An investor who has all the answers doesn’t even understand all the questions. - Sir John Templeton

In bioscience investment, there are many data pieces that are dynamic. They are like characters in The Matrix who shape-shifted to fit their changing environment. As such, you have to piece them together into a grand collage to get the underlying theme. That phenomenon is best illustrated through an oncology-focused innovator dubbed Atara Biotherapeutics (NASDAQ:ATRA). Despite what seemed to be a clear runway to the promised land of mega-profits, Atara's senior management suddenly bid farewell.

Like an earthquake that topped the Richter scale, the aforesaid event shook investors' confidence to the core. Investors with a weak stomach vomited and took their losses. In the aftermath, the stock depreciated over 50%. Some investors holding the stock became disillusioned and confused. Though a lot of money was lost, Atara still procured 30% gains for IBI's core portfolio Alpha. The elephant in the room is whether there are further upsides. In this research, I'll present a fundamental analysis of Atara and piece together the underlying story of corporate change.

Figure 1: Atara stock chart (Source: StockCharts)

Figure 1: Atara stock chart (Source: StockCharts)

About The Company

As usual, I'll deliver a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Operating out of San Francisco, California, Atara is focused on the innovation and commercialization of allogeneic T-cell immunotherapies (“A-TCI”) to serve the strong unmet needs in cancers and autoimmune diseases. As A-TCI functions similar to a CAR-T, it rallies the most important cells of the immune system (i.e. T-cells or generals of an army).

Instead of engaging CD4 (helper T-cells), A-TCI primes CD8 (killer) T-cells with intelligence to improve these cells’ adeptness at detecting and destroying cancers and virus. Powering by A-TCI, Atara is growing a robust pipeline of immunotherapies. The partnership with Memorial Sloan Kettering (MSK) also enabled Atara to deliver the next-generation mesothelin-targeted CAR-T (i.e. MT-CART)

