Note: All prices herein are in Canadian dollars.

On Jan. 8, Aurora Cannabis (NASDAQ:ACB) provided analysts with revenue guidance for the first time. Aurora has set expectations at $50 to $55 million in revenue for the calendar fourth quarter:

"Based on preliminary (unaudited) results, the Company anticipates revenues for Q2 2019 of between $50 million and $55 million (net of excise taxes), compared to $11.7 million for the same quarter in the prior year, and compared to $29.7 million for the previous quarter ended September 30, 2018 ("Q1 2019"). The results reflect an anticipated revenue growth rate in excess of 327% compared to Q2 2018 and in excess of 68% compared to Q1 2019."

Aurora also suggested they will have positive EBITDA by the second calendar quarter of 2019, or Aurora's Q4/19:

"Additionally, disciplined cost management is anticipated to result in SG&A costs to be roughly consistent with the previous quarter, including a full quarter of costs related to all integrated subsidiaries in MedReleaf, Anandia and Agropro. Consequently, management believes the combination of substantial revenue growth and disciplined cost management positions the Company well to achieve sustained positive EBITDA beginning in Fiscal Q4 2019 (Calendar Q2 2019)."

This earnings report matters because it will be Aurora's first earnings report since Canadian recreational cannabis was legalized on Oct. 17. This 92-day quarter includes 76 days of legalized cannabis (83%). Thus, revenue is quite unpredictable since market share and market size for this nascent market are both unknown - although we're slowly seeing data on the size of those markets, such as the data I used in Canadian Cannabis May Generate A Quarter-Billion In Fourth Quarter Sales: Sales Data Analysis.

Aurora's guidance is lower than what analysts expected. According to BNN Bloomberg, analysts expected revenue of $67 million in this quarter:

"Aurora Cannabis Inc. says it expects to report second-quarter revenue of between $50 million and $55 million.

Analysts had expected revenue at the marijuana producer to total about $67 million for the quarter ended Dec. 31, according to Thomson Reuters Eikon."

$14 to $21 Million in Incremental Revenue

Last quarter, Aurora had pro forma revenue of $34.2 million to $35.8 million, depending on which acquisitions are included in the pro forma calculation:

| Q4/18 | Q1/19 | Chg | |

| Combined pro forma revenue | $33.1M | $35.8M | 8% |

| Aurora & MedReleaf (pro forma) | $33.1M | $34.2M | 3% |

| Aurora | $19.1M | $29.7M | 55% |

| MedReleaf | $14.0M | $4.5M | |

| Agropro, Borela, Anandia | $1.6M |

Source: Author based on company filings, table from my previous article on Aurora Cannabis.

Given pro forma sales of $34 to $36 million last quarter, Aurora's suggestion of $50 to $55 million in December quarter revenue (calendar fourth quarter, Aurora's Q2/19) implies that Aurora will generate between $14 and $21 million of incremental revenue from recreational cannabis. Actual recreational sales may vary from this range, depending on how well medical cannabis sales do in the December quarter.

Estimated Market Share of 10% to 15%

From Aurora's guidance and a few other pieces of information, we can estimate Aurora's market share. Based on this information, I estimate that Aurora's market share is in the range of 10% to 15%.

This calculation involves a couple different data points, notably:

- The Government of Canada's Cannabis Demand and Supply – initial report for October 2018.

- Data from Hexo (OTCPK:HYYDF) earnings, which I covered in Hexo: Recreational Cannabis Propels 300% QoQ Revenue Growth.

The Government of Canada announced a preliminary summary of cannabis sales and inventory for the month of October 2018. That data includes:

| Dried (kilograms) | Oil (litres) | |

| Sales - medical (October 1-31) | 2,756 | 5,479 |

| Sales - non-medical (October 17-31) | 4,504 | 1,763 |

| Sales | 7,261 | 7,243 |

| Federal licence holders | 13,798 | 30,163 |

| Provincial distributors/retailer | 6,382 | 2,458 |

| Finished inventory (October 31) | 20,180 | 32,621 |

| Federal licence holders | 96,037 | 13,725 |

| Unfinished inventory (October 31) | 96,037 | 13,725 |

Source: Government of Canada.

Among other things, this chart includes non-medical (recreational) cannabis sales volume for October 2018 and inventory levels of provincial distributors and retailers at the end of October.

