As we announced last year on Seeking Alpha, we commenced the New Money Portfolio to capture alpha intelligently, without chasing for yield. To be considered as a pick within our New Money Portfolio, the company must be considered a strong buy.

In order to provide readers with a more detailed playbook than just buy/hold/sell picks, we provide a few more granular recommendations, such as strong buy, speculative buy, and trim. Here’s our definition of strong buy:

Strong Buy means that I am recommending a high-quality REIT that's trading at a wider margin of safety. Recognizing principal preservation is critical, my recommendation is telegraphing readers that the company is a blue chip on sale.

One of the key valuation differences between a regular buy and strong buy is that the company must have enhanced price appreciation catalysts that support annual total returns of 25% or higher (over 12-18 months).

To be clear, our results aren’t predicated on short term trade tactics, aka “market timing.” Instead, we utilize the New Money Portfolio as Buffett-like model in which we strive to incorporate deep value investing principles along with modest diversification.

So far, in the first quarter of 2019, the New Money Portfolio has returned 16.9%, and there are 11 REITs (out of 31) that have returned in excess of 20% year-to-date. Although many of these picks have been downgraded from Strong Buy to Buy (due to price appreciation) we maintain a tactical approach in which we look to squeeze as much as we can out of each stock to achieve our targeted goals and objectives.

In order to better evaluate the New Money Portfolio, I thought it would be interesting to provide readers with the best and worst of the bunch, commencing with three of the biggest winners and then three of the biggest losers.

Finally, at the end of the article I will provide some comparisons to some of the more popular yield-chaser names, such as Washington Prime (WPG) and Global Net Lease (GNL). So let’s get started…