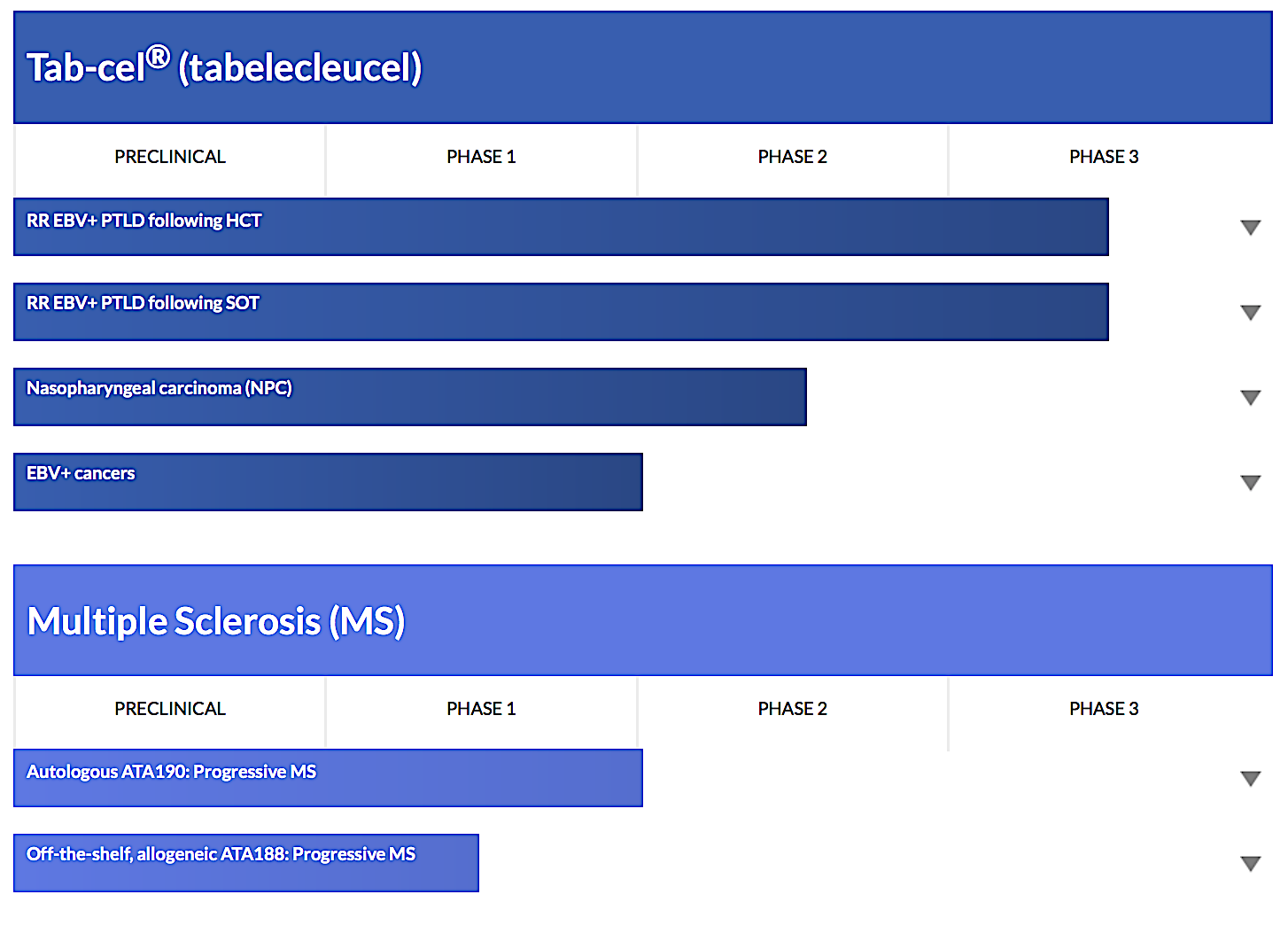

Figure 2: Therapeutic pipeline (Source: Atara)

Figure 2: Therapeutic pipeline (Source: Atara)

Tab-Cel

The reigning champion of Atara's pipeline is an off-the-shelf Epstein-Barr Virus (“EBV”)-specific A-TCI coined tabelecleucel (i.e. tab-cel). Currently being investigated in two Phase 3 (MATCH and ALLELE) trials, tab-cel seems like the answer for patients afflicted by EBV associated post-transplant lymphoproliferative disorder (EBV/PTLD) following either hematopoietic cell transplantation (“HCT”) or solid organ transplant (“SOT”).

Backed by strong data for a rare disease, Atara easily convinced the FDA and EMA to grant tab-cel the Orphan Drug Designation. Moreover, the company secured the FDA Breakthrough Therapy designation and EMA Priority Medicines status for tab-cel. Following suit, Health Canada placed tab-cel into the expedited approval category.

In the latest earnings report, Atara disclosed that tab-cel enrollment for the aforementioned Phase 3 studies are proceeding slower than anticipated. I believe that is due to the rare nature of the disease rather than the efficacy and safety of tab-cel. In other words, it's difficult to recruit patients because there aren't many of them.

Poised to capture the global market, Atara will file a conditional approval for tab-cel in the EU with the initial Phase 3 results in 2020. After the application is accepted by the EMA, Atara will disclose the preliminary top-line results. In my view, MATCH/ALLELE will most likely deliver positive outcomes to warrant conditional approval. And since there is a strong demand for EBV/PTLD treatment, conditional approval should be forthcoming. Thereafter, full approval is definitely within grasp.

CAR-T

As Atara expanded its research and development (R&D) collaboration with the premier MSK Cancer Center, the company is enjoying the fresh blood of next-generation CAR-T to nourish its pipeline. During the 2019 American Association of Cancer Research (AACR) Annual Meeting, MSK reported strong Phase 1 results for MT-CART. In the pilot study, patients suffering from malignant pleural mesothelioma experience the remarkable 72% response rate following MT-CART treatment. Additional results were presented at the 2019 American Society of Clinical Oncology ("ASCO") Annual Meeting.

With excellent early data, Atara/MSK are pushing MT-CART in combination with an immune checkpoint inhibitor (anti-PD-1). Amid this ongoing development, Atara expects to file an investigational new drug ("IND") application in 2020. In my view, MT-CART does not hold empty promises. Rather, it'll empty out the cancer cells in the patient's body. My rationale stemmed from the high efficacy in the pilot study. Moreover, MT-CART is highly adept at knocking out deadly cancers. When you pit an MT-CART with a PD1 inhibitor, all hell breaks loose for cancers because of the uncanny treatment synergy. Specifically, the immune checkpoint inhibitor will release the brake on the immune system for MT-CART to zone in for the kill.

