Business Overview

Destination XL (NASDAQ:DXLG) is a specialty retailer focused on Big & Tall consumers (B&T). The company operates 339 retail and outlet stores that are located in the continental US, with the exception of two stores in Toronto, Canada, and one in London, England.

DXL sells apparel through several different retail stores, including Destination XL, Casual Male XL, Rochester Clothing, Shoes XL, and Living XL. A third of the company’s stores are Casual Male XL stores, which are in the process of being rebranded as DXL stores. DXL also sells merchandise through Amazon, Walmart.com, and other third-party retailers.

Destination XL shares trade in the US under the ticker “DXLG”. Valuation metrics cited in this report are consistent with a share price of $2.20 as of 8/27/18.

Financial overview (all $ amounts are in thousands)

Market cap | 105,500 |

Debt | 70,286 |

Cash | 6,994 |

Enterprise Value | 168,792 |

(Source: Capital IQ)

Competitors/Other Sources of Big & Tall Clothing

The following is a list of specialty and general retailers that sell B&T clothing:

Destination XL (destinationxl.com)

King Size Direct (kingsizedirect.com)

ASOS Plus (us.asos.com)

Walmart Big & Tall* (walmart.com)

Amazon Big & Tall* (amazon.com)

Macy’s Big & Tall (macys.com)

Old Navy Big & Tall (oldnavy.com)

Kohl’s Big & Tall (kohls.com)

JC Penney Big & Tall (jcpenney.com)

Men’s Wearhouse (menswearhouse.com)

*Destination XL is a seller on Amazon and Walmart's third-party marketplaces, which mitigates the competitive threat to some degree from these two retailers. DXL has over 10,000 products available on Amazon, and close to 1,000 on Walmart. Products sold by DXL comprise around 10-15% of the B&T clothing available on Amazon, per my research.

Web Traffic Comparison

Page Visits* | |

King Size Direct | 1.06 million |

Destination XL | 1.16 million |

*Average monthly site visits over the last 16 months. Data from SimilarWeb.

Destination XL's primary competitor appears to be KingSizeDirect, another online specialty retailer targeted at B&T consumers.

It’s instructive to note that DXL’s product selection appears to be more high-end than that of KingSizeDirect. Brands such as Calvin Klein and Ralph Lauren are sold by DXL but are unavailable through KingSize. DXL also appears to face very little competition when it comes to brick & mortar stores, a positive for investors.

Size of Market

“If you are 6'2" or taller and/or weigh at least 225 pounds, then you are one of 13 million men in the United States - or nearly 1 in 5 - who make a perfect fit with KINGSIZE.” – according to kingsizedirect.com.

I reviewed data from the U.S. Census Bureau and believe the above statistic to be reasonably accurate. In addition, according to the Bureau of Labor Statistics, the average American household size is 2.58 people (as of findings from 2010) and the average American family spends $1,700 annually on clothing. This means that the average American spends $659 on clothes per year.

13 million men who are “XL” x $659 in average annual spending on clothes = $8.57 billion = maximum potential size of market.

Men IDXL* | Market Size | DXL’s share |

25% | $2.14 billion | 21.96% |

50% | $4.29 billion | 10.96% |

75% | $6.43 billion | 7.3% |

100% | $8.57 billion | 5.5% |

*IDXL refers to the percentage of the 13 million men referenced above who are potential DXL customers. I included this chart because it is reasonable to believe that not all men who are “6'2" or taller and/or weigh at least 225 pounds” are potential DXL customers.

For example, a slim 6’2” man could likely fit a L or XL, which are available at most non-specialty retailers. While these projections are very large-scale, broad estimates, they indicate that DXL has room for customer acquisition and increased store traffic.

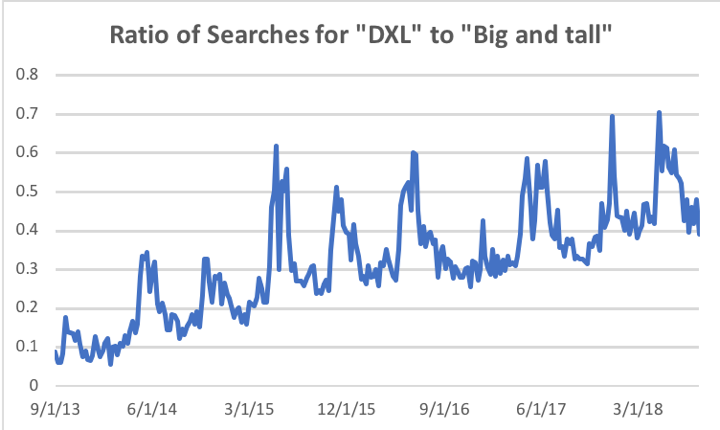

Google Trends Data

The above graph represents the ratio of Google search interest for “DXL” to search interest for “big and tall” over the past five years in the United States. The upward trend in this chart indicates that DXL has been gaining mindshare among B&T consumers. The original results are below:

(Source: Google Trends)

(Source: Google Trends)

I included this information because if DXL can be to “Big & Tall” what Foot Locker (FL) is to athletic shoes, then the company will be able to sustain top-line growth and achieve profitability. The uptrend on the first chart is a positive indicator that DXL is on a path to do so.

Industry Comps and Valuation

The following charts provide a comparison of valuation metrics between Destination XL and other apparel retailers:

EV/EBITDA | Gross Margin* | SG&A Costs* | |

Destination XL | 9.9 | 45.6% | 41.3% |

JC Penney | 4.7 | 33.9% | 30.6% |

Abercrombie | 5.4 | 61.2% | 58.7% |

Foot Locker | 5.0 | 33.1% | 19.6% |

Zumiez | 8.3 | 34.2% | 27.3% |

Tailored Brands | 6.5 | 42.7% | 32.5% |

*Average over the past five fiscal years.

(Source: Data taken from each company's respective SEC filings; valuation metrics are calculated by the author)

Destination XL’s gross margins are second-highest in its peer group, whereas its SG&A costs as a percentage of net sales are second-last. This bespeaks significant operational underperformance and indicates that there is room for management to reduce costs and carve out a road to profitability.

In addition, the fact that new store build-outs are largely complete means that management should be able to reduce capital expenditures and use free cash flow to pay down debt obligations. FCF (excluding changes in working capital) has been improving over the past few years, per the below chart:

Cash flow (in thousands) | FY 2013 | FY 2014 | FY 2015 | FY 2016 | FY 2017 |

Operating CF ex. WC | 7,188 | 13,793 | 21,605 | 28,939 | 14,954 |

Capital expenditures | 54,125 | 40,927 | 33,447 | 29,239 | 22,565 |

FCF ex. WC | -46,937 | -27,134 | -11,842 | -300 | -7,611 |

SG&A as % of Net Sales | |

FY 2013 | 43.74% |

FY 2014 | 42.22% |

FY 2015 | 40.83% |

FY 2016 | 38.49% |

FY 2017 | 41.29% |

Q1 2018 | 41.34% |

(Source: DXL's 10-K report)

Reducing SG&A expenses to 2016 levels would allow the company to break even on an operating basis. In addition, DXL is profitable when one looks at EBITDA, since depreciation & amortization expenses for the company are somewhat higher relative to those of its peers.

According to DXL’s most recent 10-K, “with our new store growth complete, we expect that our depreciation levels will begin to decrease beginning in fiscal 2018.”

DXL Revenue (all $ amounts are in millions)

