HCP, Inc. (HCP) is a promising income play for dividend investors in the healthcare REIT sector, but only at the right price. The healthcare real estate investment trust faces favorable long-term industry trends, has a strong balance sheet, and covers its dividend with AFFO. That said, though, the REIT's shares do not make an attractive value proposition for long-term dividend investors based on today's stretched valuation. In addition, HCP is at the brink of being overbought, potentially exposing investors to a correction over the short term. An investment in HCP yields 4.7 percent.

HCP - Portfolio Overview

HCP is a healthcare real estate investment trust with large investments in senior housing properties, medical office buildings, life science buildings, hospitals, and other healthcare-related facilities. Senior housing and medical office buildings account for the lion share (61 percent) of HCP's property investments.

Here's a breakdown by property type.

Source: HCP Investor Presentation

Source: HCP Investor Presentation

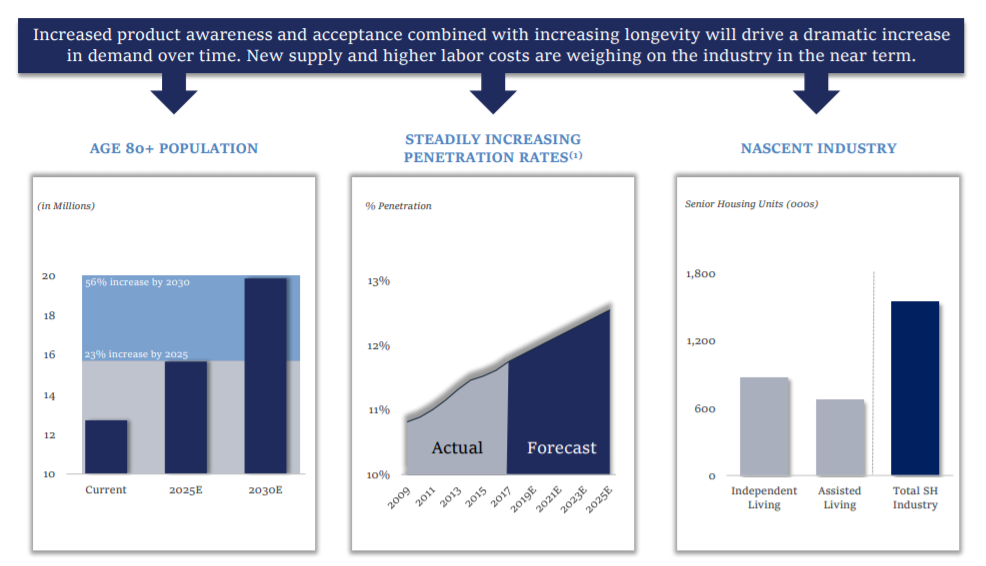

HCP benefits from an aging U.S. population and rising healthcare expenditures, especially as it relates to advanced age cohorts (80+). Strong projected growth in U.S. elderly demographics bodes well for HCP's senior housing part of the property portfolio going forward.

Source: HCP

Source: HCP

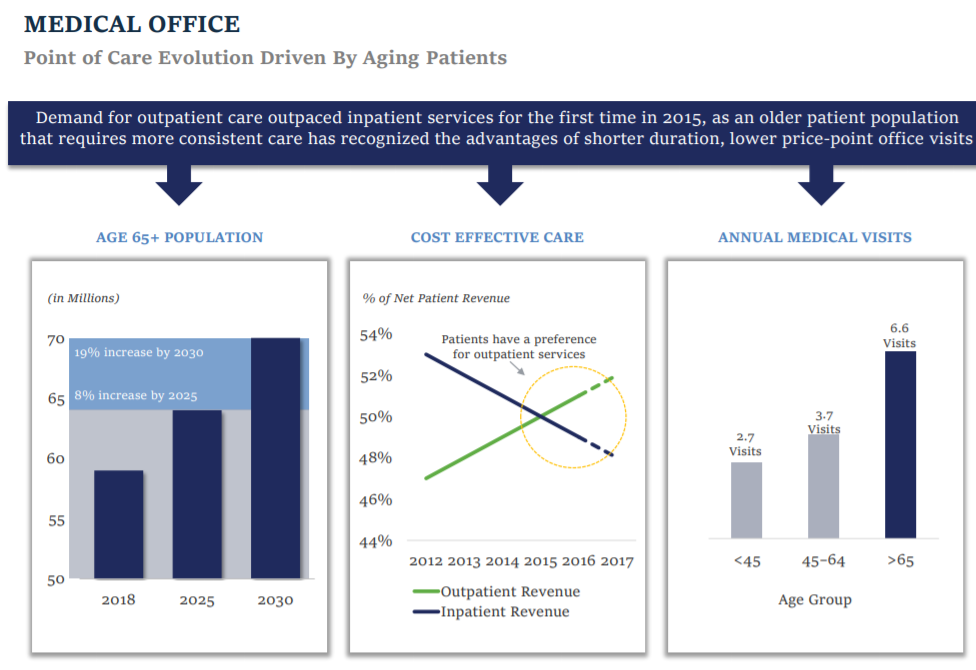

At the same time, HCP benefits from increasing demand for outpatient care. Patients require easy, cost-effective and efficient visits to healthcare professionals, which is why outpatient revenues (which are directly related to medical office buildings) have steadily risen over the last couple of years.

Source: HCP

Source: HCP

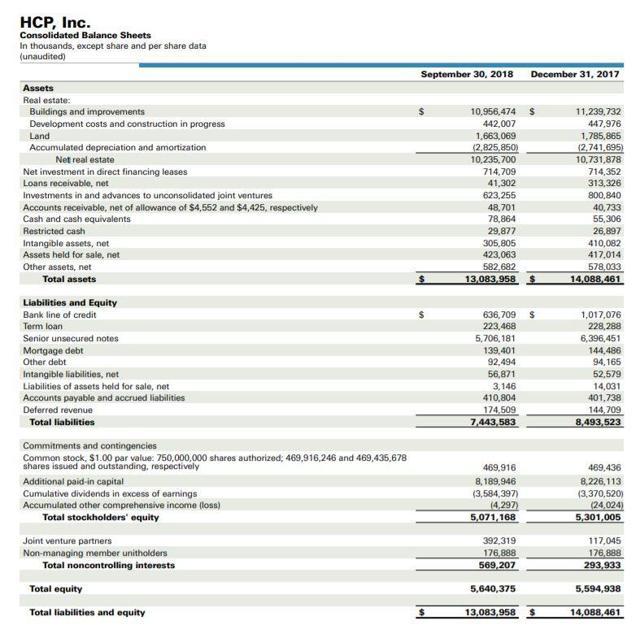

Balance Sheet Lends Some Downside Protection

HCP has an investment-grade rated balance sheet (BBB+ rating from Standard & Poor's, Baa2 rating from Moody's, and BBB rating from Fitch), which adds a layer of protection to the investment thesis in case the U.S. economy slides into a recession or the healthcare REIT industry heads for a downturn.

Source: HCP

Source: HCP

Solid Distribution Coverage

HCP