Multiple Sclerosis

In addition to tab-cell and MT-CART, Atara is brewing a multiple sclerosis (“MS”) portfolio that comprises of ATA-190 and ATA-188 for autologous progressive MS and allogeneic progressive MS/recurrent relapsing MS (“RRMS”), respectively. Early in May, the company presented good Phase 1 safety data for AT-188 at the 5th Congress of the European Academy of Neurology (EAN). Additional safety and efficacy data will be featured at a scientific conference in 2H2019. As a "wild card," I do not have much expectation for the MS franchise. But if ATA-190 and -188 can surprise investors with positive results, the market bull will enjoy a most vigorous rally in the history of this stock.

With the sound underlying fundamentals, there is a good chance for ATA-190 and -188. Aside from steroid and immunosuppressants, there is no other treatment option for MS. Current MS treatments have notorious side effects. As such, the demand for novel treatment is so strong that market bulls want to jump out of the gate like synchronize swimmers about to take a dive. If Atara can garner positive results for its MS portfolio, this stock should be worth at least several billion dollars higher. After all, the MS market is already worth at least $21B in 2016. And, it's growing at a rapid pace.

Management Shuffling

Despite strong pipeline development, I found that the recent management changes quite "mind-boggling." This is a crucial point in the company's growth cycle for such a drastic shift. On May 28, Atara announced the appointment of Pascal Touchon as the new President and CEO. Interestingly, Touchon has over 30 years of bioscience leadership experience. Most remarkably, he served as the Global Head of Cell & Gene and member of the Oncology Executive Committee at Novartis (NVS). Underneath his belt is the successful launch of tisagenlecleucel or Kymriah. Aside from managing global CAR-T operations, Touchon led multiple clinical studies and built a strong leadership team. He also held leadership positions in various companies such as Servier, Sanofi (SNY), and Glaxo (GSK).

It probably takes a week for Touchon to finish polishing his trophy case. And his entry into Atara couldn't have been better. After all, this is the Golden Age of CAR-T. Nonetheless, there was a lot of uncertainty about how events will unfold, because in connection with Touchon's appointment, two former captains left the ship. Specifically, Isaac Ciechanover stepped down after seven years of leadership and servitude. Concurrently, the Global Head of Research and Development (Dr. Dietmar Berger) departed to "pursue other opportunities." Ciechanover remarked:

When I announced my decision to step down in January, I had agreed to stay on until my successor was chosen. I am thrilled with the appointment of Pascal, who I know will lead the company in its next stages of growth.

I've been pondering for a while what "exactly happened" at the corporate headquarter. What other opportunities could be better for Berger than heading the R&D of a thriving organization. In bioscience investing, you have to read the tea leaves because the surface picture can be convoluted. In my search, I came to the conclusion that both executives were forced to leave, but on good terms. I doubt that Ciechanover was thrilled by Touchon's entry. As Touchon's specter is now looming large over Atara with his CAR-T's crown, there is no room for Ciechanover. That being said, it seems that Atara is now shifting its growth strategy toward CAR-T rather than immunotherapy. I don't blame the company because CAR-T has unprecedented efficacy and safety for deadly cancers. The drug truly delivers hopes in seemingly hopeless cancers. Therefore, it made sense that Atara ramped up its think tank.

The departure of Berger is not in isolation. A good number of investors fled which accounted for the strong share price depreciation. They all followed Ciechanover's footstep. And, their departure signals either loyalty to the former Chief who brought substantial fortunes to the company or fear of incoming losses. For me, I would have been happier had Ciechanover and Berger stayed on board. Regardless of their prowess, it sours my taste when a company brought in new talents from other firms. It's more prudent to reward loyalty within the organization, as Philip Fisher recommended. But cruelty is a reflection of the survival of the fittest in the business world. You simply have to play with the cards that you're dealt with.