Sales | YoY Growth | |

FY 2014 | $414.0 | 7.1% |

FY 2015 | $442.2 | 6.8% |

FY 2016 | $450.3 | 1.8% |

FY 2017 | $467.7 | 3.9% |

Q1 2018 | $113.3 | 5.3% |

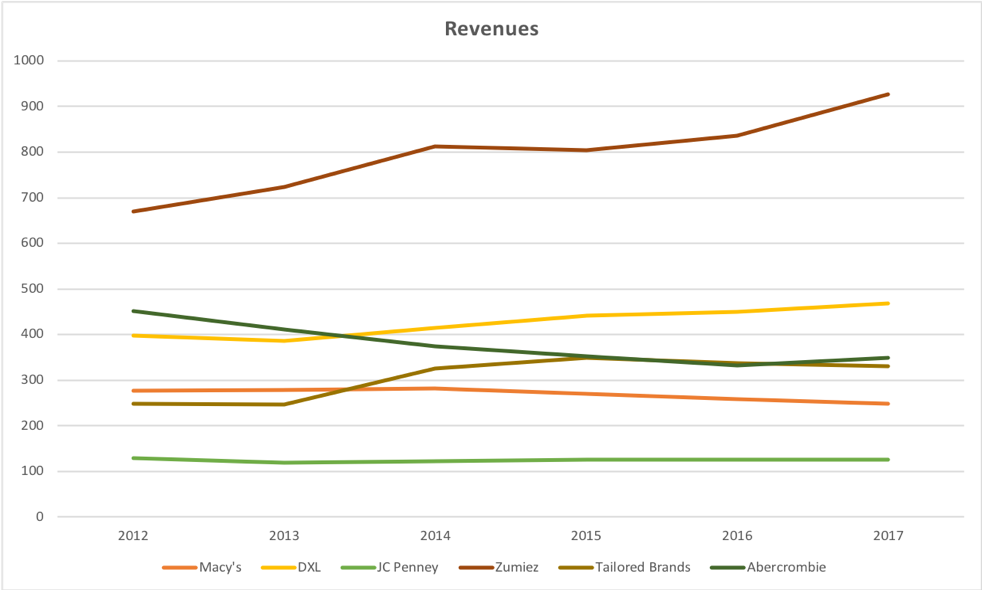

Below is an industry comparison of sales trends:

(Source: Capital IQ)

Note that DXL, Tailored Brands, and Zumiez are the only companies out of the six who have managed to maintain revenue growth over the past five years (chart is scaled for relative comparison purposes).

Investment Concerns

- DXL faces competition from a variety of players online, from large department store chains like Macy’s (M) and online-only retailers like King Size Direct.

- Whether management will be able to successfully reduce costs without hurting top-line performance remains to be seen. If it is unable to do so, share price deterioration is likely to continue.

- Big & tall men may choose, for the sake of convenience or some other reason(s), to purchase clothes at B&T sections of department stores instead of shopping at stores like DXL that cater directly to this segment.

- DXL’s market is constrained by the fact that for a man to shop at DXL, he must consciously identify as B&T; in other words, some men who wear XL+ size clothing may not perceive themselves as B&T.

- By catering and marketing primarily to men, DXL may be missing out on sales to women who shop for their spouses, relatives, etc.

- One of DXL’s strengths is that it is the only retailer with a nationwide presence that is focused exclusively on the B&T niche. However, Macy’s and other department stores chains could decide to increase their B&T sales efforts, which could adversely affect DXL’s business. The below image is the B&T section of a local J.C. Penney (JCP):

Investment Positives

- Management seems cognizant of the need to reduce costs and appears to be taking incremental steps to do so. SG&A expenses were down slightly year/year from 42.9% to 40.2% for fiscal Q1 2018, an encouraging result. Note that this was the first time in five quarters that SG&A expenses declined by more than 100 basis points on a year/year basis.

- If management is able to continue reducing costs, there is significant potential for share price appreciation. I am cautiously optimistic that the company will be able to do so given management’s spoken commitment to cost reduction and the fact that current expense levels appear unreasonably high for a company whose gross margins are solid.

- DXL holds a dominant position in the B&T market, particularly when it comes to brick & mortar stores.

- Casual Male-branded stores comprise a third of DXL locations and are being slowly converted to DXL-branded locations. This presents an opportunity for DXL to increase brand awareness and customer retention by marketing DXL as the premier, one-stop source for all things B&T.

- Management has noted in the 10-K that the company will be more focused on DTC efforts and “customer acquisition, customer retention and customer re-activation” now that retail store build-out efforts are largely complete. This may translate to greater sales and operational efficiency if management executes successfully.

- As referenced above, now that new store build-outs are largely complete, management should be able to focus on operational efficiency and customer retention. This is particularly important because 6 out of 10 B&T men are unaware that DXL exists (according to a Nielsen study cited in an investor presentation) and 93% of transactions take place through the company’s rewards program, indicating strong brand loyalty.

I’d like to add that recent bottom-line struggles are attributable in part to increased spending on marketing and advertising efforts. Such expenditures may be painful in the short-run but are important to drive brand awareness and customer retention. Per DXL's Q4 2016 earnings call:

“Every customer that we get to walk in the store it's a win. They come in, they enjoy the experience and we own them. The cost of acquisition of that customer is expensive, but the good news is that the money we're investing today has long-term positive profitability to it, because we have a good stickiness to this marketing. We get him in this year and we spend the money, we’re going to own that guy for the next four or five years.”

Insights from Store Visits

I recently visited a DXL store and spent around 45 minutes speaking to a sales associate. Here are some of the takeaways from my visit:

- Associates and employees were friendly, professional, and were very knowledgeable about sizing, fit, and other points of interest to B&T consumers. This was consistent with the training process for sales associates as described in the 10-K, which appears to be quite intensive and intended to ensure that associates are engaging, informative, and knowledgeable about everything B&T.

- The store was spacious and well-organized: different sections of the store were focused on various types of clothing, from casual to formal styles.

- Product selection was very broad: there were tuxedo rentals, suits and ties, casual apparel, athletic apparel, and both formal and athletic shoes.