Top 3 Performers

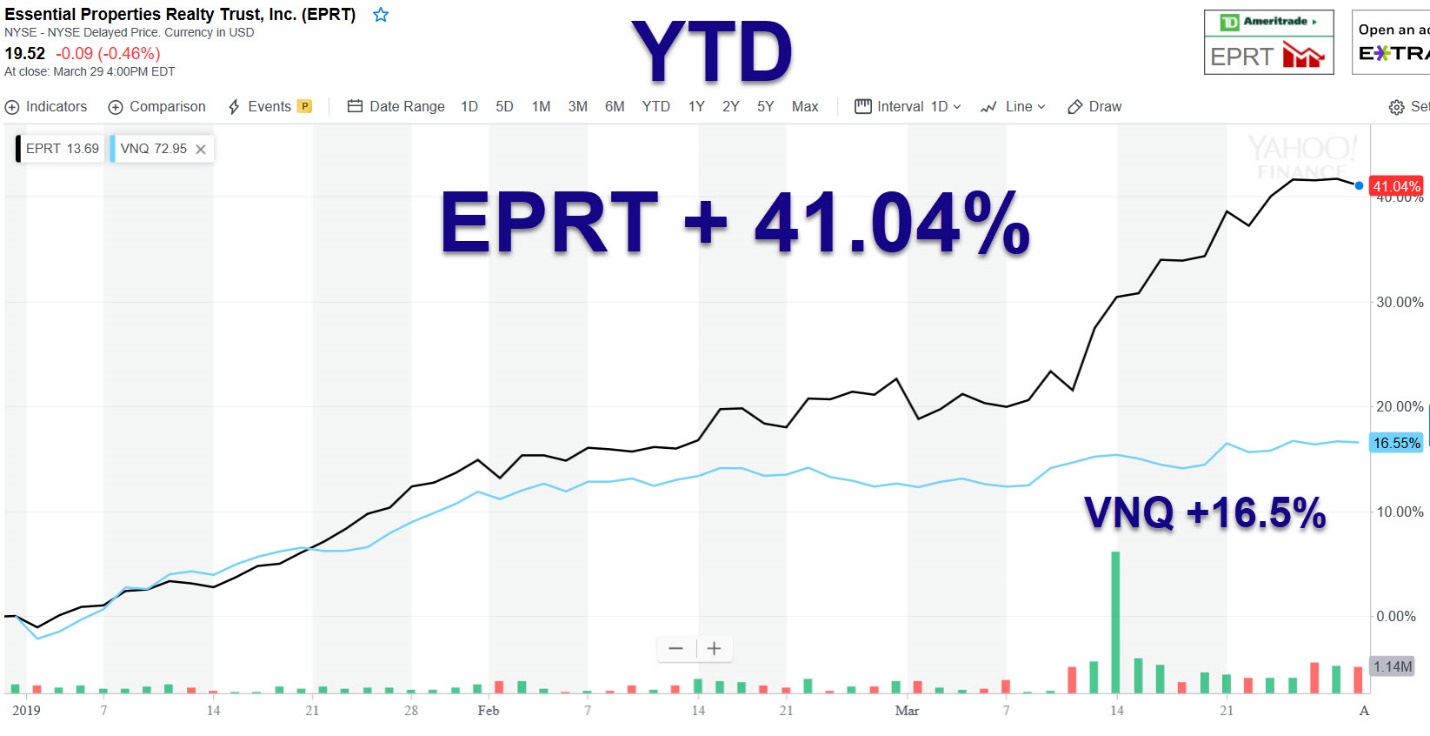

Essential Properties Realty Trust (EPRT) is our overall top-performer year-to-date (Q1-19) returning in excess of 41%. In case you missed it, I wrote an introductory article on the company just after it listed shares (began trading on June 21, 2018) and I conclude that the company has “all of the ingredients to become the next Realty Income (O).”

Then in December 2018 we initiated a strong buy on EPRT “based on the favorable risk management practices and discounted valuation.” We explained that “there's at least 20% upside and that EPRT should be trading in line with STOR and NNN.” We added that the “6.0% dividend yield screams strong buy, and this warrants our strong buy (25% total return target) recommendation.”

Source: Yahoo Finance

CatchMark Timber (CTT) is our second-best performer in the New Money Portfolio, shares have returned a whopping 38% year-to-date. In November 2018 we explained that CTT’s management team “has been very clever in driving upside in its EBITDA without dramatically changing its debt load.” We added that the “hint of (shareholder) buybacks marks for a fundamental change in a company that was intently focused on getting scale.”

Our ultra-bullish tone suggested that “an investment in timber has a place in any portfolio, especially at lows when market sentiment is at its weakest” such that “if the company was sold in the private market today it would fetch a higher price than what is being indicated by the market.” Our approach to fundamental analysis and understanding NAV (net asset value) was key to unlocking value: “the income story is in place (5.6% dividend yield), and the management team has excellent experience. CatchMark is simply the best choice.”

Source: Yahoo Finance

Hannon Armstrong (HASI) is our third-best New Money pick. Shares have returned in excess of 35% year-to-date. Back in November 2018 we explained that “HASI will soon begin returning to its previous policy of dividend increases, and we suspect the company to boost its dividend by around 4-5% in 2019. This will certainly provide for a catalyst and our expectation that the company could return 15-20% in 2019.” Then in February 2019 we explained that we are “glad to see the dividend growing again in 2019. The company announced a 2% increase in the quarterly dividend to an annualized $1.34 per share.”

We are not only encouraged by the dividend growth, but also the record $1.2 billion of transactions closed in 2018. The combination of higher portfolio yields (from the balance sheet investments) and higher securitizations in 2018 allowed HASI to increase its core return on equity to an impressive 11%. Although we believe the company remains on solid footing, we are trimming shares in HASI and we have removed the Strong rating (based on valuation).

