In a matter of just a few weeks, the epicenter of the coronavirus is now deemed to be in Europe, according to the World Health Organization. The virus may have originated from China, but China - and most other Asian countries - have had far more success than other countries around the world in managing this crisis.

I believe we are going to see a divergence in fortunes in Asian and European equity markets for the next six to nine months. While the investing environment may be fraught with many unknown unknowns, what we can see at hand is the difference in capability of different countries and regions in dealing with the virus. This is a known known and can be used to make a rational investment decision.

China warned of the emergence of the coronavirus in January 2020, theoretically giving other countries more than enough lead time to prepare for it. In the highly interconnected world we live in today, it would be foolhardy and complacent for any government to think the virus will not spread to its borders.

China's government took aggressive and swift action in locking down Wuhan and neighbouring cities, a bold authoritarian move that effectively put 50 million people under mandatory quarantine. On hindsight, this helped dramatically reduce the rate of infections in China.

You can see the total coronavirus cases in China tapering off. To date, China has 80,849 cases of infection. Against a population size of close to 1.4 billion, that represents less than 0.01% of the population being infected. Yes, 0.01%! China has been hugely successful in dealing with an infectious disease despite having the world's largest population spread out across mammoth swathes of land.

At last count, China reported a measly 20 new coronavirus cases on 14 March. Sometimes an authoritarian government helmed by one man within a single party is useful in dealing with a crisis, as political gridlock is avoided. This virus is going far to challenge our mindsets on different political systems.

Source: Worldometers.info

Source: Worldometers.info

Other Asian countries have tapped on their experience in dealing with the outbreak of SARS in 2003 and recent onset of MERS and swine fever and have been efficient in stemming the spread of the virus, employing a mix of measures which include free testing of the virus and social distancing. They have also been effective in using big data to their advantage in contact tracing.

Despite China sounding the alarm bells early enough for other countries to take action to prepare for the spread of the coronavirus, European countries have been extremely slow in managing the risk. You can see from the chart below the sharp rate of infections across Europe compared to Asia. In comparison, Taiwan and Hong Kong have reported about 47 and 129 cases respectively despite their close proximity to China.

While I very much hope that Europe will eventually follow in China's footsteps in ridding the virus, the fact that it has little or no experience dealing with past pandemics like SARS will not play to its favour.

Europe is also made up of a number of member states, and while broad sweeping stimulus packages like this EUR 37 billion investment initiative delivered by the European Commission will on paper help the bloc, there will be many questions on how targeted these initiatives are with respect to individual member states. Tourism-dependent Greece is very different from Italian carmakers.

In Italy, Salvini's first instinct was to politicise the coronavirus episode by calling Conte's government incompetent. Fontana, the League governor of Lombardy, called the virus "a little more than the normal flu", and is now forced to eat his words. In the UK, only 36% of Britons trust Boris Johnson's handling of the coronavirus crisis.

The European Center for Disease Prevention and Control warned that the actual number of COVID-19 cases in Europe could be far higher due to under-detection, while German Chancellor Merkel expects two-thirds of the German population to get the virus.

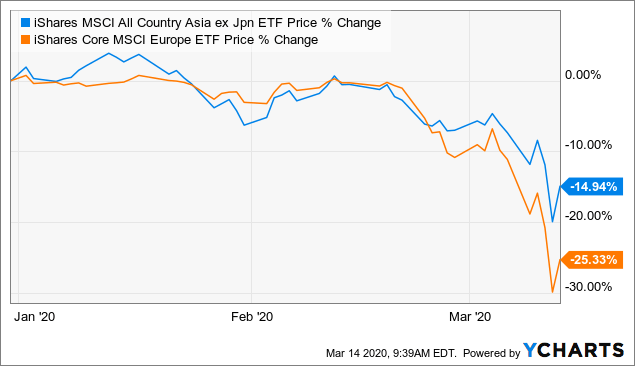

The difference in capability of governance in Asia and Europe has translated into divergent performances in their equity markets. Year to date, the iShares MSCI All Country Asia ex Japan ETF (AAXJ) has returned -14.9%, while the iShares Core MSCI Europe ETF (IEUR) has returned -25.3%.