- According to Alex, products from DXL’s private label brands strongly outsell products from third-party manufacturers like Calvin Klein and Ralph Lauren. Margins on private label products are higher than those from third-party manufacturers, which is a positive for the business if this result holds true for all DXL locations.

- While product selection was solid, there was a lack of more “hip”, urban wear. Take a look at the selection of ASOS Plus, versus that of DXL. You’ll notice that ASOS has more apparel that is geared to a younger, more “urban” consumer.

I also visited a Casual Male XL store and spoke to another associate there. The following are a few notes from my visit:

- The store was filled primarily with products from DXL’s private label brands. The associate told me that Harbor Bay, True Nation, and GS are the company’s most popular private-label brands. Apparel was very moderately-priced and lower-end than that of the DXL store I visited.

- The DXL store was superior in terms of product selection, quality of employees, and size/atmosphere of the store.

- If my observations are reflective of all Casual Male XL stores, DXL will benefit from the ongoing transformation of Casual Male XL stores to DXL stores. The associate I spoke with confirmed that Casual Male stores are in the process of being phased out.

I also poked around other department stores and found that:

- Macy’s does not have a dedicated section in its stores for B&T consumers; instead, an associate told me that some brands have XL+ sizes available.

- J.C. Penney does have a section in-store dedicated to B&T customers; however, the one I visited was rather small and comprised of lower-end material.

Marketing

This video was published in September 2016 and represents a great example of what I think DXL should be doing more of to increase customer awareness and brand presence. The company paid a well-known YouTube “influencer” named Aaron Marino to create a video titled “BIG Matt Gets A Makeover | Style & Shopping Tips for BIGGER Dudes”.

The clip been viewed over 350K times and has received over 8,000 likes. DXL offered a special promotional code and discount for viewers of said video. Note that this video is an “indirect” advertisement, i.e., it is an ad concealed under the guise of a lifestyle vlog. This type of marketing is generally perceived as more authentic.

Note the muted response to DXL’s own YouTube videos, which collectively have less than 3K views. I mention this in particular because, according to the Q2 and Q4 2017 earnings calls, younger customers make up a small but fast-growing segment of DXL’s customer base that spend more and shop more frequently.

DXL must attract younger customers in order to sustain growth, and this type of “influencer” marketing is important to this end. It seems that management is aware of this: per its 10-K, "In fiscal 2017, we increased our marketing expenses to $29.5 million, with an emphasis on new creative and additional digital advertising."

Conclusion

As goes without saying, DXL’s management must reduce operating expenses and/or improve gross margins in order to engineer a turnaround in share price and company performance. Given DXL’s strong brand positioning, lack of brick & mortar competitors, and management’s ongoing restructuring efforts, I am cautiously optimistic about Destination XL’s future.

In addition, DXL has a valuable opportunity to market itself as the go-to source for all things B&T. The company also appears to be focused on extending its dominant position to digital by focusing on developing its mobile app and e-commerce capabilities. DTC currently comprises 21.1% of TTM sales.

However, the retail landscape is a challenging one and it is difficult to pinpoint exactly what proportion of B&T consumers would be likely to shop at a specialty retailer like Destination XL. In addition, the bull case for DXL is contingent upon management’s ability to execute and walk a fine line between maintaining top-line results while reducing costs. As mentioned before, DXL’s competitive edge may be dulled if department stores begin to increase their B&T efforts.

The “bull case” scenario assumes that:

- Management will be able to gradually reduce SG&A expense levels to 2016 levels and achieve profitability.

- Depreciation and amortization expenses will decline steadily (while management has mentioned that D&A expenses will decrease now that new store build-outs are mostly complete, the exact level of D&A expense reduction is unknown.)

- Gross margins will remain relatively stable.

This investment thesis may be derailed if:

- Management fails to execute its game plan and improve operational efficiency.

- Macy’s and other retailers step up its sales and marketing efforts to B&T consumers.

- The B&T niche is not as large as expected and/or the retail environment worsens.

- Ongoing trends in healthy eating/fitness indirectly affect store traffic and top-line performance.

All in all, DXLG shares at these levels appear reasonably attractive from a risk-reward standpoint. However, company performance must be carefully monitored to ensure that the bull case scenario remains intact.

I'll continue to monitor the company's progress and will keep readers updated via articles on this site. Note that the company will be reporting Q2 2018 earnings after market close on Thursday, August 30. Please feel free to reach out with any comments or questions either via the comments section or through email (email address is in my Seeking Alpha bio). Thanks for reading!