Financial Assessment

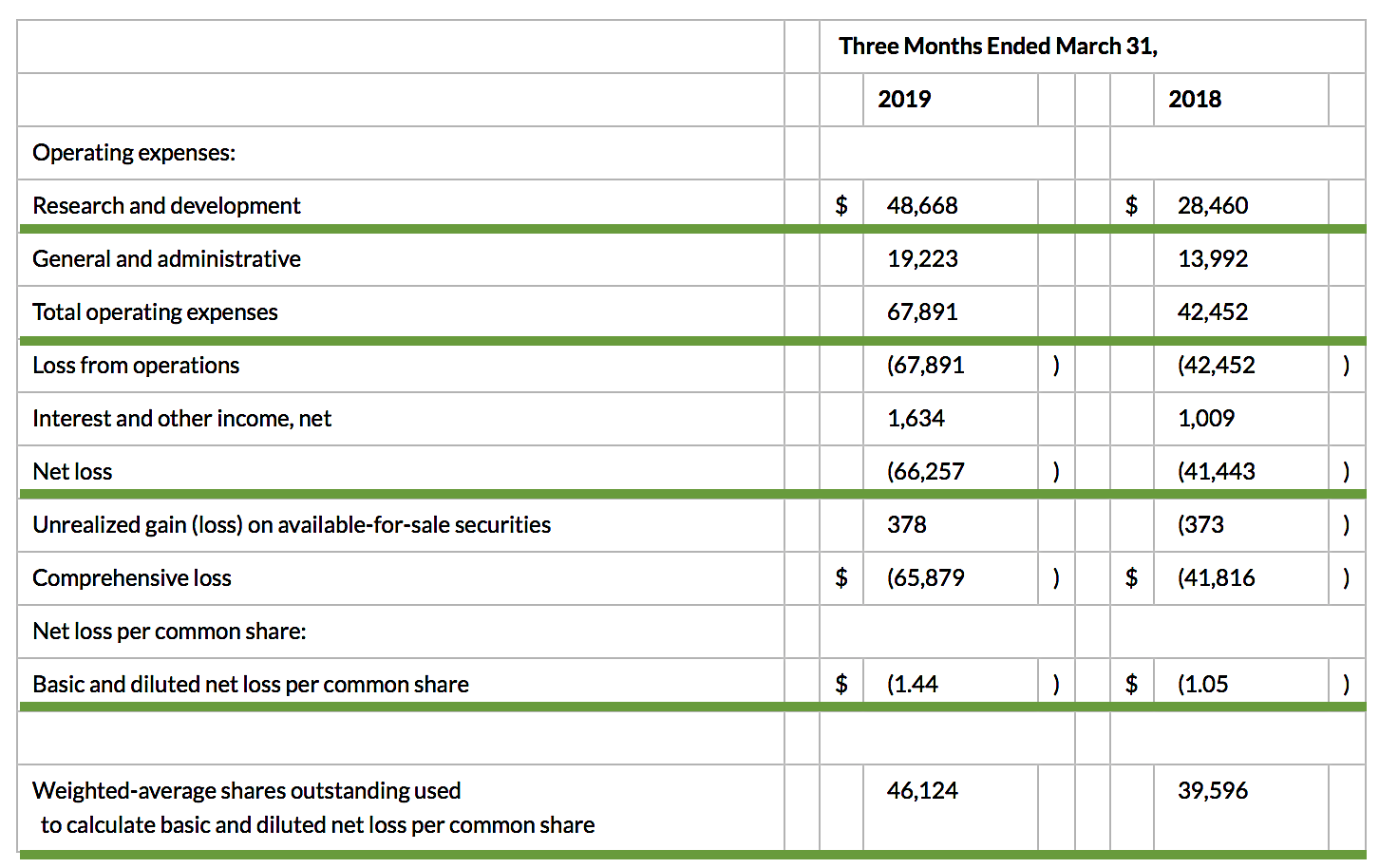

Just as you would get an annual physical for your well-being, it's important to check up on the financial health of your stock. For instance, your health is affected by "blood flow" as your stock's viability is dependent on the "cash flow." With that in mind, I'll analyze the 1Q2019 earnings report for the period that concluded on March 31. As a young developmental-stage company, it's the norm that Atara has yet to generate any revenue. Therefore, let's analyze more meaningful metrics.

