growing Demand

Once, the debate question was, is there enough lithium to power mobile devices like laptops, phones and power tools? But now, the big question is can the future demand for lithium battery power be met?

Joe Lowry, an expert on the lightest metal, expects demand to nearly triple by 2025. Supply is lagging, which has pushed up the price. Annual contract prices for lithium carbonate and lithium hydroxide doubled in 2017, according to Industrial Minerals, a journal. This is attracting investors to the "lithium triangle."

Regional Domination

Without question, Chile enjoys regional domination among global lithium markets, and this has given SQM a premier position in the market. The mineral-rich brines provide high-quality proven reserves the markets seek. That and a friendly investment environment, proximity to ports, and the cheapest production costs have created a massive global supply source that is widely coveted.

The chart below for 2016 reflects SQM dominance that surpasses other countries in foreign investments. Australia also produces considerable lithium. However, it must refine it from ore, a more costly process. Perhaps this accounts for less foreign investment there.

Bear in mind that Argentina and Bolivia have resources equal to Chile, but at present, they lag behind in investment. But it is fair to say that Argentina is hastening to gain ground. Collectively, these three countries "account for 75% of the world's known reserves of lithium. Expect foreign investment and a friendlier business environment there as demand continues to ramp up and the perception of foreign corruption diminishes.

Regulations

In spite of Chile's leading position, there are laws that control lithium production, ostensibly, to protect a fragile ecosystem.

CORFO is the Chilean development agency that regulates lithium mining. SQM recently engaged in arbitration proceedings with CORFO concerning its failure to comply with obligations in their lease agreement. During the interim period, negotiations with CORFU received extensive press coverage that clearly spooked many investors creating a disincentive that may have cooled investor demand for shares.

On January 17, 2018, the long dispute ended when CORFO struck a deal that required SQM to increase royalty payments for mining in the Salar de Atacama. On the positive side, CORFO agreed to significant increases in production quotas. For more detail concerning the dispute and subsequent negotiations, please go to the following source.

The higher royalty payments for lithium carbonate are 40% for prices above US$ 10,000 per MT. This adds to production costs, and investors must watch to determine if greater production can absorb the additional cost without negatively affecting stock valuations. Growing revenue and earnings are major company variables to watch through 2021.

SQM First Quarter 2018 Results

On May 24, 2018, SQM reported earnings of US$ 113.8 equal to US$ 0.43 per ADR. It missed a Q1 earnings estimate of US$ 0.46.

It is noteworthy that Q2 2018 earnings are now estimated at US$ 0.48 suggesting an expectation of greater lithium production and higher earnings.

Revenues increased marginally and showed a slight increase of 0.03% year to year coming in at US$ 518.7 million.

Stock Valuation Peaked

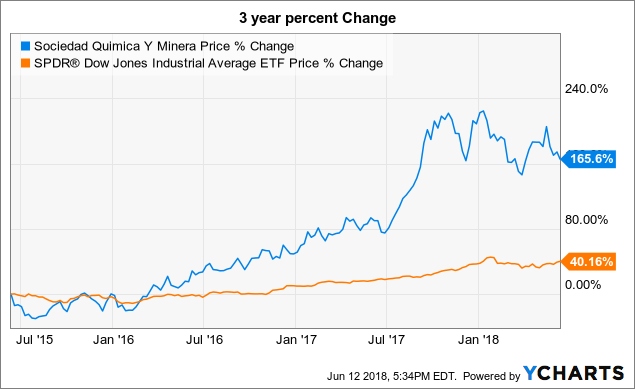

SQM 3 Year Growth Compared to SPDR

SQM data by YCharts

SQM data by YCharts SQM data by YCharts

SQM data by YCharts

A 3-year SQM growth pattern since 2015 double peaked by the end of 2017. Growth is similar to the Dow Jones ETF, which peaked and also fell off.

This year, SQM has floundered in a consolidation pattern never reaching its previous high water mark.

Six-Month Weekly Chart

Source: bigcharts Stock Charts

A 6-month weekly chart shows the slow stochastic attracted buyers this year selling off each time. Recently, it turned the corner from oversold and is now at a midline 50% position.

Investors continue to weigh the demand side of the equation with some recent headwinds that SQM has had to deal with. The news is fluid, and the balance may easily shift in SQM's favor.

The Good News

Settling this dispute has opened the door to considerably greater lithium production through 2021, and doing so is consistent with the company's awareness of growing global demand.

The global demand for lithium has encouraged a three-stage company capital investment of more than half a billion dollars over the next 4 years. Lithium production is expected to increase from 48,000 MT to 180,000 MT.

CEO, Patricio Solminihac reported that:

"Demand continues to grow at record rates and total market demand should be over 20% in 2018. Average prices during the first three months of this year surpassed 16,000/MT given a tight supply and demand balance. We believe that this price pressure will continue throughout the first half of the year."

The following bulleted points summarize current developments the company is working on to meet growing world demand.

- In Chile, the goal is to expand production from 48,000 to 70,000 MT with a total capex of US$ 75 million. The additional 22,000 MT is expected to be operational by the end of 2018.

- Expansion in the Salar de Atacama during the next 18 months will increase lithium production from 70,000 MT to 120,000 MT by investing US$ 200 million.

- By 2021, completion of the last stage will increase production from 120,000 MT to 180,000 MT with a US$ 250 million investment.

Takeaway

Concerns influencing stock markets ebb and flow over time, but I believe we are looking at a paradigm shift that will require some years to evolve. The tidal wave of demand for battery power is growing as part of changes issuing in this young century. They will include electrically powering millions of vehicles and other devices, and they will be with us for some time.

Batteries are already getting bigger. Tesla (TSLA) recently produced the world's largest 129 megawatt lithium battery that is capable of providing the power requirements of a city in Southern Australia.

World's largest Lithium Battery

Source: Reuters

Elon Musk's crown is on the line as South Korea's Hyundai Electric is building a 150 megawatt battery near Ulsan, a city in southeast South Korea.

In fact, in the race for "lithium battery supremacy," South Korea appears poised to take the lead in production.

This revolution moving the world to greater electrical power is well underway. It is early time, but the big lithium producers are well established. They are located where the greatest concentrations of lithium reserves abound. They will lead in providing the numerous metric tons of lithium needed. In my opinion, SQM is poised to be a big player.

There is a window of opportunity here that extends well into 2025. And, better still, share values have declined.

Don't miss the coming final article in the series that covers FMC Corporation (FMC). And please stay tuned and put the four-article series together and make up your own minds.

Author Disclosure: The information and data that comprise this article came from external sources that I consider reliable, but they were not independently verified for accuracy. Points of view are my considered opinions, not investment advice. I bear no responsibility for investment decisions you decide to make.