Source: Yahoo Finance

Worst 3 Performers

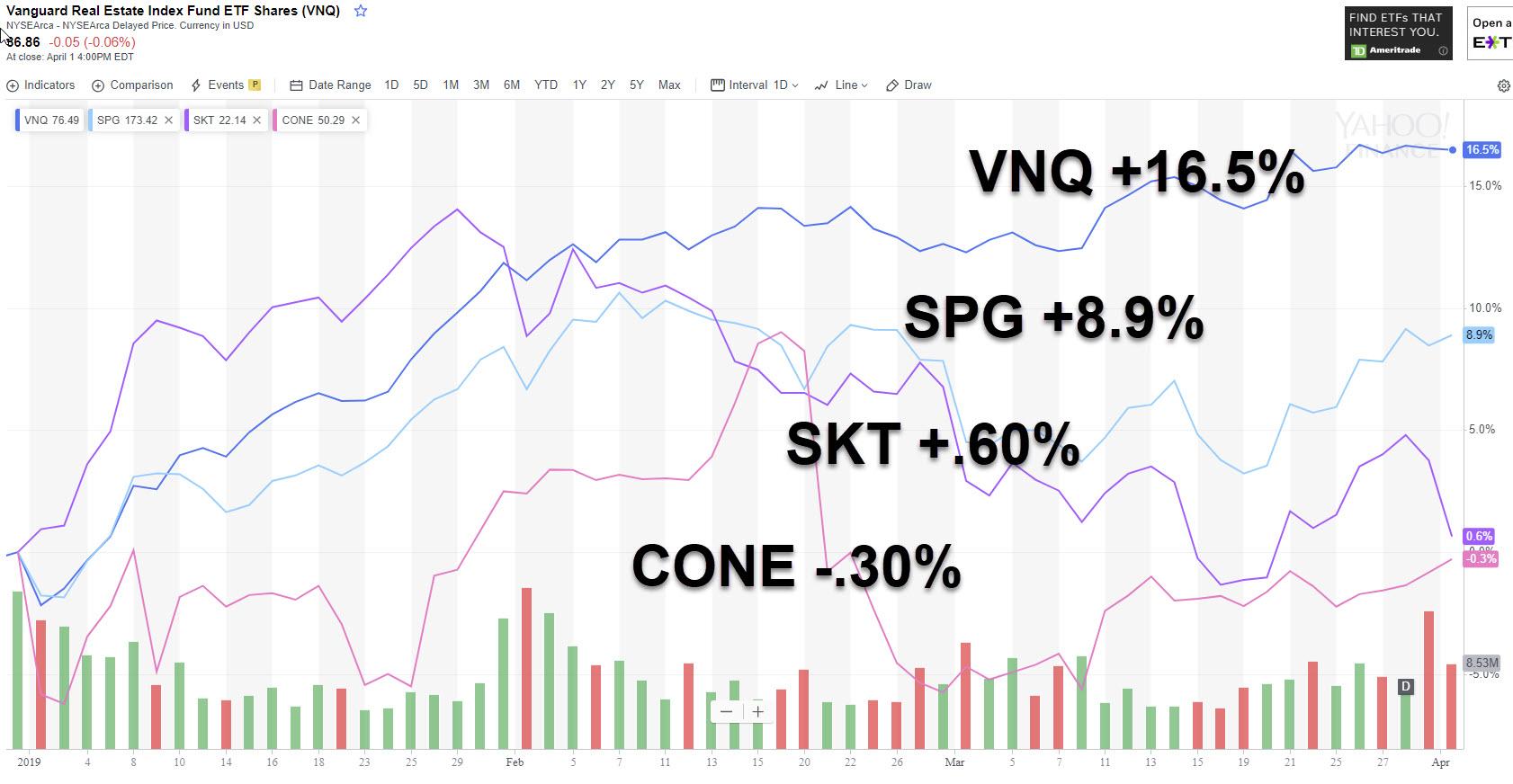

Our overall worst New Money performer year-to-date is Tanger Outlets (SKT), returning -.50%. Although many have exited the name, we continue to purchase more shares utilizing dollar cost averaging. In addition, we consider diversification a key to our successful portfolio modeling strategies, and we believe that ultimately Tanger will deliver strong returns (I'm working on an in-depth article later in the week).

Recently, another writer explained his short position in Tanger by claiming that “the dividend is not as covered as it would first appear, and the ball remains in SKT's court to prove that they will be able to handle the upcoming higher expiring rents.” The proof already is in the pudding, so to speak, Tanger has a best-in-class payout ratio in the mall REIT sector, and the company does not have to worry about utilizing excess cash flow (or FAD) to fund high capex redevelopment like the traditional mall REITs. So the payout ratio is actually the secret sauce for Tanger, and I will provide these details for you later in the week.

CyrusOne (CONE) is the second worst performers year to date, shares have returned 2.7%. Although the company’s 2019 FFO per share guidance fell short of the consensus estimate, we’re convinced CONE has set the stage for growth in 2020 and beyond, with outsized potential to generate returns in the high double digits. Consider CONE a high-growth data center REIT.

CONE’s mission-critical facilities protect and ensure continued IT infrastructure operation for approximately 1,000 customers - including more than 205 Fortune 1000 companies. The strong balance sheet, helped by S&P’s credit upgrade last September, provides significant financial flexibility and capacity to fund growth: with no near-term debt maturities, debt fully unsecured, and liquidity of approximately $1.6 billion. Again, like Tanger, we are taking the opportunity to purchase more shares cheaper, recognizing that our “strong buy” thesis will eventually play out to our advantage.

Simon Property Group (SPG) is the third worst New Money performer. Shares have returned 6.9% year-to-date. Although the lower-quality mall REITs (ie CBL and WPG) are experiencing headwinds with redevelopment, Simon’s balance sheet is positioned nicely for outperformance. Simon’s cost of capital is just 3.5% (courtesy of one of just 2 "A" credit ratings) that allows the company to borrow massive amounts of money at very low interest rates. The company has access to revolving credit facilities with more than $7 billion in remaining liquidity in case it wants to tap short-term credit markets to fund its growth.