Cannabis companies recognize revenue when they sell cannabis to provincial distributors. As a result, inventory levels will be included in cannabis revenue for licensed producers, including Aurora. Given that inventory prior to calendar Q4 was functionally zero (although Aurora did sell ~100 kg of recreational cannabis in the previous quarter), this inventory also will contribute to Aurora's December quarter sales.

The sales totals above include 15 days of recreational cannabis sales - Oct. 17 to Oct. 31. Aurora's December quarter will include an additional 61 days of cannabis sales. Any estimate we make from full-quarter sales will be only an estimate since daily cannabis sales will vary. Two of the leading causes of that variance will be:

- Initial cannabis sales were very high. There were lineups at cannabis stores due to pent-up demand and the novelty factor. As a result, weekly sales for the rest of the quarter may be lower than October sales.

- Initial cannabis availability was poor. Through the quarter, more stores are opening which will increase supply. Further, stores in Quebec and elsewhere already were running out of cannabis in October - meaning that sales for October were lower than true demand, even adjusted for the number of stores that were open. I discussed the gives and takes in more depth elsewhere.

These two factors cut in opposite directions. To take the simplest possible extrapolation, I'll simply suggest that full-quarter cannabis sales will continue at the same sales/day pace of the first 15 days of cannabis sales. This results in sales of:

| Dried Cannabis | Cannabis Oil | |

October sales (15 days) | 4,504 kg | 1,763 L |

Full quarter sales (76 days) | 22,820 kg | 8,933 L |

In addition to these sales, I will estimate that end-of-December inventory levels will be ~equal to end-of-October inventory.

Next, we can convert the cannabis oil sales to dried cannabis to determine total sales by kilogram equivalent. This step is necessary because we will be using a blended average price (including both dried cannabis and cannabis oil) to convert from dollars - as Aurora predicted - into weight. Thus, we need to combine these two totals.

From a prior conversation with Hexo's investor relations, I know that Hexo's oral sprays have a conversion factor of 10 mL being equivalent to 1 gram of dried cannabis:

Source: Via Hexo investor relations.

This equivalency factor is unlikely to be universal, but it's a reasonable estimate for converting cannabis oil volume into a kilogram equivalent. This results in:

| Sold at Retail | Inventory | Total | |

| Cannabis oil est. | 8,933 L | 2,458 L | 11,391 L |

| Oil equivalency | 10 mL = 1 g | ||

Cannabis oil est. (in kg) | 893 kg | 246 kg | 1,139 kg |

| Dried est. | 22,820 kg | 6,382 kg | 29,202 kg |

| Total LP sales est. (Q4/18) | 23,714 kg | 6,628 kg | 30,341 kg |

Source: Author based on various data.

Licensed producer sales will be made up of both cannabis sold at retail in the quarter and cannabis which ends the quarter in inventory at retailers and distributors. Combined cannabis estimated to be sold at retail and inventory from end-of-October (under the assumption it will be roughly the same at the end of December), I arrive at an estimate of ~30,000 kilogram equivalents sold in calendar Q4/18.

That figure alone doesn't get us Aurora's market share, however. To do that, we need to convert my incremental revenue estimate of $14 to $21 million into kilogram equivalents. This task is made easier by Hexo's earnings release.

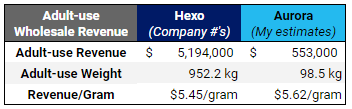

In that release, Hexo told us that their gross revenue per gram of cannabis sold for the recreational market was $5.45/gram. Gross revenue includes the cannabis excise tax, which we will want to exclude to determine net revenue.

Cannabis excise tax is detailed on the Government of Canada's website for federal taxes, but there are also provincial taxes. For the majority of provinces, this duty works out to the greater of 10% of the wholesale price of the cannabis or $1.00/gram ($0.25/gram federally and $0.75/gram provincially).

Source: Government of Canada; an example of provincial and federal excise taxes.

Recreational cannabis is much less than the $10/gram level needed to allow a 10% tax to be higher than a $1/gram tax, so we can simply estimate recreational excise tax at $1/gram.

Both Hexo and Aurora earned ~$5.50/gram for their recreational cannabis sales:

Source: Author based on company filings.