Accordingly, the research and development (R&D) registered at $48.7M compared to $28.5M for the same period a year prior. The bulk of R&D spending was attributed to the development of ATA-188 and tab-cel. I view the 70.8% year-over-year (YOY) R&D increase positively because the money invested today can turn into blockbuster profits tomorrow. You have to plant a tree today in order to enjoy its fruits. That aside, there was $66.3M ($1.44 per share) net losses versus $41.4M ($1.05 per share) decline for last year. The 31.4% bottom line depreciation is due to higher R&D and other corporate expenses.

Figure 3: Key financial metrics (Source: Atara)

Figure 3: Key financial metrics (Source: Atara)

Regarding the balance sheet, there were $237.5M in cash, equivalents, and investments. Based on the $67.8M quarterly operating expense (OpEx) rate, I calculated that there should be adequate capital to fund operations into year-end prior to the need for an additional offering. Notwithstanding, an offering should be coming soon. Of note, investors usually shy away from a public offering. Contrarily, I prefer a young bioscience company to raise capital this way rather than incurring substantial bank debts. Short-term bank debts can be recalled anytime that can prompt a company to file a Chapter 11.

Though I do not mind a public offering, it's important for you to determine if you are holding a "serial diluter." A firm that employs dilution as a "cash cow" will render your investment essentially worthless. As the shares outstanding increased from 39.5M to 46.1M for Atara, my rough arithmetics yield the 16.7% dilution. At this rate, Atara easily cleared my 30% dilution cutoff for a profitable investment. Hence, this company is most definitely not a serial diluter.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your investment regardless of its fundamental strengths. Moreover, the risks are growth-cycle dependent. At this point in its life cycle, the main concern for Atara is whether the lead franchise tab-cel can generate positive clinical outcomes and thereby gains conditional approval first and full approval later. In case of a negative clinical event for tab-cel, the stock will likely tumble over 70% and vice versa. With excellent prior data, I believe that tab-cel will deliver good results. Therefore, I ascribed a 35% chance of clinical failure for tab-cell.

The other risks center around the clinical data of its CAR-T and MS franchises. Nonetheless, if they fail to procure positive results, the stock will most likely tumble around 50% because they are not the main assets at this point in Atara's growth cycle. There is also the concern that Atara might grow too aggressively and thereby runs into the potential cash flow constraint. Additionally, the departure of top-level management could foretell fundamental deterioration rather than an organic focus on CAR-T.

Conclusion

In all, I reduced my buy recommendation on Atara to a hold. I also lowered my rating from five to four of five stars. My lower rating accounted for the higher risks of trial failure associated with the departure of Drs. Ciechanover and Berger. Atara is a leading immunotherapy innovator. And by 2020, the company will file for conditional approval of tab-cel in the EU. Thereafter, the initial data will be released. I expect good results from that franchise. Now in the efforts to capture the rising tide of CAR-T, Atara strengthened its partnership with MSK to deliver the next-generation mesothelin-targeted CAR-T for solid tumors. Perhaps, the company is too aggressive that it replaced the former chief, Ciechanover, with the CAR-T All-Star, Touchon. Even the Head of R&D Berger resigned. Though investors are rocked by the possibility that organic problems prompted senior leadership to run, it's more likely that Atara is pushing for CAR-T to replace tab-cel. In bioscience investment, you have to work with the available data pieces to synthesize the big picture.

If you're holding this stock, it's best to reduce the position in half to account for the potential risks. If Atara managed to generate good data, this stock can easily rally multiple folds. And if the potential wild card (MS assets) hits, Atara will appreciate far higher than its current valuation. By reducing your position rather than selling out, you positioned yourself to reap profits while not losing the barn in case of failure. Last but not least, the story on Atara reinforced the need to diversify rather than overly concentrate on any bioscience investment.

Thanks for reading! Please hit the orange "Follow" button on top for updates.

Dr. Tran's analyses are the best in the biotech sphere, well worth the price of subscription.

Very professional, extremely knowledgeable, and very honest … I would highly recommend this service and his stock picks have been very profitable.

Simply put, this is worth every penny. Just earlier today, one of the companies recommended by Dr. Tran got acquired for a nice 50% premium.

As I reserve higher market intelligence and exclusive features for IBI members, I invite you to take my temporary offer of 2 weeks FREE TRIAL.