Not that Simon even needs that since it's generating $1.35 billion in annual retailed adjusted funds from operations (operating cash flow minus maintenance costs). So while low-quality malls (Class D, C and B) are indeed struggling, high-quality Class A Malls (which make up 26% of all malls), ones like what Simon owns, are thriving. The core fundamentals, which are ultimately what long-term income investors need to track to know the health of its business, are all excellent: Average sales per square foot: $650 (top 75 malls $750), revenue growth (first 9 months of 2018): 2.1%, FFO/share growth: 10%, dividend growth (YOY): 11.3%, occupancy: 95.5% (up 0.8% from Q2 and above historical average of 94.3%), same-store net operating income: +2.3%, and lease spread 13.9%.

Source: Yahoo Finance

Source: Yahoo Finance

We have confidence that these Strong Buys will generate strong returns “at some point.” As I alluded to at the beginning of the article, “my recommendation is telegraphing readers that the company is a blue chip on sale.” As Benjamin Graham reminds us all (in The Intelligent Investor),

“The wise men finally boiled down the history of mortal affairs into the single phrase, “this too will pass.” Confronted with a like challenge to distill the secret of sound investment into three words, we venture the motto, margin of safety. This is the thread that runs through the preceding discussion of investment policy – often explicitly, sometimes in a less direct fashion.”

Don’t Chase Yield

As I explained in an article last week, “this reaching for yield is just asking for trouble. These high yielding REITs are often referred to as yield traps, meaning they have terrible fundamentals, including deteriorating business models and cash flows, weak balance sheets, and the risk of having their dividends cut or eliminated.”

As I referenced above (with regard to Tanger), the payout ratio is an important metric to consider because it determines the overall safety of the dividend. Two examples of REITs to avoid include Washington Prime and Global Net Lease.

Although both REITs are high yielding (WPG’s dividend yield is 18.2% and GNL’s dividend yield is 11.3%), we consider the payout ratios dangerous and extremely speculative. It’s important for readers to understand that there's an enhanced risk to loss of principal because even though the shares appear cheap, a likely dividend cut could spark further price erosion.

Do you remember these words, “The More It Drops, The More I Buy?”

As intoxicating as it may sound, buying more of WPG and GNL could result in painful losses, and that’s of course why I include the word “strong” in front of our sell recommendation (WPG and GNL are Strong Sells). Thus, even though year-to-date returns for these two REITs are decent (WPG +21.2% YTD and WPG +10.2% YTD), a dividend cut could spark a selloff that could result in painful defeat.

According to data from FAST Graphs, WPG’s AFFO payout ratio is 120% and GNL’s Payout Ratio is 107%. This means that, unlike Tanger, these two REITs have no buffer to protect against unforeseen events (case in point: CBL just announced it was suspending the dividend for two quarters to settle a lawsuit).

Had you hit the buy button a year ago with CBL (CBL) (after reading, The More It Drops, The More You Buy), you would have seen your CBL account drop by more than 70%.

Source: Yahoo Finance

In Conclusion

We take pride in our REIT research because it has led to superior returns (16.9% YTD). Although we don’t claim 20% YTD returns across the board (for all picks), we definitely have more winners than losers, and the secret to that success has been the power of the margin of safety. As such, our diversified basket of Strong Buy picks has allowed us to smooth out the impact of the outliers (ie SKT, CONE, and SPG) – despite the fact they all have a strong margin of safety. Howard Marks (The Most Important Thing) explains,

“Whereas the theorist thinks return and risk ate two separate things, albeit correlated, the value investor thinks of high risk and low prospective return as nothing but two sides of the same coin, both stemming primarily from high prices. Thus, awareness of the relationship between price and value – whether for a single security of an entire market – is an essential component of dealing successfully with risk.

Author's note: Brad Thomas is a Wall Street writer, and that means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free, and the sole purpose for writing it is to assist with research, while also providing a forum for second-level thinking.

Note: Chart with VNQ,SPG, SKT, and CONE was updated as of 4/2/19.

Invest with the #1 Ranked REIT and #1 Finance Analyst on Seeking Alpha

"Your articles should be mandatory in High schools and Colleges, as a separate subject on real estate investments."

"Always well-written, factual, and very entertaining, and you did it the hard way."

"Brad is the go-to guy, with REITs. Wonderful info, he has provided great ideas, on which I read & perform my own DD."

"Brad Thomas is one of the most read authors on Seeking Alpha, and he has developed a trusted brand in the REIT sector."

We are providing this special offer so you can sleep well at night...

![]()