If we take an estimate of $5.50/gram gross and apply a $1/gram excise tax, we come up with a net recreational cannabis price of $4.50/gram. Using that price, we can convert Aurora's incremental recreational cannabis revenue into a weight equivalent and, from there, convert that figure into a market share:

| Low | High | |

| Aurora Incremental Revenue | $14,000,000 | $21,000,000 |

| Net price/gram | $4.50 | |

| Volume sold (kg equivalent) | 3,111 kg | 4,667 kg |

| Total market est. | 30,341 kg | 30,341 kg |

| Aurora market share | 10.3% | 15.4% |

Source: Author's estimates.

Based on the above, I estimate that Aurora might have 10% to 15% market share of the Canadian recreational cannabis market.

Thoughts

Aurora's guidance was a disappointment compared to the expectations of analysts. That said, Aurora's expectation to "miss" guidance here says more about the quality of the analyst estimates in this sector than it does about Aurora's performance, in my view. This is a nascent market with little to go on: Analysts in the sector are almost uniformly bullish, often irrationally so, in my view.

To supply a bit of context to Aurora's possible 10%-15% market share, it may be useful to look at Aurora's value relative to the value of the market. That information can be used to supply a bit of context here.

By my count, Aurora currently trades at an enterprise value of about $6.6 billion (partially-diluted using Black-Scholes for options/warrants). In sum, the enterprise values of the 28 Canadian cannabis producers that I track is $40 billion.

Source: Author in a previous article on Ontario cannabis sales.

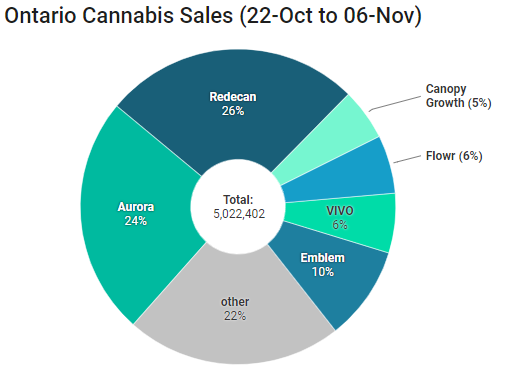

Notably, however, my listing of 28 companies excludes some private companies (e.g., Redecan who led in Ontario cannabis sales in October) and also excludes Canada's Island Garden, which is a subsidiary of Pyxus (PYX). This listing also excludes several smaller producers. Combined, those companies may account for another $5 billion in value.

In total, this gives Aurora a value of a little less than 15% of the total Canadian cannabis market:

| Aurora Market Share est. | 10-15% |

| Aurora Enterprise Value est. | $6.6 billion |

| Total Market EVs est. | $45 billion |

| Aurora's value as % of Market | 14.7% |

Source: Author's estimates.

In that light, Aurora's share of the total cannabis market is perhaps slightly disappointing - it's a little lower than their value as a percentage of the market, at midpoint.

However, Aurora's actual recreational cannabis sales may end up higher than the $14-21 million range. Aurora may be lowballing their guidance slightly in order to beat that guidance. Aurora also may have seen a shift in sales from medical to recreational cannabis - which would result in higher recreational sales than just their incremental revenue.

Further, Aurora also has businesses which are aimed outside of Canada. For example, Aurora paid $8 million to purchase Europe's largest organic hemp producer in September and paid $290 million to purchase ICC Labs in South America in September. Given the attention paid to Aphria's (APHA) LATAM purchases, readers may have doubts about whether the prices paid for these assets accurately reflects their true value. Despite potential valuation concerns, however, it's clear that Aurora (and Canopy Growth (CGC), among others) has non-Canadian assets that add value to its enterprise. Many of the smaller Canadian producers lack those assets. As a result, we might expect Aurora's EV (as a percentage of the Canadian market) to be a bit higher than their Canadian market share.

Overall, Aurora's guided revenue looks approximately in-line with their value relative to the rest of the market.

Last year, Aurora announced their December quarter earnings on Feb. 8, so we have about a month before we learn Aurora's actual earnings. Notably, however, Aphria earnings (covering up to Nov. 30) are due out on Jan. 11, which will be the second earnings release covering legalization, after those of Hexo.

Happy investing!

Members of The Growth Operation, my cannabis newsletter community, receive:

- Daily run-downs of breaking cannabis news - including news on both U.S. and Canadian cannabis producers.

- Exclusive access to my in-depth research articles cannabis companies and the cannabis market in the United States and Canada.

- Access all my past Seeking Alpha articles - even back-articles that are no longer free.

- Free trials are available all month.