Data by YCharts

Data by YCharts

With the virus still rampant in Europe, and as member states in the European Union close their doors to each other, European equities will continue to take a further beating in the next 6-9 months. As a sign of how fortunes have reversed, Apple (AAPL) has closed all its stores outside China until 27 March, and has reopened its stores in China. The WHO is right - the epicenter of the virus is now firmly in Europe.

The million-dollar question is whether it is the right time to enter the equity markets in general, or is there more bloodshed to come. There are no definitive right or wrong answers to this question, but I will show you some charts where I believe the risk-reward currently favours buying equities.

The VIX index is now near its 2008-2009 highs. I believe the world already knows we are headed for a global economic contraction. That said, if we are able to avoid a series of high-profile defaults and bank runs (Lehman-style), then the damage to equities can be contained. My guess is that the VIX moves lower at this point, supporting equities.

A lot of selling has been done by funds in the volatility-targeting space. Due to the spike in volatility, volatility-targeting funds have been forced to pare down their exposure to US equities, to the extent that their implied allocation to US equities now stands near the 0 percentile level since 2000, as noted by Nomura's Charlie McElligott.

A lot of selling has been done by funds in the volatility-targeting space. Due to the spike in volatility, volatility-targeting funds have been forced to pare down their exposure to US equities, to the extent that their implied allocation to US equities now stands near the 0 percentile level since 2000, as noted by Nomura's Charlie McElligott.

Trend-following CTA strategies are also almost entirely 100% short across global equities, while risk-parity fund exposure has been reduced to 2.9 percentile since 2011.

The conclusion I would draw is that positioning is relatively clean in the equity space, after heavy deleveraging and selling from the three aforementioned financial strategies. The volatility-targeting fund space is estimated at USD 400 billion, CTA strategies are estimated at USD 250 billion, and the risk-parity space is estimated at USD 400 billion.

The conclusion I would draw is that positioning is relatively clean in the equity space, after heavy deleveraging and selling from the three aforementioned financial strategies. The volatility-targeting fund space is estimated at USD 400 billion, CTA strategies are estimated at USD 250 billion, and the risk-parity space is estimated at USD 400 billion.

We now share our investing world with these new-fangled financial strategies, which tend to sell into downtrends, and buy into uptrends, hence exacerbating the market move at hand. It should come as no surprise that this is the Dow's fastest 20% drop in history.

With equity exposures for these strategies relatively clean, I will reiterate that the risk-reward favours buying equities at this point. Equities moving higher from here will also receive tailwinds from volatility-targeting and risk-parity funds building back exposures.

The S&P 500 managed to rebound strongly from its long-term trendline on Friday's close. Its uptrend is still very much intact for now.

I tend to refrain from using words like bottom-fishing, as it implies a sense of complacency and misplaced confidence that we have already seen the worst. However, after weighing the odds, equity markets are currently looking more "bottom-like" than "abyss-like" for now.

I tend to refrain from using words like bottom-fishing, as it implies a sense of complacency and misplaced confidence that we have already seen the worst. However, after weighing the odds, equity markets are currently looking more "bottom-like" than "abyss-like" for now.

Do note that the risks are very real that the coronavirus situation might simply flare up in a matter of days, which may very well lead to more fear-induced selling in equities. That said, judging from the manner of and data associated with the sell-off, the question I would like to end off is: "At this juncture, who is left to sell equities?".

If you feel risk-on still, then my suggestion would be to have a nibble at Asian equities.

The Xtrackers Harvest CSI 300 China ETF (ASHR) is still holding its range despite the coronavirus fears, which is a sign of strength.

The iShares MSCI Taiwan ETF (EWT) is still trading above its multi-year uptrend.

The iShares MSCI Taiwan ETF (EWT) is still trading above its multi-year uptrend.

Since launching in June 2019, my technical analysis service has generated an absolute return of 50.1% with 32 trade recommendations as of March 2020 (excluding trades that are still Live) with an average holding period of 6.5 weeks per trade. Do check out my Marketplace Service at The Naked Charts!